The average expat medical insurance cost lands around $2,500 per year for an individual, but that’s just a starting point. The real price can swing…

The average expat medical insurance cost lands around $2,500 per year for an individual, but that’s just a starting point. The real price can swing from as low as $1,000 to well over $10,000. Where you land on that spectrum depends almost entirely on your age, where you’re moving, and the level of medical coverage you need.

What Does Expat Medical Insurance Typically Cost?

Figuring out the cost of expat medical insurance can feel like trying to hit a moving target. While industry averages give you a ballpark figure, your personal situation is what really drives the final premium. Think of it like buying a car—the sticker price changes fast once you decide on the model, engine size, and all the extra features.

The core idea is simple: your cost is unique to you. It really boils down to three main variables:

- Your Age and Health: Just like any other insurance, premiums tend to climb as you get older.

- Your Destination: This is a big one. Medical care costs vary wildly across the globe. Getting covered in the USA or Singapore will be far more expensive than in Thailand or Mexico.

- Your Plan Choices: A bare-bones, hospital-only plan will naturally cost much less than a comprehensive policy that includes outpatient care, dental, and vision.

Based on 2025 data, the average annual premium for an individual expat medical plan is about US$2,517. This number typically reflects a standard plan that balances emergency coverage with some routine outpatient care, but it’s critical to remember this is just a midpoint.

Costs can shift dramatically based on the factors I just mentioned. For a complete breakdown, check out our international medical insurance cost guide.

Your insurance premium isn’t a random number pulled from a hat. It’s a carefully calculated reflection of your personal risk profile and the cost of medical care in your chosen destination.

Getting a handle on these key drivers is the first step to setting a realistic budget. Before we dive deeper into each factor, here’s a quick summary to give you a clearer picture.

A Quick Look At Expat Medical Insurance Costs

This table gives you a general idea of what to expect for annual premiums based on different levels of medical coverage. It’s a great way to see how your choices can impact the final price.

| Plan Type | Typical Annual Cost Range (Individual) | Primary Influencing Factors |

|---|---|---|

| Basic (Inpatient Only) | $1,000 – $3,500 | Age, Destination (Excluding USA) |

| Standard (Inpatient + Outpatient) | $2,500 – $6,000 | Age, Destination, Deductible |

| Premium (Comprehensive) | $5,000 – $12,000+ | Age, Destination (Worldwide), Benefits |

As you can see, the jump from a basic plan to a premium one is significant, but so is the level of protection and peace of mind you get. The key is to find the right balance for your needs and budget.

