Thinking you can get by with your home health insurance or a basic travel plan while living abroad is one of the most common—and costly—mistakes…

Thinking you can get by with your home health insurance or a basic travel plan while living abroad is one of the most common—and costly—mistakes expats make. These policies are built for short trips, not long-term life in a new country. A quick expat medical insurance comparison shows you exactly where the dangerous gaps are.

For anyone serious about living abroad, a specialized global medical plan isn’t a luxury; it’s absolutely essential.

Why Your Old Health Plan Isn’t Enough for Life Abroad

Moving to another country is a massive undertaking, and it completely changes what you need from your healthcare coverage. The insurance that served you well back home, or that cheap travel policy you grabbed for a two-week vacation, just wasn’t designed for the realities of expat life. They are full of geographical limits and are meant for temporary emergencies, not your actual, ongoing well-being.

Think about it this way: a standard travel policy is great for a sudden, unexpected medical event—a broken leg while hiking or a nasty bout of food poisoning. It’s for emergencies. What it almost never covers are things like routine check-ups, managing a chronic condition like diabetes, or getting mental health support. This leaves you dangerously exposed, with the risk of paying huge out-of-pocket costs for everyday health needs. If you want to dive deeper, we have a detailed guide on why U.S. health insurance doesn’t work abroad.

Critical Coverage Gaps in Standard Plans

It’s always a shock for new expats when they discover what their old plans don’t cover. Relying on them gives you a false sense of security that can put both your health and your finances on the line.

A true expat medical plan is built completely differently. It functions just like your primary health insurance back home, but with a global footprint. The difference becomes crystal clear when you put them side-by-side.

| Feature | Standard Travel Insurance | Domestic Health Plan | Expat Medical Insurance |

|---|---|---|---|

| Primary Focus | Short-term emergencies | Care within home country | Long-term, comprehensive care |

| Routine Check-ups | Almost never covered | Covered within network | Included as standard |

| Chronic Conditions | Generally excluded | Covered within network | Managed and covered |

| Medical Evacuation | Often included (emergency) | Rarely included | A core, robust benefit |

The New Non-Negotiable for Global Living

It’s not just about having better coverage anymore. These days, a huge number of countries require proof of comprehensive health insurance just to approve your visa or residency application. A basic travel policy will almost certainly fail to meet their legal standards, putting your entire move in jeopardy.

An expat-specific plan is no longer just a good idea—it’s a foundational requirement for a secure and successful life abroad. It gives you peace of mind, satisfies legal obligations, and guarantees you have access to quality care, no matter where you are.

This is exactly why getting to grips with the core pillars of a global health plan is so critical. From worldwide provider networks that bill the insurer directly to robust medical evacuation services that can get you to the best care, these are the features that separate flimsy coverage from real protection. As we continue this expat medical insurance comparison, you’ll get the insight you need to choose a plan that truly safeguards your health and future.

Choosing the right expat medical insurance isn’t about chasing the lowest premium. It’s a different mindset entirely. You need to do a careful expat medical insurance comparison, matching a policy’s structure to the real-world demands of your life abroad. To pull this off, you have to look past the marketing fluff and learn the language of insurance to truly understand how a plan will impact your health and wallet.

