Thinking about retiring overseas is more than just a daydream—it’s a real, achievable goal. But it’s a goal built on a solid foundation of smart…

Thinking about retiring overseas is more than just a daydream—it’s a real, achievable goal. But it’s a goal built on a solid foundation of smart planning. The blueprint for a successful move abroad really boils down to four key pillars: choosing the right destination, securing your legal residency, getting your cross-border finances in order, and—most importantly—locking in comprehensive expat medical insurance.

Crafting Your Overseas Retirement Blueprint

The fantasy of moving somewhere sunnier and more affordable is incredibly powerful. In fact, research shows a growing number of Americans—around 34%—are seriously considering it. But turning that vision into a sustainable reality takes a structured approach that goes way beyond planning a two-week vacation. A successful move isn’t about just picking a spot on the map; it’s about carefully building a new life that protects both your health and your nest egg.

Your journey starts with a bird’s-eye view of the essentials. This means taking an honest look at your finances, digging into visa requirements, and shortlisting countries that truly align with your lifestyle and budget.

If you’re leaning towards the Caribbean, for instance, a detailed guide on Retiring in the Dominican Republic can offer some fantastic, in-depth advice. But no matter where you plan to go, one piece of the puzzle is absolutely non-negotiable.

The Cornerstone Of Your Plan: Expat Medical Insurance

Before you get lost in spreadsheets or visa paperwork, you have to sort out your healthcare. Trying to rely on local systems or patching things together with short-term travel insurance is a massive gamble. And let’s be clear: in almost all cases, your U.S. Medicare will not cover you abroad.

This is exactly why getting a robust expat medical insurance plan is the first and most critical step. It’s the safety net that ensures one medical issue doesn’t spiral into a full-blown financial catastrophe. Without it, your retirement savings are completely exposed.

A comprehensive international health plan isn’t just for emergencies. It’s about securing long-term peace of mind, covering everything from routine check-ups and chronic condition management to a potential medical evacuation.

Think of it like building a house. Your retirement blueprint has several key pillars, but your expat medical insurance plan is the foundation everything else stands on. To help you get organized, a resource like this expat checklist for leaving the U.S. can provide a clear, step-by-step roadmap for what comes next.

To make this a bit clearer, let’s break down the essential planning areas you need to focus on.

Key Pillars of an Overseas Retirement Plan

Here’s a quick summary of the main components every future expat retiree needs to address. Getting these four areas right is the key to a smooth and secure transition.

| Planning Area | Key Objective | Critical Consideration |

|---|---|---|

| Healthcare | Secure continuous, global medical coverage. | Your domestic insurance (like Medicare) likely won’t work overseas. |

| Finances | Create a sustainable budget and tax strategy. | Currency fluctuations and U.S. tax obligations must be managed. |

| Residency | Obtain the legal right to live in your new country. | Visa requirements vary widely and often require proof of health insurance. |

| Location | Find a country that matches your lifestyle and budget. | Evaluate local healthcare quality and accessibility before committing. |

Getting a handle on these pillars early on will save you countless headaches down the road and put you on the path to a successful and worry-free retirement abroad.

Finding Your Ideal Retirement Destination

Choosing where to spend your golden years is a deeply personal call that no travel brochure can make for you. The real secret is to shift from a vacation mindset to a practical one, building a framework that lines up with your actual lifestyle, needs, and—most importantly—your budget. This means getting honest about tangible factors like cost of living, healthcare quality, visa rules, and even the local climate.

For many folks, the money conversation is where it all starts. Let’s say your monthly budget is $2,500. In a city like San Diego, that might just about cover rent, if you’re lucky. But in a place like Lisbon, Portugal, that same amount can fund a genuinely comfortable life, complete with a nice apartment, dining out regularly, and even trips around Europe. This huge gap in purchasing power is exactly why so many people are looking overseas.

Beyond The Bottom Line

While your bank account is a huge piece of the puzzle, your quality of life depends on so much more. You’ve got to picture what day-to-day living will actually look and feel like.

- Healthcare Access: How far is the nearest reputable hospital? Can you easily find doctors who speak English? The standard of care can be world-class in a capital city and completely different just a few hours away in a rural town. This is why having an expat medical insurance plan with a strong global network is vital.

- Climate and Environment: Are you chasing endless sunshine, or do you love the idea of four distinct seasons? Be honest about your tolerance for things like high humidity, rainy seasons, or scorching summer heat.

- Expat Community: Do you want to dive headfirst into a new culture, or would having a network of fellow expats make the transition smoother? A solid expat community can be an incredible support system when you’re navigating a new country.