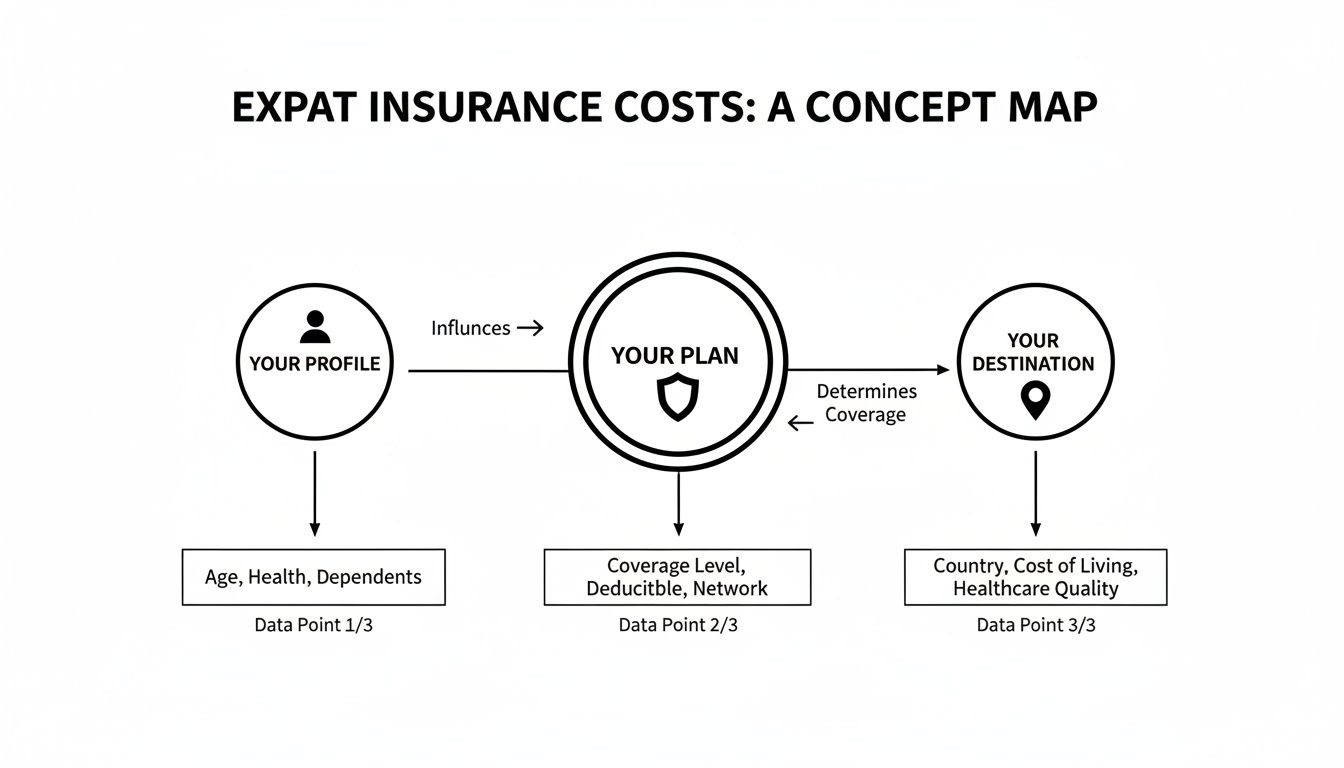

The 6 Factors That Drive Your Premium

Figuring out the cost of expat medical insurance is a bit like booking a flight. You and the person in the next seat could be paying wildly different prices based on when you bought your ticket, where you’re sitting, and what extras you added on. Your insurance premium works the same way—it’s built from a few core components that insurers piece together to arrive at your final price.

Once you get a handle on these six factors, you’ll start to see exactly how your choices pull the levers on your premium. It puts you in the driver’s seat, allowing you to find that sweet spot between rock-solid medical coverage and a price that fits your budget.

This chart breaks down how your personal profile, your destination, and your plan choices all feed into the final number.

As you can see, it really boils down to three things: who you are, where you’re going, and what kind of plan you build. Let’s dig into each one.

1. Your Age and Health

This is the big one, and it’s the most straightforward. For an insurer, age is the clearest indicator of health risk. It’s just a statistical reality: as we get older, we’re more likely to need medical care.

That’s why a premium for a 60-year-old expat will be significantly higher than for a 30-year-old, even if they have the exact same plan. Your health history also plays a part. While many modern plans cover pre-existing conditions, a complex medical background might mean a higher starting premium.

2. Your Destination Country

Where you choose to live has a massive impact on your insurance cost—arguably more than any other factor. Medical care costs are wildly different from one country to the next.

Think about it: a top-tier plan that provides fantastic coverage in a place like Thailand would barely make a dent in medical bills in the United States, which is globally recognized as the most expensive place for healthcare. Insurers have to price this reality into their plans.

To manage this, they offer different geographic coverage areas:

- Worldwide: Covers you absolutely everywhere. It’s the most comprehensive and the most expensive.

- Worldwide Excluding the USA: This is a hugely popular option. It gives you global freedom but cuts out the sky-high costs of U.S. healthcare, making it far more affordable.

- Regional Plans: If you know you’ll be sticking to one part of the world, like Europe or Southeast Asia, these plans offer even more savings by limiting coverage to that specific zone.

3. Your Plan’s Structure

This is where you have the most control. The nitty-gritty details of the plan you choose—your benefits, limits, and cost-sharing options—will directly shape your final premium.

4. Your Level of Coverage

A bare-bones, inpatient-only plan (which covers you if you’re admitted to a hospital) is going to be your cheapest option. If you start adding outpatient services like regular doctor visits, prescriptions, and diagnostic tests, the price will climb.

The type of medical network your plan uses matters, too. Understanding the trade-offs between a PPO vs. an HMO for expats can help you decide what level of flexibility you need and how much you’re willing to pay for it.