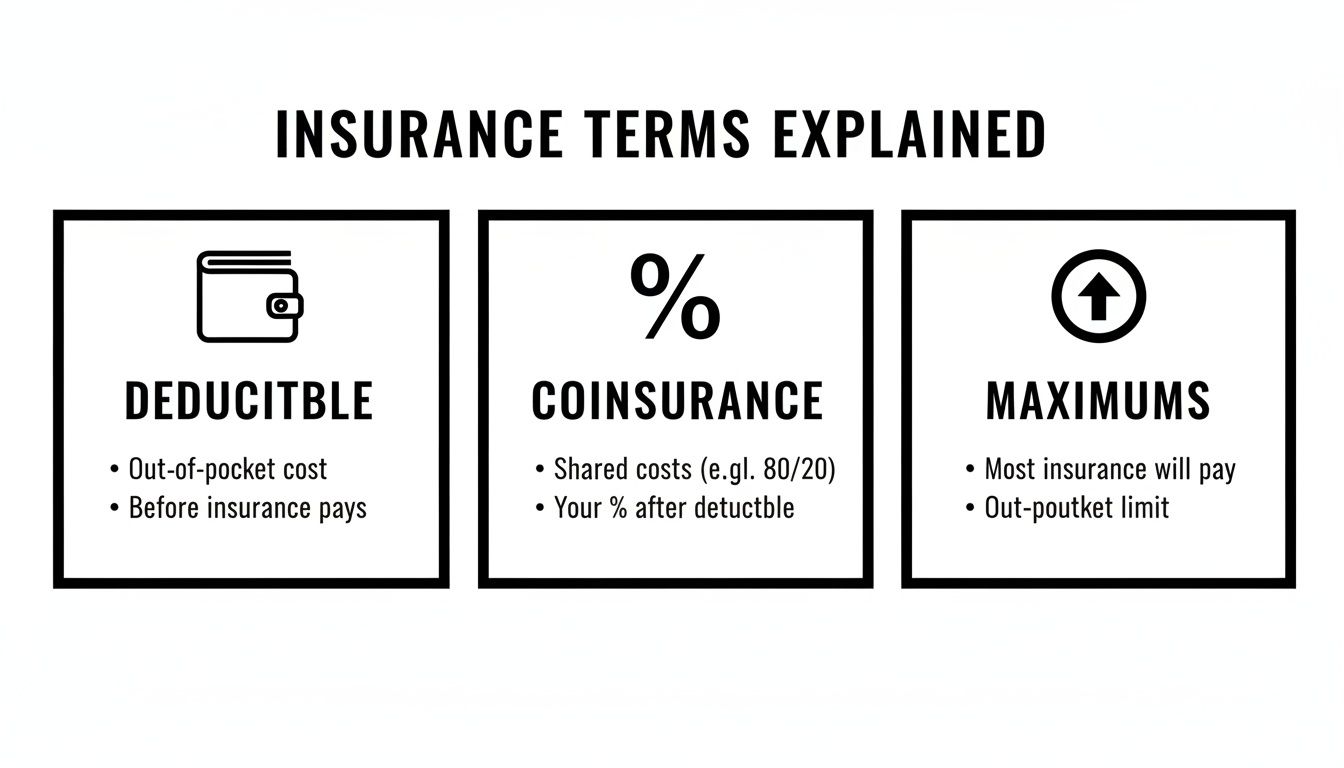

The whole process starts with getting a grip on the core financial pieces of any plan. These terms dictate what you’ll actually pay out-of-pocket when you need care, so nailing this part down is absolutely critical.

Read More: Do Expats in Canada Need Private Health Insurance?

The Financial Framework Of Your Plan

The first terms you’ll bump into are often the most important for your budget. They define the cost-sharing balance between you and the insurance company.

- Deductible: Think of this as the amount you have to pay for covered medical services before your insurance company starts chipping in. For example, if you have a $1,000 deductible, you’re on the hook for the first $1,000 of your healthcare costs that year.

- Coinsurance: Once you’ve paid your deductible, you and your insurer share the costs. A common split is 80/20. This means the insurance company covers 80% of the bill, while you pay the remaining 20%.

- Annual and Lifetime Maximums: This is the absolute ceiling on what an insurer will pay out for your claims. Lifetime maximums are becoming less common, but the annual maximum—often from $1 million to unlimited—is a huge indicator of a plan’s strength.

These pieces all work together. A plan with a high deductible usually comes with a lower monthly premium, which can be a smart move if you’re healthy and want to keep your fixed costs down. On the flip side, a lower deductible means a higher premium but less of a financial shock when you actually need to use your insurance.

Understanding how deductibles and premiums play off each other is the first step to finding a plan that fits your financial comfort zone. It’s a calculated trade-off between predictable monthly costs and what you might have to pay out-of-pocket.

Evaluating Your Scope Of Coverage

Beyond the numbers, the real meat of a plan is in what it actually covers. Expat plans are worlds away from standard travel policies, offering benefits designed for long-term health and well-being. When you’re comparing, you need to put these key areas under the microscope.

