Living abroad is one of life’s great adventures, but it comes with a critical question that too many Americans overlook: what about health insurance? It’s…

Living abroad is one of life’s great adventures, but it comes with a critical question that too many Americans overlook: what about health insurance?

It’s a costly mistake to assume your domestic health plan will cover you once you’re on foreign soil. The hard truth is that most U.S. insurance, including Medicare and ACA plans, offers little to no protection outside the United States. This is where specialized expat medical insurance comes in—it’s not just a nice-to-have, it’s an absolute necessity.

Your Guide To Expat Health Insurance While Living Abroad

Stepping into expat life is thrilling, but figuring out healthcare can feel like a maze. The biggest trap for Americans is thinking their health insurance card is like a credit card—that it’ll just work everywhere.

Unfortunately, it won’t.

Your U.S. health plan is built for the U.S. healthcare system. The moment you establish a life abroad, that safety net effectively vanishes. A sudden illness or an unexpected accident could leave you facing staggering medical bills, turning your dream into a financial nightmare.

That’s exactly why expat medical insurance for Americans living abroad exists. It’s not a luxury item; it’s the foundation for a secure and successful life overseas. This guide is your roadmap to getting it right.

Understanding The Need For Specialized Expat Coverage

This isn’t your average travel insurance, which is designed for short trips and unexpected emergencies. Long-term expat health insurance is meant to be your primary medical plan abroad, covering everything from routine doctor’s visits to serious hospitalizations.

And the need for it is growing. The global expat medical insurance market is already valued at around USD 331 million in 2024 and is set to climb, thanks to a global expat community of roughly 87 million people.

After the pandemic, something shifted. Surveys found that a staggering 67% of expats now rank comprehensive medical coverage as their number one concern when relocating. This sharp increase shows just how much people are realizing the importance of solid, dependable expat health plans. You can review the full market research about expat insurance trends to see this shift for yourself.

Think of it this way: You wouldn’t use your local library card in another country and expect it to work. Similarly, your U.S. health plan isn’t recognized by international healthcare systems.

What This Guide Will Cover

We’re going to break it all down for you, step by step. We’ll start by digging into why your U.S. plan just won’t cut it and then compare the different types of international and expat plans you can choose from.

You’ll learn how to read the fine print on policies—from deductibles and co-pays to medical evacuation—and get a simple checklist to make sure you’re picking coverage that truly gives you peace of mind. Our goal is to give you the confidence to choose an expat medical insurance plan that lets you focus on what really matters: building an amazing life in your new home.