5. Your Deductible

A deductible is the amount of money you agree to pay out-of-pocket for your care before your insurance company starts paying. This is a lever you can pull to directly influence your premium.

Choosing a higher deductible is a simple trade-off. By taking on more of the initial financial risk yourself, you can significantly lower what you pay for the plan on a monthly or annual basis. Opting for a $2,500 deductible instead of $500, for example, can lead to dramatic savings.

6. Your Optional Benefits

Finally, you can customize your plan with add-ons. Need dental and vision coverage? Planning to start a family and need maternity benefits? Each of these will increase the total cost.

The key is to be realistic about what you’ll actually need. These add-ons provide crucial protection for specific services, but they aren’t free.

How Different Choices Impact Your Annual Premium

To see how these moving parts fit together, let’s look at how different decisions can swing the annual premium for a hypothetical 40-year-old expat.

| Factor | Lower Cost Option | Higher Cost Option | Estimated Impact |

|---|---|---|---|

| Location | Living in Portugal (Worldwide ex. USA) | Living in the USA (Worldwide) | +200% to 400% |

| Coverage Level | Inpatient-Only (Hospitalization) | Comprehensive (Inpatient + Outpatient) | +75% to 150% |

| Deductible | $5,000 Annual Deductible | $250 Annual Deductible | +40% to 80% |

| Add-Ons | No Dental or Vision | Dental & Vision Benefits Included | +15% to 30% |

As the table shows, a single choice—like needing coverage in the USA—can multiply your costs. By understanding these levers, you can build a plan that truly matches both your healthcare needs and your financial reality.

Expat Medical Insurance Costs Around The World

The factors that drive your premium don’t exist in a vacuum. They come to life in the real world, creating wildly different costs depending on where you decide to plant your flag.

Your destination is easily the single biggest variable in the equation. Why? Because the local price of private medical care sets the baseline for what insurers have to charge. An identical plan can genuinely cost four times as much in one country as it does in another.

Let’s make this concrete by walking through some realistic scenarios. We’ll look at the annual expat medical insurance cost for a 35-year-old individual and a family of four (two adults, two children) across a few high, mid, and low-cost regions. These numbers are solid estimates for a standard plan offering good inpatient and outpatient coverage.

High-Cost Destinations: The USA and Singapore

Countries like the United States and Singapore sit at the very top of the pricing pyramid. The U.S. is notoriously the most expensive healthcare market on the planet, and with no public options available to most expats, private medical insurance isn’t just a good idea—it’s essential. The premiums absolutely reflect that reality.

Singapore, on the other hand, is known for its world-class (and equally pricey) private medical system.

- Single Expat (Age 35): In the USA, a comprehensive plan will easily run you $12,000 to $16,000 a year. In Singapore, you can expect to pay between $6,500 and $8,500.

- Family of Four: The costs multiply fast. A family in the U.S. could be looking at premiums of $30,000 to $35,000+. In Singapore, that same family might budget $19,000 to $24,000 annually.

The reason for these eye-watering figures is simple: the underlying cost of a doctor’s visit, a hospital stay, or a prescription is exceptionally high. Insurers have to price their plans to cover those potential expenses.

Mid-Range Countries: Spain and The UAE

Next up are popular expat hubs like Spain and the United Arab Emirates, specifically Dubai. These spots boast excellent private medical infrastructure but at a more manageable price point than the top tier. Both countries also have mandatory health insurance requirements for residents, which helps shape a competitive market.

When you’re tallying up your potential expat medical insurance cost, it’s also smart to look at the bigger picture, including the overall cost of living in the best European cities for expats. This gives you a much clearer financial forecast for your move.

- Single Expat (Age 35): In Spain, a solid plan would likely set you back $4,500 to $6,000. In Dubai, the range is quite similar, typically from $5,000 to $6,500.

- Family of Four: A family premium in Spain would land somewhere between $14,000 and $17,000, while in Dubai, it might be a bit higher at $16,000 to $18,000.

Key Takeaway: Your choice of country translates directly to your insurance bill. Researching the local private medical system of a potential destination is every bit as important as looking into visa rules or housing costs.