Start with the fundamentals of medical care:

- Inpatient Care: This is any treatment that requires you to be admitted to a hospital, like surgery, a stay in the ICU, or even just an overnight observation. Make sure the plan covers a private room, as that’s the standard in many countries.

- Outpatient Care: This bucket includes all the services that don’t need a hospital stay. We’re talking doctor’s visits, consultations with specialists, and diagnostic tests like X-rays and lab work.

- Prescription Drugs: Always check the formulary, which is the list of covered medications. You’ll want to be sure any prescriptions you take regularly are on that list.

This growing focus on comprehensive health is showing up in the data. In 2025, the adoption of travel medical coverage is expected to jump, with attachment rates climbing from 73.5% to 80.8%. As you weigh your expat insurance options, pay special attention to the limits for emergency evacuation—you’ll want at least $100,000—and waivers for pre-existing conditions, as these benefits can vary wildly from one plan to another. You can dive deeper into the 2025 travel insurance trends analysis on battleface.com.

Before we move on, having a structured way to compare plans is incredibly helpful. This checklist breaks down the essential features you should be looking at side-by-side.

Expat Insurance Comparison Checklist

| Feature/Criteria | What to Look For | High-Priority Consideration For |

|---|---|---|

| Annual Maximum | Is it at least $1 million, or unlimited? Lower limits can be risky. | Everyone, but especially those in countries with high healthcare costs. |

| Deductible & Coinsurance | How much will you pay out-of-pocket? Balance this against the monthly premium. | Budget-conscious individuals and those managing chronic conditions. |

| Geographic Coverage | Does it cover “Worldwide” or “Worldwide excluding USA”? The difference can save you 30-50%. | Expats who do not plan to spend significant time or seek care in the U.S. |

| Inpatient/Outpatient Care | Does it include private rooms? Are specialist visits and diagnostics fully covered? | Expats seeking comprehensive, day-to-day medical care. |

| Pre-existing Conditions | Is there a waiting period? Are conditions excluded or covered with a higher premium? | Anyone with a known medical history (e.g., diabetes, heart conditions). |

| Emergency Evacuation | Is the limit at least $100,000? Does it cover transport to the nearest adequate facility? | Nomads, adventure travelers, and those living in remote areas. |

| Prescription Drugs | Are your routine medications on the plan’s formulary? What are the coverage limits? | Individuals who rely on specific, ongoing medications. |

| Home Country Coverage | Does the plan cover you for short trips back home? For how long? | Expats who plan to visit their home country regularly. |

Using a checklist like this ensures you don’t overlook a critical detail that could end up costing you dearly down the road. It forces a methodical approach, which is exactly what you need when dealing with something as important as your health.

The Fine Print That Matters Most

Finally, the details buried in the policy documents can make or break your coverage. Skipping over these can lead to denied claims and bills you weren’t expecting.

One of the most critical clauses is the geographic area of coverage. Many plans offer “Worldwide” or “Worldwide excluding USA” options. Since medical care in the United States is notoriously expensive, excluding it can slash your premium by 30-50%. If you don’t plan on spending much time or getting treatment in the U.S., this is one of the biggest cost-saving levers you can pull. It’s also worth investigating the specifics of international medical insurance for expats to see how coverage in your home country works for those brief visits back.

Just as important are the rules around pre-existing conditions. Some insurers might enforce a waiting period before covering a condition you already have. Others might exclude it completely or agree to cover it for a higher premium. Being completely transparent about your medical history during the application isn’t just a good idea—it’s essential to make sure your coverage is solid when you actually need it.

A Side-By-Side Comparison of Top Expat Insurance Plans

Okay, let’s move from theory to reality and do a direct expat medical insurance comparison of what’s out there. But instead of getting bogged down by brand names, it’s far more effective to look at plans through the lens of archetypes—profiles built for specific expat lifestyles. This way, you can match your actual needs to a plan’s fundamental design.

We’re going to break down three common archetypes: ‘The Comprehensive Protector’ for families who need extensive benefits, ‘The Lean Globalist’ for solo expats who prioritize affordability, and ‘The Nomad Navigator’ for professionals who demand total flexibility.