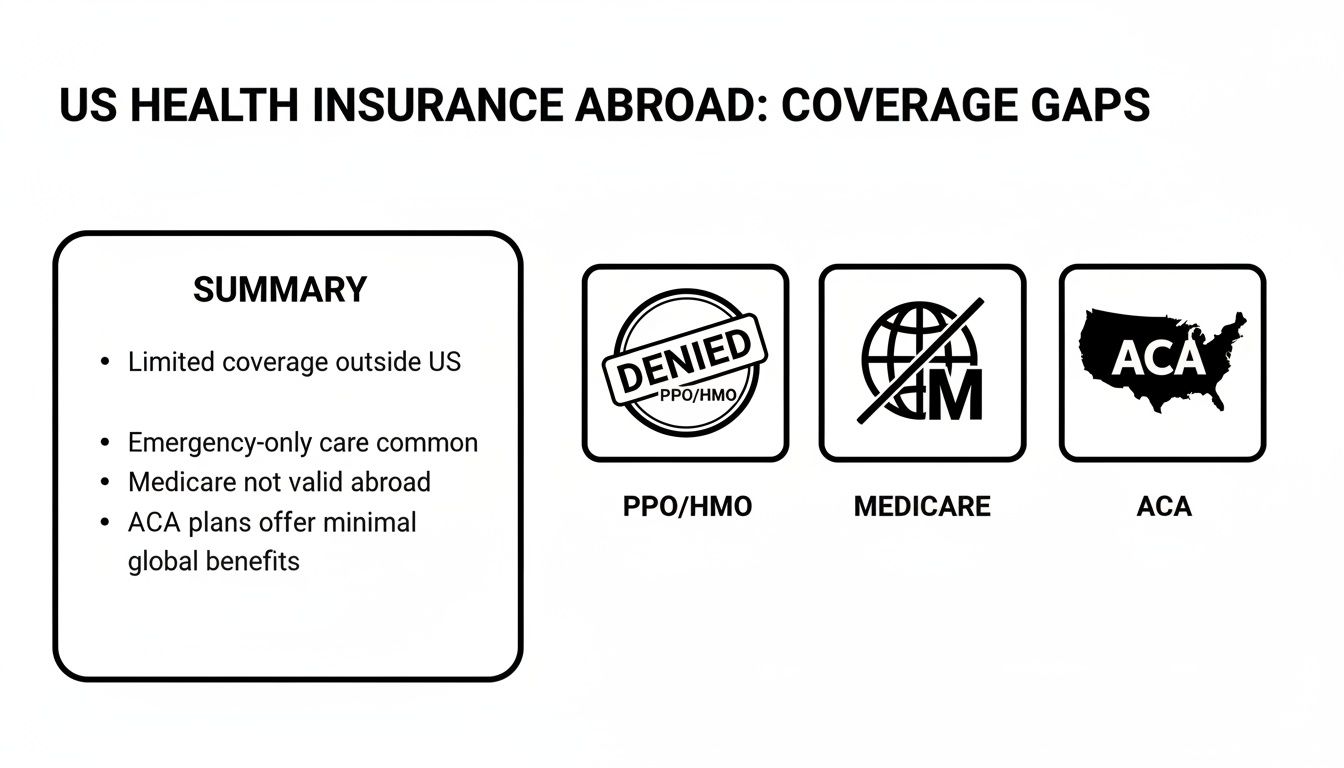

Why Your US Health Insurance Falls Short Overseas

Trying to use your U.S. health plan while living abroad is a bit like showing up with a local library card in another country—it’s just not part of their system and won’t get you access when you need it most. This common mistake can have devastating financial consequences, quickly turning a manageable health issue into a full-blown crisis.

The heart of the problem is that U.S. health insurance networks, whether you have a PPO or an HMO, are designed for the American healthcare system. That means hospitals and clinics overseas are almost always considered “out-of-network.”

What does that mean for you? Your insurer has no direct payment agreements with these providers. You’ll likely have to pay the entire medical bill upfront, out of pocket, and then cross your fingers for a partial reimbursement later—if you get one at all. Many domestic plans will simply deny claims for services you receive outside the United States, period.

The Myth Of Medicare Coverage Abroad

For American retirees, one of the most dangerous assumptions is thinking Medicare will follow them overseas. This is flat-out wrong.

Medicare provides no coverage for healthcare services you receive outside the United States, except in a few incredibly rare and specific situations (like being on a cruise ship within six hours of a U.S. port).

Relying on Medicare for your healthcare while living in another country means you are effectively uninsured. It is not a safety net and will not protect you from the high costs of medical care in your new home.

This leaves a huge protection gap for the millions of retirees who decide to spend their golden years in another country. Without a proper expat medical insurance plan, you are on the hook for every single dollar of your medical bills, from a routine check-up to complex surgery.

ACA Plans Are For US Residents Only

The Affordable Care Act (ACA), often called Obamacare, was a major step forward for healthcare in the U.S. However, its protections and benefits were created exclusively for residents of the United States.

These plans do not extend coverage globally. Once you’re no longer a resident of the state where you bought your plan, you typically lose your eligibility for that coverage. It’s a critical detail that many Americans overlook when planning their move. You can dig deeper into the specifics of why U.S. health insurance doesn’t work abroad in our detailed guide.

Portability Gaps and The Clear Need For Expat Insurance

The way U.S. insurance is structured creates massive coverage gaps for Americans who move abroad. While employer-sponsored plans covered roughly 154 million people in the United States in recent years, these plans rarely offer guaranteed or full international portability for long-term expat assignments.