Affordable Locations: Mexico and Thailand

Finally, we have countries like Mexico and Thailand, which offer quality private healthcare at a fraction of the cost you’d find elsewhere. This makes them incredibly attractive to retirees, digital nomads, and other budget-conscious expats. The affordability of medical care there directly pushes insurance premiums down.

- Single Expat (Age 35): You could find excellent coverage in Mexico for $4,000 to $5,500 annually. In Thailand, the price is even more competitive, often falling between $3,500 and $5,000.

- Family of Four: For a family, a plan in Mexico might cost $13,000 to $16,000. In Thailand, a family could expect to pay anywhere from $14,000 to $18,000, with costs varying based on the quality of international hospitals included in the network.

These examples really drive the point home—geography dictates the price. A plan that’s considered premium in Thailand might not even cover the basics in the United States.

Why Your Insurance Bill Is Likely To Increase

It’s a frustrating reality for pretty much every expat: your renewal premium is almost always higher than the last one. This annual price hike isn’t some arbitrary decision your insurer cooked up. Instead, it’s a direct reflection of powerful global trends in healthcare that are pushing up the expat medical insurance cost for everyone.

Once you understand these forces, the increase feels less like a personal penalty and more like a reaction to an evolving—and increasingly expensive—global medical landscape. Seeing the bigger picture makes planning your long-term budget a whole lot easier.

The Engine of Rising Costs: Medical Inflation

The main driver behind rising premiums is medical inflation. Think of it as the healthcare version of regular inflation, only on steroids. It represents the ballooning cost of medical services, technology, and treatments, and it consistently outpaces general economic inflation, year after year.

This happens for a few key reasons:

- Advanced Medical Technology: Incredible new diagnostic tools, surgical robots, and innovative therapies are changing the game, but they come with hefty price tags.

- New Prescription Drugs: Breakthrough medications, especially for complex conditions, can cost thousands of dollars per dose. Insurers have to adjust their pricing to cover these powerful but pricey treatments.

- Higher Demand for Services: As global populations age and health awareness grows, more people are seeking medical care. This increased demand, especially in the post-pandemic era, puts upward pressure on prices for everything from a simple check-up to major surgery.

This relentless upward trend is a global phenomenon. In fact, these soaring healthcare costs are fueling double-digit rises in expat health insurance premiums worldwide. A recent industry analysis projects a 10.3% average hike for 2026, right on the heels of increases of 10% in 2025 and 9.5% in 2024. This data, based on surveys of hundreds of insurers across 82 countries, really underscores the persistent financial pressure of medical inflation. You can learn more about these global medical trends and their direct impact on insurance pricing.

Your annual premium increase is less about your personal health and more about the rising cost of providing quality medical care to everyone on a global scale.

Planning for Predictable Increases

While you can’t stop medical inflation, you can definitely anticipate it. When budgeting for your life abroad, it’s smart to factor in an annual premium increase of around 8% to 10%. Doing this prepares you for renewal time and helps you avoid sticker shock.

By understanding that your expat medical insurance cost is tied to these large-scale economic forces, you can better plan your finances. It also helps you see your policy for what it truly is: a shield against predictably rising healthcare expenses.

Proven Strategies To Lower Your Expat Insurance Bill

Figuring out what drives your premium up is one half of the equation; the other is knowing how to actually do something about it. While you can’t exactly halt global medical inflation, you have a surprising amount of control over your policy and, by extension, your expat medical insurance cost. A few smart adjustments can lead to some serious savings without leaving you dangerously underinsured.

Think of your policy less like a fixed, off-the-shelf product and more like a plan you can customize. By tweaking a few key levers, you can strike that perfect balance between solid medical protection and a premium that doesn’t break the bank. Let’s walk through five proven ways to bring that bill down.

1. Opt for a Higher Deductible

This is one of the quickest and most direct ways to lower your premium. A deductible is simply the amount you agree to pay out-of-pocket for your medical care before the insurance company starts to pay.

By choosing a higher deductible, you’re essentially telling the insurer you’ll handle the smaller stuff, which reduces their immediate risk. They reward you for this with a lower annual premium. For example, just increasing your deductible from $500 to $2,500 could easily slice 20-30% off your yearly cost.