The Comprehensive Protector For Families

This plan archetype is the gold standard for expats who simply can’t afford any gaps in their coverage, especially those with kids or other dependents. Its defining feature is a very high—or even unlimited—annual maximum. This ensures that even a catastrophic medical event won’t spiral into financial disaster. Peace of mind is the name of the game here.

Key features you’ll almost always find include:

- Robust Maternity and Newborn Care: Coverage for childbirth and care for the newborn is often included after a waiting period, a non-negotiable for growing families.

- Broad Wellness Benefits: Think routine check-ups, vaccinations, and sometimes even vision and dental. It functions more like a primary health plan you’d have back home.

- Strong Chronic Condition Management: These plans are built to handle ongoing health issues without forcing you to pay steep out-of-pocket costs, which is critical for long-term stability abroad.

The trade-off, as you might guess, is the cost. Premiums are significantly higher, but for anyone prioritizing complete, worry-free coverage for their family’s health, the value is undeniable.

The Lean Globalist For The Budget-Conscious

Not every expat needs—or can afford—a top-tier plan. ‘The Lean Globalist’ archetype is for the healthy, solo individual who wants solid protection against major emergencies without paying for bells and whistles they’ll likely never use. The entire strategy here is to manage costs by taking on a bit more of the financial risk yourself.

This is usually done through:

- Higher Deductibles and Coinsurance: By agreeing to pay more out-of-pocket for initial or shared costs, you can bring your monthly premium down substantially.

- Essential Inpatient and Outpatient Coverage: These plans stick to the core medical needs like hospital stays and doctor visits but might have lower limits or exclude things like wellness and dental.

- Excluding USA Coverage: Choosing a “Worldwide excluding USA” policy is one of the biggest cost-saving moves you can make, often slashing premiums by 30-50%.

This archetype is perfect for a self-funded expat or a retiree in good health. It’s about protecting your savings from a major medical disaster while keeping your fixed monthly expenses as low as possible.

This minimalist approach is tapping into a huge market. The broader travel insurance industry, valued at $23.8 billion in 2024, is expected to explode to $132.9 billion by 2034. Within that, travel medical insurance is the fastest-growing segment, highlighting a global trend toward prioritizing health security abroad. When you’re comparing these leaner plans, it’s crucial to look at the provider’s global network size and any post-2020 pandemic clauses. You can learn more about the travel insurance market’s impressive growth on alliedmarketresearch.com.

Before we jump into our third archetype, it helps to quickly review the financial terms that really define these plans. This infographic neatly summarizes the key insurance terms that dictate your out-of-pocket costs.

Getting a feel for the interplay between your deductible, coinsurance, and plan maximums is the key to balancing your budget with your coverage needs.

The Nomad Navigator For Global Professionals

Our final archetype is tailor-made for the modern location-independent professional—the digital nomad. This lifestyle demands maximum flexibility, since your home base can change on a whim. ‘The Nomad Navigator’ plan prioritizes worldwide access and rock-solid emergency support over routine, in-place care.

Hallmarks of this kind of plan include:

- Superior Medical Evacuation: High coverage limits for emergency medical transport are non-negotiable. This ensures you can get to the best possible care facility, no matter how remote you are.

- Seamless Telehealth Access: 24/7 access to medical professionals via phone or video is a core feature. It provides immediate advice without needing to track down a local clinic.

- Flexible Monthly Subscriptions: Many nomad-focused plans work like a subscription service, letting you pause or cancel coverage easily as your travel plans change.

This plan might offer less coverage for non-emergency outpatient services or chronic conditions, focusing its resources on agility and emergency response instead. For these plans, the user experience is a huge differentiator—pay close attention to how easy it is to make a claim online and how responsive their support team is. A strong direct-billing network is also vital, as it saves you from having to pay massive sums upfront and then wait weeks for reimbursement.

By thinking in terms of these three distinct archetypes, you can move beyond a simple feature list and start to see which plan structure truly aligns with your life abroad.