This is a fundamental limitation that leaves millions of Americans abroad in need of specialized expat medical insurance for Americans living abroad. The need is only made more urgent by the fact that American healthcare costs are so much higher than in most other countries, making U.S.-based coverage both wildly expensive and impractical for an expat. You can discover more insights about these U.S. health system trends.

This all builds an undeniable case for a purpose-built expat health plan. It’s not an optional upgrade or a luxury—it’s an essential layer of security for any American living abroad, ensuring you get quality care without putting your financial future on the line.

Comparing Your International & Expat Insurance Options

Trying to figure out insurance options can feel like learning a new language, filled with confusing terms and small but important differences. To make the right call, you need to understand the main types of plans available for American expats. Each one serves a very different purpose, and picking the wrong one could leave you with some serious—and expensive—coverage gaps.

Think of it like choosing a vehicle for a trip. You wouldn’t take a sports car on a rugged mountain trail, and you definitely wouldn’t use a bicycle for a cross-country road trip. In the same way, the insurance you need depends entirely on how long you’ll be gone and what you’ll be doing overseas.

First, let’s be clear about one thing: your U.S. health plan probably won’t cut it. This visual shows why your stateside PPO, HMO, and Medicare plans are not built for the global journey you’re on.

As you can see, domestic plans have geographic boundaries that pretty much stop at the U.S. border, making specialized expat coverage a must-have.

Short-Term Travel Medical Insurance

Short-term travel medical insurance is like a first-aid kit for your trip. It’s designed for a specific, limited time—usually anywhere from a few days up to a year—and isn’t meant for someone actually living abroad.

Its main job is to cover unexpected medical emergencies that might pop up while you’re away. This could be anything from a sudden illness to an accidental injury that needs immediate medical attention.

But it’s just as important to understand what it doesn’t do. These plans almost always exclude routine check-ups, preventive care, and pre-existing conditions. They are a temporary safety net, not a substitute for real health insurance.

Best for:

- Tourists and vacationers on trips lasting less than one year.

- Business travelers on short-term international assignments.

- Expats who are in between long-term plans and just need to fill a temporary gap.

Long-Term Expat Health Insurance

Now we’re talking. This is the main event: a comprehensive, renewable medical plan designed to be your primary health coverage while living in another country. Unlike short-term plans, long-term expat health insurance is built for the realities of day-to-day life abroad.

It covers a huge range of healthcare needs, from emergency hospital stays to routine doctor visits, specialist appointments, and prescription drugs. These plans are medically underwritten, can be renewed every year, and often let you add on extras like dental, vision, and mental health coverage.

Think of an expat health plan as your home country’s health insurance, but with a global passport. It’s designed to provide solid, day-to-day medical security no matter where you call home.

This is the right choice for expat medical insurance for Americans living abroad for the long haul. Depending on your destination, you might also run into specific local plans for non-residents, like Australia’s Overseas Visitors Health Cover (OVHC), which can sometimes supplement a global expat plan.

Medical Evacuation Plans

A medical evacuation (or “medevac”) plan is a very specific but incredibly important piece of the puzzle. This insurance focuses on one thing and one thing only: getting you to a place with adequate medical care in a serious emergency.

Imagine you’re in a remote village or a country where the local hospitals just can’t handle your severe injury or illness. A medevac plan covers the massive cost—often over $50,000—of transporting you to the nearest quality hospital or even flying you all the way back to the United States.

It’s crucial to know that this is not health insurance; it won’t pay your hospital bills once you get there. Instead, it’s often bought as a separate policy or included as a vital feature in a good long-term expat health plan.

To help you visualize how these different insurance types fit together, take a look at the table below. It breaks down their core features side-by-side.

