Picture this: a serious medical emergency hits while you’re living abroad, and the local hospital just doesn’t have the resources to give you the life-saving…

Picture this: a serious medical emergency hits while you’re living abroad, and the local hospital just doesn’t have the resources to give you the life-saving care you need. This is where medical evacuation insurance becomes your emergency exit plan. It’s a specialized policy designed purely to get you from an inadequate facility to one that can provide the best possible care, whether that’s in a neighboring country or all the way back home.

Your Lifeline When Local Healthcare Isn’t Enough

For expats, the lines between different types of insurance can get blurry, but understanding the distinctions is absolutely critical. Your standard expat health insurance is built to cover your medical bills in your new home country—it pays for doctor visits, hospital stays, and local prescriptions. On the other hand, short-term travel insurance might include a small medical benefit for tourists, but its main job is to cover things like lost luggage or canceled flights.

Neither of those, however, is designed to handle the massive logistical and financial weight of a medical evacuation.

A medical evacuation isn’t just booking a flight. It’s a complex medical mission involving a specialized aircraft, a dedicated medical crew, and life-support equipment that can easily run between $25,000 and $250,000.

This is the exact gap that medical evacuation insurance is built to fill. It’s not about paying for the treatment—it’s about covering the astronomical cost of getting you to the right place for that treatment.

Understanding the Core Differences

Let’s use an analogy. Think of your expat health insurance as your trusted local doctor. Medical evacuation insurance, in this case, is the specialized air ambulance that flies you to a world-renowned specialist when your local doctor admits they’re out of their depth. Each one plays a unique and vital role in keeping you safe while you’re living abroad.

Here’s how they work in different real-world scenarios for an expat:

- Standard Expat Health Insurance: Covers the cost of your appendectomy surgery at the hospital down the street in your new city of residence.

- Travel Insurance: Reimburses you for a canceled flight and a quick doctor’s visit for a stomach bug during a two-week vacation back home.

- Medical Evacuation Insurance: Arranges and pays for an air ambulance to transport you from your remote town of residence to a major medical center after a serious accident where local care is insufficient.

To make it even clearer, here’s a quick comparison that highlights the unique purpose of each insurance type, so you can see exactly where medical evacuation coverage fits into your overall expat safety net.

Comparing Key Insurance Types for Expats

This table breaks down the core purpose of medical evacuation, travel, and standard expat health insurance to give you a quick, at-a-glance understanding.

| Insurance Type | Primary Purpose | Typical Expat Scenario |

|---|---|---|

| Medical Evacuation Insurance | Covers emergency transportation from an inadequate facility to a capable one. | A severe injury in a country with limited medical infrastructure requires an air ambulance to a hospital in a neighboring country or back home. |

| Standard Expat Health Insurance | Covers routine and emergency medical treatment within your country of residence. | You visit a local doctor for the flu, need surgery, or require ongoing care for a chronic condition in your new home country. |

| Travel Insurance | Covers short-term travel risks like trip cancellations, lost luggage, and limited emergency medical bills. | Your luggage is lost on a short vacation, or you need stitches for a minor cut while sightseeing away from your expat base. |

As you can see, while each policy provides a form of protection, only medical evacuation insurance is specifically designed to handle the high-stakes, high-cost logistics of getting you to critical care when it matters most for your life abroad.

The High Stakes of Living Abroad Without Evacuation Coverage

It’s easy to get swept up in the excitement of starting a new life abroad and let the practical stuff slide. But when a medical crisis hits far from home, that dream can unravel into a logistical and financial nightmare. Let’s move past the hypotheticals and look at the real-world consequences for expats caught without a dedicated medical evacuation plan.

Picture an expat retiree enjoying life in a quiet coastal village who suddenly has a major heart attack. The local clinic is fantastic for day-to-day care, but it’s not equipped with the cardiac specialists or surgical tools needed for complex procedures. Without evacuation coverage, they’re facing a life-threatening delay, left scrambling to find a way to a major medical center that could be hours—or even countries—away.

This kind of scenario exposes a critical gap that even the best expat health insurance won’t cover: the ability to get you to a world-class facility when your life is on the line.