To make this even clearer, let’s put these archetypes into a simple comparison table. This should help you see the key trade-offs at a glance.

Expat Insurance Provider Archetype Comparison

| Feature | Archetype 1 (Comprehensive) | Archetype 2 (Budget-Friendly) | Archetype 3 (Nomad Specialist) |

|---|---|---|---|

| Ideal User | Expats with families, those needing maternity or chronic care. | Healthy, solo expats or retirees on a fixed budget. | Digital nomads, remote workers, frequent travelers. |

| Annual Maximum | Very high to unlimited. | Lower, but sufficient for major emergencies. | Moderate to high, with a focus on emergency services. |

| Key Strength | All-encompassing coverage, including wellness and routine care. | Low monthly premiums. | Ultimate flexibility and strong emergency support. |

| Cost Driver | Breadth of benefits (maternity, dental, wellness). | Higher deductibles and coinsurance. | Strong medical evacuation and telehealth services. |

| Main Trade-off | Highest premium cost. | Higher out-of-pocket costs when care is needed. | Less coverage for routine, non-emergency care. |

| Coverage Area | Typically worldwide, including the USA. | Often “Worldwide excluding USA” to save costs. | Worldwide, with easy on/off subscription models. |

As you can see, there’s no single “best” plan—only the plan that’s best for you. The Comprehensive plan offers total peace of mind for a price, the Budget-Friendly plan protects your savings without breaking the bank, and the Nomad plan gives you the freedom to roam without worry. Your lifestyle dictates the right choice.

Which Expat Insurance Profile Fits Your Life?

A smart expat medical insurance comparison isn’t just about spreadsheets and policy limits. It’s about understanding how those features translate into real-world protection that fits your life. There’s no single “best” plan. The right one is always the one that lines up with where you’re going, your health, and your family’s needs.

To make this tangible, let’s walk through four classic expat profiles. Seeing how their different situations dictate their insurance priorities will help you zero in on what truly matters for your own journey. It’s the best way to turn an abstract choice into a concrete, confident decision.

The Relocating Family in Europe

Picture a family with two young kids moving to Spain. Their needs go way beyond just emergency coverage. They’re looking for comprehensive, day-to-day healthcare that feels solid and dependable, so they can handle everything from fevers to check-ups without financial surprises.

For this family, a top-tier expat health plan is non-negotiable. Their shopping list would prioritize:

- Robust Maternity and Newborn Care: Even if they’re not planning another child, having this option provides huge peace of mind. Keep in mind these benefits almost always come with a 10- to 12-month waiting period.

- Comprehensive Wellness Benefits: We’re talking routine check-ups for the kids, annual physicals for the parents, and vaccinations. This is all about maintaining long-term health, not just reacting to problems.

- Low Deductibles and Copays: With kids, you know doctor visits for colds and scraped knees are just part of life. A plan with low out-of-pocket costs keeps these frequent, small expenses from adding up.

This family isn’t too worried about coverage for extreme adventure sports, but they’ll demand a high annual maximum and a strong network of direct-billing hospitals across Europe.

The Digital Nomad in Asia

Now, imagine a solo digital nomad bouncing between Thailand, Vietnam, and Bali for months at a time. For them, it’s all about flexibility and a rock-solid emergency safety net. They’re healthy and more concerned with protecting against a catastrophic event than paying for routine doctor visits.

Their focus is completely different from the family in Spain. They need a plan built for a life in motion.

For a digital nomad, the most critical features are high-limit medical evacuation and seamless telehealth access. Their plan must be able to respond instantly, no matter how remote their location, providing both virtual advice and a physical exit strategy if needed.

The key features for this profile are:

- High Emergency Evacuation Limits: A minimum of $250,000 is a smart starting point. This ensures they can be transported to a top-tier medical facility if something serious happens.

- Flexible Subscription Models: The freedom to pay monthly and easily pause or cancel coverage is a massive plus for a lifestyle that can change on a dime.

- A “Worldwide Excluding USA” Clause: Since they have no plans to work or get care in the United States, this is the single most effective lever they can pull to lower their premium.