2. Adjust Your Geographic Coverage Area

Here’s a big one: healthcare costs in the USA are in a league of their own, a fact that dramatically bloats insurance premiums. If you don’t plan on living in or traveling frequently to the United States, selecting a “Worldwide excluding USA” plan is a game-changer.

This single move can often slash your premium by 40% or more, making it one of the most powerful cost-saving decisions you can make. On a similar note, if you know you’ll be sticking to one region, a plan covering just Europe or Asia will offer even more savings.

Your premium is a direct reflection of risk. By removing the highest-cost healthcare market from your coverage area, you significantly lower the potential financial risk for the insurer, and they pass those savings on to you.

3. Pay Your Premium Annually

Insurers often tack on small processing fees for monthly or quarterly payment plans. These little charges might not seem like much on their own, but they absolutely add up over the course of a year.

Choosing to pay your entire premium in one lump sum annually usually gets rid of these fees. It’s a simple administrative switch that could save you 5-8% on your total cost for the year.

4. Review and Remove Unnecessary Benefits

It’s tempting to go for the all-inclusive plan with every bell and whistle, but do you really need everything? Take a hard look at optional benefits like premium dental, vision, or maternity coverage.

If you’re a single male expat, for example, maternity benefits aren’t doing you any good. Trimming just one or two of these add-ons can make a noticeable dent in your premium. You can find more ideas for building a lean-but-effective policy in our guide to affordable international health insurance.

5. Maintain a Healthy Lifestyle

This last strategy is more of a long-term play, but it’s incredibly effective. Being proactive about your well-being naturally leads to fewer health problems and, over time, a much better risk profile in the eyes of an insurer.

Taking steps to understand and manage your health, for instance by exploring options like at-home health testing for longevity, can provide valuable insights into your wellness. A clean bill of health makes you a more attractive applicant, which is your best leverage for securing better rates when it’s time to renew.

How To Get An Accurate Insurance Quote For Your Needs

You’ve got the basics down—you know the factors, you’ve seen the price ranges, and you have a few tricks up your sleeve to lower your premium. Now it’s time to move from theory to reality and get a personalized quote that truly reflects your unique situation and the real expat medical insurance cost you can expect.

While online calculators are great for a ballpark figure, they simply can’t capture the full picture of your life abroad. A tailored quote is the only way to build a realistic budget and avoid nasty surprises later on. This is where you need to go beyond the generic tools and get some specialized advice.

This is exactly why working with an insurance broker who lives and breathes the expat world is such a game-changer. Instead of spending hours researching dozens of providers yourself, a good broker does the heavy lifting. They’ll scan the entire market to find plans that perfectly match your health needs, budget, and destination.

What You Will Need To Provide

To get the most accurate quote possible, you’ll need to have some information ready. Think of it as giving the broker or insurer the raw materials they need to build a precise picture of your needs and calculate a premium that’s right for you.

Be prepared to share the following:

- Personal Information: This is the simple stuff—your full name, date of birth, and the details for any family members you want to cover.

- Destination and Coverage Area: Get specific. Name your primary country of residence and mention if you’ll need coverage in other regions, especially the USA, which can significantly change the cost.

- Desired Coverage Level: Have an idea of what you want. Are you looking for basic inpatient-only care, or do you need comprehensive outpatient services? Don’t forget to mention specific add-ons like dental or maternity benefits.

Comparing Your Quotes Fairly

Once the quotes start rolling in, it’s tempting to just glance at the final price. Don’t do it. To make a smart decision, you have to dig into the details and ensure you’re making a true apples-to-apples comparison.

A lower price often means a higher deductible or fewer benefits. Your goal is to find the best value—the right balance of comprehensive coverage and affordability—not just the cheapest option.

When you’re looking at different plans, check the annual limits, the deductible amounts, and the specific list of what’s actually covered. A plan that seems like a bargain at first might have a low coverage cap or exclude a benefit that’s a must-have for you. Taking the time to compare these details ensures you end up with a policy that gives you genuine peace of mind and solid financial protection for your new life abroad.

Ready to find the perfect plan for your life abroad? The team at Expat Global Medical has been helping expats secure reliable and affordable international health insurance since 1992. Get a free, personalized quote today and let our experts guide you to the right coverage. Get Your Free Expat Insurance Quote from Expat Global Medical

1 Comment

Comments are closed.