The Staggering Financial Reality

The single greatest risk of skipping medical evacuation insurance is the astronomical cost of emergency transport. An air ambulance isn’t just a private jet; it’s a mobile intensive care unit staffed by a specialized medical team, and the price reflects that.

The costs are often financially devastating and typically include:

- Aircraft and Flight Crew: Sourcing and deploying a medically equipped jet on short notice.

- Specialist Medical Team: Doctors, nurses, and paramedics dedicated to your in-flight care.

- Life Support Equipment: Onboard ventilators, cardiac monitors, and critical medications.

- Landing and Airport Fees: Securing permits and access at both departure and arrival airports.

- Ground Ambulance Coordination: Arranging seamless transfers between hospitals and the tarmac.

This massive logistical effort comes with a price tag that can easily skyrocket into six figures. A transport within Europe might run $25,000, while a flight from Asia back to the United States could top $200,000. Facing a bill like that out-of-pocket can wipe out a lifetime of savings in a single, terrible event.

The most dangerous assumption an expat can make is that their standard insurance will cover an emergency flight home. In reality, most domestic plans stop working the moment you leave your home country’s borders.

Why Your Expat Health Plan Isn’t Enough

Many expats do the smart thing and secure excellent expat health insurance in their new country. That’s a vital first step, but it isn’t the whole solution. Expat policies are designed to pay for care within a defined region or globally. They simply aren’t all built to arrange or fund a complex international medical transfer to a facility of your choice.

It’s a crucial distinction that many people overlook. This coverage gap is precisely why a growing number of expats are turning to specialized protection.

The global medical evacuation insurance market is projected to expand significantly, reaching an estimated USD 13.7 billion by 2033. This growth is fueled by a rising awareness among the expat community of just how high international medical costs can be and the sheer price of an evacuation, which can range from $25,000 to over $100,000 per incident. As more people live and work globally, this kind of coverage is becoming less of a luxury and more of an absolute essential.

Beyond the Financial Impact

The consequences of being unprepared stretch far beyond your bank account. The emotional toll on an expat and their family during a crisis is immense. Trying to coordinate logistics, navigate language barriers, and authorize payments—all while dealing with a severe health issue—is an overwhelming burden no one should have to bear.

A medical evacuation insurance plan provides more than just a flight; it offers a 24/7 lifeline. It connects you with a team of multilingual experts who manage every single detail, from consulting with local doctors to arranging hospital admission at your destination. This support system allows you and your family to focus on the only thing that truly matters: getting better.