The Retiree in Central America

Let’s consider a retiree moving to Costa Rica who is managing a pre-existing condition like hypertension. Their number one concern is predictable, affordable access to their ongoing care—from specialist appointments to prescription refills. Living on a fixed income means unexpected medical bills are a major threat.

This profile requires a very specific approach to coverage. A high deductible might bring the premium down, but it could leave them exposed to crippling costs for the routine care they know they’ll need.

Their comparison will dig deep into the policy’s fine print, looking for:

- Pre-Existing Condition Coverage: They must find a plan that explicitly covers their specific condition, even if it means a waiting period or a slightly higher premium. Some providers, like GeoBlue, might offer immediate coverage if you can show proof of prior insurance.

- Prescription Drug Formularies: It’s non-negotiable. They have to confirm their maintenance medications are on the insurer’s approved list to keep recurring costs under control.

- Strong Local Provider Network: Access to respected local doctors and hospitals that can direct-bill the insurer is vital for managing their health without constant administrative headaches.

The Corporate Professional on Assignment

Finally, let’s look at a professional on a two-year assignment in Dubai. Their company provides a basic local health plan, but it has some obvious gaps. It might not adequately cover dependents, offer protection for personal travel, or include robust emergency evacuation for trips outside the UAE.

This expat isn’t starting from scratch; they’re looking to supplement what they already have. The goal is to build a safety net that plugs the specific holes in their corporate plan.

This professional will be hunting for a policy that delivers:

- Global Coverage: A plan that protects them and their family during vacations and trips back home is a must.

- Emergency Medical Evacuation: The company plan likely only covers local emergencies. A supplementary plan with a powerful evacuation benefit provides a worldwide security blanket.

- Riders for Specific Needs: They can bolt on extras like dental and vision benefits if their primary plan is missing them, essentially building their own complete coverage package.

By seeing how your own life maps against these profiles, you can start to separate the “nice-to-haves” from the “must-haves.” That’s what makes an expat medical insurance comparison both personal and truly effective.

Navigating the Costs and Financial Tradeoffs

Figuring out the price tag on an expat medical insurance plan can feel a bit like solving a puzzle. But that final premium isn’t just an arbitrary number; it’s a direct reflection of your personal risk profile and the level of financial protection you’re signing up for. An effective expat medical insurance comparison means digging deeper than the monthly cost to understand what’s really driving it.

The biggest factors that will shape your premium are your age and current health. It’s just a fact of the industry: insurers see older individuals or those with pre-existing conditions as higher risk, and that translates to higher costs. Your destination also plays a huge role. A plan that covers you in a place with notoriously expensive healthcare, like Switzerland or Hong Kong, will naturally cost more than one designed for a country with more affordable medical services, like Thailand or Mexico.

Key Drivers of Your Insurance Premium

The single biggest cost variable you can actually control is your geographic area of coverage—specifically, whether you include the United States. Thanks to the sky-high cost of medical care in the U.S., adding it to your policy can pump up your premium by 30-50%. If you don’t plan on spending much time or seeking treatment in the States, choosing a “Worldwide excluding USA” plan is the single most powerful move you can make to manage your budget.

Beyond geography, your deductible is the next lever you can pull. Your deductible is simply the amount you agree to pay out-of-pocket before your insurance kicks in. When you opt for a higher deductible—say, $2,500 instead of $500—you’re signaling to the insurer that you’re willing to shoulder more of the initial financial hit. In return, they’ll give you a lower monthly premium. It’s a calculated tradeoff: you save on your fixed monthly bill but face a bigger one-time cost if you actually need to use the plan for something serious. You can get a much deeper dive in our comprehensive international medical insurance cost guide.

Spotting Hidden Costs and Making Smart Tradeoffs

A temptingly low premium can sometimes hide other potential expenses down the line. It’s so important to scrutinize the policy for limitations that could leave you with an unexpected bill. For instance, some budget-friendly plans might slap you with heavy penalties for going outside their approved network of doctors or hospitals, or they might not cover certain treatments like physical therapy or mental health support at all.