Comparing Insurance Types for Americans Abroad

This table contrasts the primary features of Short-Term Travel, Long-Term Expat, and Medical Evacuation insurance to help you choose the right type for your needs.

| Feature | Short-Term Travel Medical | Long-Term Expat Medical | Medical Evacuation Plan |

|---|---|---|---|

| Primary Purpose | Emergency medical for trips under one year | Comprehensive, primary health coverage for living abroad | Emergency transport to an adequate medical facility |

| Duration | Days to 12 months; non-renewable | Annually renewable; designed for long-term stays | Typically annual; can be standalone or part of another plan |

| Routine Care | No (Excludes check-ups, physicals) | Yes (Covers doctor visits, preventive care, prescriptions) | No (Transportation only) |

| Pre-Existing Conditions | Typically excluded | Often covered, subject to underwriting | No (Medical transport, regardless of condition) |

| Best For | Tourists, business travelers, temporary visitors | Expats, digital nomads, global retirees, international families | Anyone living or traveling in areas with limited medical care |

| Medical Bills Covered? | Yes, for emergencies | Yes, for a wide range of medical services | No, only covers the cost of transportation |

Choosing the right plan really comes down to matching the coverage to your lifestyle and the length of your stay abroad. For a complete breakdown, you can review our detailed international health insurance comparison guide, which breaks down the features of leading plans. This direct comparison helps clarify which policy aligns best with your specific needs.

Decoding The Features Of A Strong Expat Health Plan

Once you’ve zeroed in on the right type of plan for your life abroad, it’s time to look under the hood. Not all expat policies are built the same, and the real value is always hiding in the fine print. Think of this as your personal checklist for spotting a quality expat medical policy that won’t let you down.

Getting a handle on these features is what separates a smart purchase from a costly mistake. It gives you the confidence to compare your options and find a plan that delivers genuine security, not just a fancy brochure.

Area Of Coverage: Your Geographic Safety Net

One of the first things you’ll run into is the Area of Coverage. This simply defines the geographic boundaries of your insurance policy. Some plans are regional, covering you in, say, Southeast Asia, while others offer truly global protection.

For many American expats, a “Worldwide excluding US” policy is the sweet spot. This plan covers you anywhere on the planet except for the United States. Why would you want that? It’s all about cost. The sky-high price of U.S. healthcare is the single biggest factor that inflates insurance premiums. By carving out the U.S., you can often slash your monthly costs while still getting top-tier care everywhere else.

And if you plan on making regular trips back home, you’re not stuck. You can either opt for a full worldwide plan from the start or, more commonly, add a rider that provides limited, short-term coverage for your visits to the States. This kind of flexibility is a trademark of good expat medical insurance for Americans living abroad.

Inpatient Vs. Outpatient Care

Understanding the difference between inpatient and outpatient services is crucial to reading any health insurance policy. They basically represent two different levels of medical attention.

- Inpatient Care: This is the big stuff. It covers any treatment that requires you to be formally admitted to a hospital, like surgery or a serious illness that needs overnight observation. It’s the kind of care you hope you never need, but you absolutely have to be covered for it.

- Outpatient Care: This is everything else—any medical service that doesn’t require a hospital admission. Think doctor’s appointments, visits to a specialist, lab work, physical therapy, and prescription drugs. The most comprehensive expat plans cover both, but more basic, catastrophic-style policies might focus only on inpatient care to keep the price down.

It’s also important to see how your policy handles the provider network. Knowing if you can go to any doctor or if you need to stick to a specific list is a big deal. You can get the full rundown in our guide to understanding international health networks for expats.

Deductibles And Co-Insurance

These two terms define how much of the medical bill you’ll be responsible for. They’re the levers you can pull to adjust your monthly premium.

A deductible is the fixed amount you pay out-of-pocket for covered services before your insurance plan kicks in. If your plan has a $1,000 deductible, you pay the first $1,000 of your medical bills for the year. Simple as that.

Co-insurance comes into play after you’ve paid your deductible. It’s a percentage split of the remaining costs. A common arrangement is 80/20, where the insurance company pays 80% and you pay 20%. Choosing a higher deductible is a popular way to lower your monthly premium, but just make sure it’s an amount you could comfortably cover if a medical issue pops up unexpectedly.