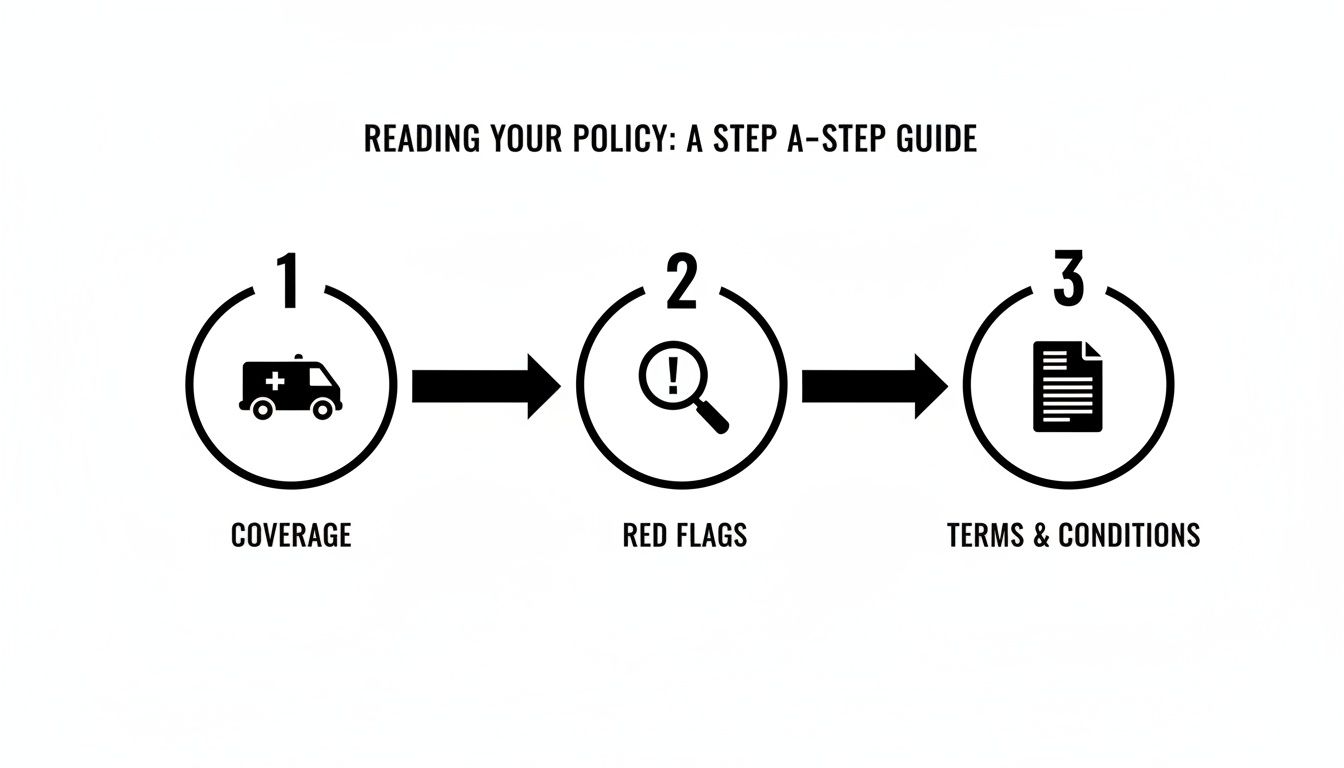

How to Read Your Medical Evacuation Policy

Let’s be honest, insurance documents are dense. They’re filled with jargon and fine print that can make anyone’s eyes glaze over. But when it comes to medical evacuation insurance, digging into the details isn’t just a smart move—it’s absolutely critical for an expat’s safety and financial security.

Think of your policy document as the user manual for your emergency lifeline. Knowing how to read it means you’ll know how to use it when a crisis hits. At its core, the policy will cover emergency medical transport, but the real story is in the nuances that determine whether your coverage is a rock-solid safety net or full of holes.

Spotting Critical Red Flags

Not all policies are created equal, and some contain clauses that can leave an expat dangerously exposed. As you review your documents, you need to develop a sharp eye for these potential red flags, which often hide in plain sight disguised in technical language.

Here are the big ones to watch out for:

- Painfully Low Coverage Limits: An air ambulance can easily cost over $100,000. If a policy has a $25,000 limit, it might look cheap upfront, but it will fall disastrously short in a real emergency. You’ll be on the hook for the massive difference.

- Vague Pre-Existing Condition Clauses: Look for crystal-clear definitions. Some policies will exclude anything related to a condition you’ve had in the past few years, while others are far more reasonable. Expats, especially retirees, need to know exactly what’s covered before you ever need to file a claim.

- Sneaky Geographical Exclusions: Many plans won’t cover you in countries with active travel warnings or those considered high-risk zones. If you live in or plan to travel through one of these areas, you must confirm it’s not on an exclusion list.

Catching these issues early is the key to avoiding devastating surprises down the road.

Decoding Key Policy Terms

Beyond the major red flags, certain phrases in your policy carry immense weight. They determine who makes the life-altering decisions during a crisis. One of the most important concepts you’ll come across is medical necessity.

Medical Necessity: This is the official justification for an evacuation. It’s not enough for you to want to be moved to a better hospital. A physician—often in consultation with the insurance provider’s own medical team—must certify that the local facility cannot provide the level of care your condition requires.

This brings up the million-dollar question: who makes the final call? Most insurers reserve the right to decide if an evacuation is approved and where you’ll be taken. It’s crucial to understand their process. Will they only move you to the “nearest appropriate facility,” or do you have the option for “repatriation to home country” or even a “hospital of choice”? These benefits completely change the value and usefulness of a policy for an expat.