Choosing a plan is really an exercise in balancing cost against risk. A higher deductible can be a smart financial move if you’re healthy, while paying a bit more for a plan with a robust, direct-billing network can save you from administrative headaches and large upfront payments.

This balancing act is becoming even more critical as the industry grows. The global travel medical insurance market, valued at around $5.24 billion in 2024, is projected to nearly double to $10.21 billion by 2034. This boom is fueled by rising international medical costs and greater health awareness among expats and long-term travelers. You can read more about these global travel medical insurance market projections and trends on programbusiness.com.

Ultimately, the goal isn’t just to find the lowest price, but to find a plan that delivers real value. By understanding how your choices about deductibles, coverage areas, and provider networks directly impact your premium, you can build a policy that truly protects your health while fitting neatly into your financial strategy abroad.

How to Secure Your Ideal Expat Health Plan

Okay, you’ve done the hard work of comparing expat medical insurance plans and have a good idea of what you need. Now it’s time to turn that research into reality and lock in your coverage. This is the final, crucial step to protecting your new life abroad.

The application process is pretty straightforward, but it’s all about precision. Insurers need a crystal-clear picture of who you are and the level of risk they’re taking on to give you an accurate quote. Getting this right from the start prevents any nasty surprises or denied claims down the road.

Gathering Your Essential Information

Before you even think about filling out a form, get your documents in order. Having everything ready to go makes the application process smooth and fast, ensuring the quote you get is perfectly matched to your situation.

You’ll almost always need to provide:

- Detailed Personal Information: This means full names, dates of birth, and passport details for everyone you want on the policy.

- Complete Medical History: Get ready to be completely honest about any pre-existing conditions, past surgeries, or treatments you’re currently receiving. Full transparency isn’t just a suggestion—it’s essential for your coverage to be valid.

- Travel and Residency Plans: Know your primary country of residence and have a general idea of any other significant travel you’ll be doing. This helps insurers understand your geographic risk profile.

The Advantage of Using a Specialized Broker

Trying to navigate the fine print and finalize a policy on your own can be a headache. That’s why working with a specialized broker like Expat Global Medical is such a smart move. An expert broker does more than just show you a list of plans; they give you impartial advice that’s actually relevant to your life.

A good broker is your advocate. They use their deep industry knowledge to find you the best terms and pricing, cut through confusing policy jargon, and help you sidestep common mistakes. It’s about giving you total confidence in your choice.

With a clear plan and an expert in your corner, you can secure a policy that offers genuine peace of mind. This last step ensures your health and finances are protected, so you can focus on starting your new chapter abroad.

Still Have Questions? Let’s Clear Things Up

Even after you’ve compared a dozen plans side-by-side, a few questions always seem to pop up. Getting straight answers is the final step to choosing a plan with confidence.

What’s the Real Difference Between Travel Insurance and Expat Medical Insurance?

This is easily the most common point of confusion, so let’s cut right to it. Think of travel insurance as a short-term safety net for emergencies on a trip. It’s there for a broken leg, lost luggage, or a canceled flight.

Expat health insurance, on the other hand, is your primary, long-term health coverage for living abroad. It’s designed to handle everything from routine check-ups and specialist visits to managing chronic conditions, just like your plan back home would.

How Are Pre-Existing Conditions and Home Country Visits Handled?

For many expats, the biggest worry is how an insurer will treat their pre-existing conditions. Every policy is different, but you’ll typically see one of two approaches: a waiting period before a specific condition is covered, or a higher premium to include it from day one. Full transparency about your medical history during your application isn’t just a good idea—it’s essential to make sure your coverage is there for you when you need it.

Another question we hear all the time is, “Will I still be covered when I visit home?” Many expat plans include a “home country coverage” benefit for short trips back, usually lasting 30 to 90 days a year. This is a huge plus, but it’s meant for temporary or emergency care, not for planned long-term treatments.

Always read the fine print on home country coverage to know exactly how long it lasts and what’s included. That way, you’re protected no matter where in the world you are.

Ready to find a plan that actually fits your life abroad? The team at Expat Global Medical offers personalized advice and free quotes from the world’s top insurers. Get your free expat insurance quote today and secure the peace of mind you deserve.