The Non-Negotiable: Emergency Medical Evacuation

For any American living abroad, Emergency Medical Evacuation is an absolute, non-negotiable must-have. Period. If you suffer a serious injury or fall ill in a place that can’t provide the care you need, this benefit covers the staggering cost of transporting you to the nearest hospital that can.

This isn’t a luxury feature; it’s a financial lifeline. A medical evacuation can easily top $50,000, which is enough to wipe out most people’s savings. It’s no surprise that medevac and emergency medical costs are among the most frequent and expensive claims filed by Americans overseas. In 2024 alone, U.S. Travel Insurance Association members provided coverage to nearly 87 million people, reflecting a huge jump in demand since before the pandemic.

A strong expat health plan isn’t just about paying for a doctor’s visit. It’s a comprehensive system designed to protect your health and finances, from a routine check-up in Berlin to an emergency evacuation from a remote island.

Finally, you’ll want to check for other important details, like how the plan handles pre-existing conditions and whether you can add valuable extras like dental and vision care. By carefully weighing each of these components, you can look past the price tag and choose an expat plan that delivers true peace of mind.

Choosing The Right Expat Medical Insurance Plan For You

Alright, now that you’ve got a handle on the key features of different expat policies, it’s time to land the plane. This is where you connect all that knowledge to your own life and find the plan that feels like it was made just for you.

Think of it as building a custom safety net. The right plan for a digital nomad bouncing around Southeast Asia is going to look completely different from what a retiree settling down in Mexico needs. This last step is all about asking the right questions to pinpoint the perfect expat medical insurance for Americans living abroad.

Your Personal Expat Insurance Checklist

Before you even start looking at providers, grab a notebook and answer these questions. Your answers will act as a filter, cutting through the noise and making your final choice a whole lot easier.

- How long will I be abroad? Is this a one-year work assignment, or have you moved for good? The length of your stay is the biggest factor in deciding between a short-term travel plan and a long-term, renewable expat policy.

- What is my host country’s healthcare system like? Do your homework here. Can expats even use the public system? Are the private hospitals the go-to for quality care? If you’re moving somewhere with amazing but pricey private healthcare, a plan with a lower deductible might be a priority to keep your out-of-pocket costs down.

- Do I need coverage for visits back to the US? If you plan on flying home for holidays or family visits, you’ll need a policy that either includes worldwide coverage with the U.S. or offers a specific add-on for it. Be honest with yourself about how often you’ll be back to avoid a nasty surprise.

- What is my realistic budget? Figure out what you can genuinely afford each month or year for a premium. Don’t forget, you can often tweak your deductible and co-insurance levels to hit a price point that works for you without gutting your essential coverage.

- What are my personal health needs? Do you have any pre-existing conditions? Are you planning on starting a family and need maternity care? Think about the specific kinds of care you might need—this is critical for choosing a plan with the right benefits.

Weighing The Factors For Your Situation

Once you have your answers, you can start weighing what features matter most. It’s a balancing act, and your personal situation is the guide.

For instance, if you’re moving to a remote area with only basic local clinics, a plan with a high limit for emergency medical evacuation should be at the top of your list. In that scenario, evacuation coverage is far more important than, say, routine dental cleanings.

On the other hand, someone relocating to a major European hub like Berlin or Paris might not worry as much about evacuation. Their focus would likely be on finding a plan with a great local network of English-speaking doctors for easy, day-to-day care.

The best expat insurance plan isn’t the one with the most features; it’s the one with the right features for your specific life. Prioritize what protects you most based on where you are and how you live.

How To Vet Your Insurance Provider

Okay, you’ve narrowed it down to a shortlist of plans that seem like a good fit. The final piece of the puzzle is to check out the companies behind them. A fantastic policy is useless if the provider is a nightmare to deal with.

Here’s what to look for in a reliable insurer:

- A Strong Hospital Network: Don’t just take their word for it—look up their list of in-network hospitals and clinics in your new home country. A deep network gives you more choice and makes direct billing (where the hospital bills the insurer directly) much more likely. That saves you from having to pay a massive bill upfront.