A Practical Checklist Before You Sign

To make sure your medical evacuation insurance actually works for you, you need to ask the right questions. Before you commit to any plan, use this checklist to get clear, direct answers from the provider. Any transparent provider will have no problem answering these in detail.

- What is the maximum coverage limit for an evacuation? Is there a separate limit for repatriation?

- How exactly do you define a “pre-existing condition”? What is the look-back period you use?

- Who has the final say on whether an evacuation is medically necessary? What role do I or my doctor have in that decision?

- Where will I be evacuated to? Is it just the nearest facility, or can I get back to my home country or a hospital of my choice?

- Are there any specific countries or regions excluded from coverage?

- Does the plan cover a companion to travel with me during the evacuation?

- What exactly does the “repatriation of remains” benefit cover?

Getting these questions answered—preferably in writing—will empower you to compare policies like a pro and choose a plan that gives you genuine peace of mind, no matter where your journey as an expat takes you.

What Happens During a Medical Evacuation?

When a medical emergency hits you in a foreign country, things can feel chaotic and completely out of control. But with the right medical evacuation insurance, what seems like chaos is actually a highly coordinated logistical operation. It’s a finely tuned machine with one single purpose: getting you to the life-saving care you need.

It all starts with one critical phone call.

The Initial Call and Assessment

The second you or a loved one calls your provider’s 24/7 assistance line, a dedicated team snaps into action. This multilingual crew immediately gets to work, gathering the essential information. They’ll get on the line directly with the attending doctor at your local hospital to get a crystal-clear picture of your medical condition and what that facility can—and can’t—do for you.

This first assessment is everything. The insurer’s own medical directors will evaluate whether the local hospital is equipped to provide the treatment you require. If they decide the local care is inadequate, that triggers a key clause known as medical necessity, and the evacuation plan is officially set in motion.

Coordinating the Transport Logistics

Once an evacuation gets the green light, the logistics team takes the reins completely. Their entire job is to sweat the details so you and your family don’t have to. You’re free to focus on your health, and this is where a specialized plan really shows its value to an expat.

The team’s responsibilities are vast and handled with military precision:

- Determining the Right Transport: Based on your specific condition and where you are in the world, they’ll decide on the best way to move you. This could be a ground ambulance for a shorter hop, a commercial flight with a dedicated medical escort, or a private, fully-equipped air ambulance for the most critical cases.

- Arranging Medical Staff: A specialized medical crew is hand-picked for your journey. This team can include doctors, nurses, and paramedics who will provide constant, uninterrupted care while you’re in transit.

- Handling All Paperwork: They manage the mountain of paperwork, from securing flight clearances and landing rights to coordinating hospital admission documents at your destination. When you’re dealing with different languages and regulations, having access to official document translation services can be absolutely essential to keep things moving smoothly.

This simple three-step guide breaks down what you really need to look for in your policy to make sure this process works for you when it counts.

Getting a handle on these key elements—your actual coverage, any red flags, and the fine print—before an emergency is the key to unlocking your plan’s full power.

From Bedside to Bedside

It’s easy to think an evacuation is just a flight from point A to point B. But in reality, it’s a comprehensive “bedside-to-bedside” service. The whole process is meticulously planned so there are no gaps or weak links in the chain of care.

A coordinated evacuation means you are never left on your own. A medical team picks you up from your hospital bed, gets you to the aircraft in a ground ambulance, monitors you with ICU-level equipment throughout the flight, and hands you off directly to the receiving doctors at the destination hospital.

This continuous oversight ensures your treatment is never compromised. You can learn more about the different transport methods and see how they’re used in various situations by exploring these travel medical air evacuation options. This integrated system handles everything from medical clearances to payments, delivering invaluable peace of mind when you need it most.

Standalone Plan vs. Integrated Health Insurance

As an expat, sorting out your health and safety coverage leads to a big question: Do you get a dedicated, standalone medical evacuation plan, or go for a comprehensive expat health insurance policy that already has evacuation benefits built in? This isn’t just about what’s covered; it’s about what makes the most sense for your life abroad. Each option has its own perks, and the right one for you hinges on your specific needs, your budget, and how you want to manage your healthcare.

Think of it this way: a standalone plan is like an emergency flare gun. It has one critical job—to get you out of a crisis—and it does that one job extremely well. An integrated expat health plan, on the other hand, is more like a multi-tool. It handles all your day-to-day medical needs and includes that emergency flare gun as one of its essential features.

Breaking Down the Core Differences

A standalone medical evacuation plan is usually the more affordable route because it’s so specialized. Its entire focus is on the logistics and staggering cost of emergency transport. It won’t pay your hospital bills, cover surgery, or reimburse you for doctor’s visits—its sole purpose is to get you to a hospital that can handle your emergency. This makes it a fantastic choice for expats who are already satisfied with their local healthcare but need to plug that critical evacuation gap.

Meanwhile, an integrated expat health insurance policy bundles it all together. It’s your go-to for routine check-ups, emergency surgery, and prescriptions, and it has medical evacuation included right in the package. The biggest advantage here is simplicity. When an emergency hits, you have one phone number, one policy, and one company managing both your medical care and your transportation. That kind of streamlined support is a massive relief during an incredibly stressful time.

The choice between standalone and integrated often boils down to a classic trade-off: cost versus convenience. Standalone plans are easier on the wallet, while integrated plans deliver a seamless, all-in-one solution for your health and safety anywhere in the world.

Standalone Evacuation Plan vs Integrated Health Insurance

Deciding between a specialized membership and an all-in-one insurance policy can feel tricky. To make it clearer, let’s lay out the key differences side-by-side. This table breaks down what you get with each approach, helping you see the trade-offs at a glance.

| Feature | Standalone Medevac Plan | Integrated Expat Health Plan |

|---|---|---|

| Primary Function | Covers only the cost and logistics of emergency medical transport and repatriation. | Covers a full range of medical treatments (inpatient, outpatient) and includes evacuation benefits. |

| Cost Structure | Generally lower annual premiums due to its specialized, narrow focus. | Higher premiums, as it provides comprehensive health coverage in addition to evacuation. |

| Claims Process | Two separate claims: one to the evac provider for transport, another to your health insurer for treatment. | A single, streamlined claims process with one company managing both medical care and transport. |

| Best For | Expats with solid local health insurance who only need to add an emergency transport safety net. | Expats seeking a single, all-encompassing policy for total health and safety management abroad. |

Ultimately, understanding the strengths and weaknesses of each option empowers you to make a choice that truly fits your life abroad, ensuring you’re not left exposed when you need protection the most.

This decision is a crucial piece of the puzzle within the global travel medical insurance market, a sector valued at a massive USD 30.59 billion in 2024 and expected to more than double by 2030. In this landscape, a single medevac flight from a remote corner of the world can easily top $150,000. That number alone shows why having solid coverage—whether standalone or integrated—is non-negotiable. To dive deeper into how these policies stack up, explore our guide comparing expat medical insurance vs. travel insurance.

Matching the Plan to Your Expat Profile

The best choice really comes down to your lifestyle. A young digital nomad hopping between countries might lean toward a flexible, budget-friendly standalone plan to back up local, pay-as-you-go healthcare. They get that critical emergency exit without paying for a full-blown international health plan they might not use often.

On the flip side, an expat family with kids moving for a multi-year assignment would almost certainly find more value in an integrated plan. The sheer convenience of having one policy cover everything—from a child’s ear infection in Dubai to a parent’s emergency flight out of a remote village—delivers priceless peace of mind. Likewise, a retiree managing a chronic condition needs the absolute certainty that their ongoing treatments and any potential emergency transport are handled by one expert provider, leaving no dangerous gaps in care during a crisis.

Choosing the Right Plan for Your Life Abroad

When it comes to medical evacuation insurance, there’s no such thing as a “one-size-fits-all” plan. The best policy is the one that fits your specific life as an expat, not a generic template. Choosing wisely means looking past the brochure and getting real about your personal circumstances—from your destination to your day-to-day life.

The needs of a corporate exec living in a city with world-class hospitals are worlds away from those of an adventurous family exploring remote jungles. So, where do you start?

Begin with a clear-eyed assessment of your environment. An expat retiring in Portugal, where the healthcare system is strong, will have a completely different set of priorities than a digital nomad setting up shop in a rural Thai village. Think about the quality and, just as importantly, the accessibility of local medical care. If top specialists are a short drive away, your risk profile is much lower than if the nearest capable hospital is a multi-hour flight away.