- An Efficient Claims Process: This is where reviews from other expats are gold. How easy is it to file a claim? More importantly, how quickly do they get their money back? A company known for dragging its feet on reimbursements is a huge red flag.

- Quality 24/7 Multilingual Support: Medical emergencies don’t stick to a 9-to-5 schedule. You absolutely need to know that you can get a real, helpful person on the phone—in your own language—no matter the time of day. This is non-negotiable.

Common Questions About Expat Medical Insurance

Let’s be honest, figuring out health insurance for a life abroad can feel overwhelming. You’ve probably got a dozen questions running through your mind as you plan your move. We get it.

To help clear things up, we’ve put together answers to the most common questions we’ve heard from Americans just like you. Think of this as your quick-start guide to understanding the essentials of expat insurance.

Can I Just Use My ACA Plan Overseas?

This is one of the first questions people ask, and the answer is a straightforward no, you generally can’t. Plans purchased through the Affordable Care Act (ACA) marketplace are designed for U.S. residents and rely on networks of doctors and hospitals located within the United States.

Once you establish residency in another country, you typically lose your eligibility for that plan. The subsidies, protections, and benefits are tied to your U.S. residency and simply don’t follow you abroad.

Will Medicare Cover Me When I Retire Abroad?

For retirees, this is a big one. It’s crucial to understand that Medicare provides virtually zero coverage for healthcare you receive outside the United States.

While there are a few incredibly specific and rare exceptions, they don’t apply to the vast majority of expats. If you move abroad and rely on Medicare as your primary health plan, you are effectively uninsured. This leaves you completely exposed to the full cost of any medical care you might need in your new home.

It’s a hard truth, but an essential one to grasp: Medicare is a domestic program. To truly secure your health and finances in retirement abroad, a dedicated expat health plan isn’t just a good idea—it’s a necessity.

Do I Still Need Insurance if My New Country Has National Healthcare?

That’s a great question, and it shows you’re thinking ahead. Even in countries with excellent public healthcare systems, a private expat medical insurance plan is a smart (and often necessary) move for a few key reasons:

- Eligibility & Immediate Access: As a newcomer, you might not be eligible for the public system right away. A private plan ensures you have solid coverage from day one, with no gaps or waiting periods.

- Bypassing the Queues: Even the best public systems can have long wait times for specialist appointments or non-emergency procedures. Private insurance usually gives you access to a network of private clinics and hospitals, letting you get seen much faster.

- Filling in the Gaps: National health plans don’t always cover everything. Things like dental, vision, and certain prescription drugs might be excluded. A private plan can fill in those gaps.

- The Big One: Medical Evacuation: This is a critical benefit. A public system won’t pay to fly you to another country for better care or transport you back to the U.S. in a severe emergency. Only a private plan with evacuation coverage offers this vital protection.

In short, while a country’s national health system is a fantastic asset, a private expat plan provides a higher level of choice, speed, and security.

What’s the Difference Between Evacuation and Repatriation?

These two terms sound similar, but they cover very different—and equally vital—scenarios. Getting the distinction is key to understanding what your expat policy actually protects you from.

Medical Evacuation is about getting you to the best possible care. It covers transporting you from a place with inadequate medical facilities to the nearest center of medical excellence equipped to handle your condition. For instance, if you were seriously injured while hiking in a remote part of Peru, evacuation would pay to fly you to a top-tier hospital in Lima. The goal is simple: get you the right care, fast.

Repatriation of Remains, on the other hand, is a benefit that covers the cost of transporting your body back to your home country if you pass away abroad. This is a logistically complex and emotionally taxing process for a family to handle, not to mention expensive. This coverage removes that heavy burden from your loved ones during an already difficult time.

Both are critical parts of any robust expat medical insurance for Americans living abroad, providing peace of mind for worst-case scenarios.

Ready to find the right medical insurance for your new life? The team at Expat Global Medical has been helping Americans secure their health and finances overseas since 1992. We partner with the world’s top insurance carriers to offer personalized advice and find an expat plan that fits your specific needs and budget.

Get Your Free International Health Insurance Quote from Expat Global Medical and take the first step toward true peace of mind.