Matching Coverage to Your Expat Profile

Different lifestyles demand different kinds of protection. The goal is to find coverage that mirrors your personal health, your travel habits, and the on-the-ground reality of your host country.

Here’s how a few different expat profiles might think through their decision:

- The Corporate Executive in Dubai: This person probably has access to fantastic local healthcare. Their main concern might be having a “hospital of choice” option, ensuring they can be flown back home or to a leading global facility for a highly specialized procedure.

- The Retiree in Portugal: With a higher likelihood of pre-existing conditions, their focus will be on finding a plan with clear, fair terms for chronic illnesses. They need absolute certainty that a sudden health issue won’t be an exclusion.

- The Adventurous Family in Southeast Asia: This family’s top priority is a provider with a proven, rapid-response network that reaches remote areas. They’ll want a plan with high coverage limits to account for complex, long-distance evacuations from less-developed regions.

This decision is more critical than ever. The global travel medical insurance sector, which includes medical evacuation, was valued at $5.24 billion in 2024 and is expected to hit $10.21 billion by 2034. Why the boom? Because an average international hospitalization can cost $45,000, and a medevac can easily add another $50,000 on top of that—a financial catastrophe for any expat caught uninsured. You can dig into the numbers and what they mean for travelers by reading these insights on the global travel medical insurance market.

How to Vet Insurance Providers

Once you have a good idea of what you need, the final step is finding a provider you can actually trust. A policy is only as good as the company that stands behind it, especially when you’re facing a crisis thousands of miles from home.

When vetting a provider, you’re not just buying a policy; you’re hiring a 24/7 emergency response team. Their experience, network, and reputation are just as important as the coverage limits listed in the fine print.

Look for companies with a long track record and an established global assistance network. Dive into customer reviews and testimonials, paying close attention to stories from other expats about actual evacuations. A provider with glowing reviews about their claims process and coordinated care shows they can deliver when it counts. That’s what empowers you to make a confident choice for your life abroad.

Have More Questions? We’ve Got Answers.

When you’re wading through the details of international insurance, it’s only natural for questions to pop up. Let’s tackle some of the most common ones we hear from expats to clear up any lingering confusion.

Isn’t Medical Evacuation Just a Feature of Travel Insurance?

Not quite, and this is a critical distinction for expats. Travel insurance is your go-to for short trips and vacations. It’s designed as a temporary package deal, covering things like a cancelled flight, a lost suitcase, or a minor medical issue you might face while on holiday.

On the other hand, dedicated medical evacuation insurance is a long-term lifeline built for expats. Its one and only job is to manage and pay for the staggering cost of emergency medical transport. You get much higher benefit limits—often in the millions—and a level of logistics support that your average travel plan simply can’t match.

Will My Health Insurance from Back Home Cover an Evacuation?

It’s almost a certainty that it won’t. Most health plans you have in your home country, including government-run systems like Medicare in the U.S., draw a hard line at the border. Once you’re living abroad, their coverage essentially disappears.

Relying on your domestic plan is a massive gamble. These policies aren’t set up to coordinate an international air ambulance, a service that can easily run you over $100,000. That bill would be entirely on you.

This is precisely the financial black hole that a dedicated expat evacuation plan is designed to fill.

Do I Get a Say in Where They Evacuate Me To?

This is one of the most important details for an expat to check in any policy, as the answer can vary quite a bit. A standard plan will usually get you to the “nearest appropriate medical facility.” That sounds good, but “nearest” might mean a hospital in a neighboring country—not necessarily the one you’d prefer or even back home.

More robust policies will offer a “hospital of choice” or “repatriation to home country” benefit. This feature gives you much more control over where you receive care. It’s vital to look for this specific language in a policy before you buy, making sure it lines up with what you’d want in a worst-case scenario.

At Expat Global Medical, our expertise lies in helping you sort through these crucial details. We can work with you to pinpoint a plan that not only provides the right level of coverage but also includes the specific benefits that deliver real peace of mind. Get your free quote today and build your global safety net.