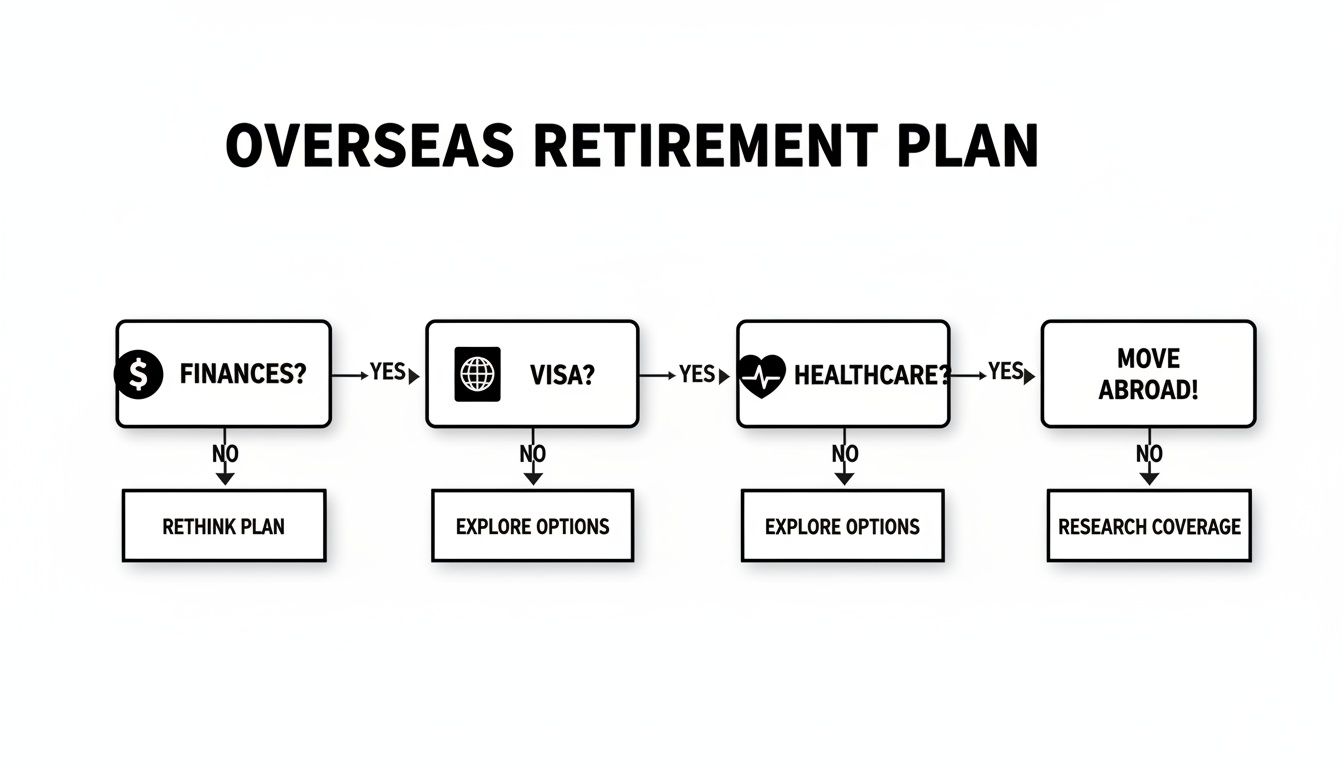

Finding the right spot is all about balancing these priorities. This flowchart is a simple way to organize your thinking around the three biggest pillars: your finances, your visa eligibility, and the healthcare system you’ll be relying on.

As the chart shows, these three things are completely interconnected. A country with a low cost of living is only a real option if you can actually get a visa and trust the local medical care—or more importantly, have a robust insurance plan that gives you access to the best private facilities.

Comparing Popular Retirement Hotspots

Let’s put a few popular countries under the microscope. Places like Panama and Costa Rica have been expat favorites for years, thanks to their warm weather and well-established foreign communities. They offer a fairly straightforward transition for many North Americans.

Lately, though, Portugal has rocketed to the top of the list for global retirees. In fact, the 2025 Global Retirement Report from Global Citizen Solutions ranked it number one, praising its unique mix of safety, quality of life, and appealing financial perks. Its updated Non-Habitual Resident (NHR) tax program, tweaked in 2024, offers a flat 20% tax on foreign pensions for a decade. Plus, its D7 “passive income” visa only requires proof of €820 per month for a single applicant—a far cry from Spain’s requirement of nearly €28,800 annually. You can read the full report from Global Citizen Solutions to get into the nitty-gritty.

Your ideal country isn’t just about the numbers—it’s about the feeling. Does this place feel like it could be home? Can you see yourself building a life here, not just visiting?

Ultimately, picking a place is a blend of careful research and gut instinct. To give you a few more ideas, you can also check out our guide to the top 7 countries to retire abroad for more detailed comparisons.

The Indispensable Scouting Trip

You can read all the articles and watch all the YouTube videos you want, but nothing replaces boots-on-the-ground experience. The single most crucial step in this whole process is taking a “scouting trip.” And I don’t mean a vacation—I mean a research mission.

When you’re there, focus on the boring, practical stuff of everyday life:

- Visit Local Hospitals: Seriously, just walk into a local clinic and then a major private hospital. Get a feel for the atmosphere, the cleanliness, and how organized (or chaotic) it seems. Ask if they work with international insurance providers.

- Shop at Local Markets: Go grocery shopping. See what things cost. Can you find the brands and products you can’t live without?

- Use Public Transportation: Try to get around town like a local. Is it easy and efficient, or is it a nightmare that will make you wish you had a car?

- Connect with Expats: Before you even go, find a local expat group on Facebook and arrange to meet a few people for coffee. Ask them for the real, unfiltered story—the good, the bad, and what they do for medical care.

This kind of hands-on experience is priceless. It’s your chance to test-drive your potential new life and discover all the little things no travel guide will ever mention, making sure the place you choose is somewhere you can truly thrive.

Navigating Visas and Securing Residency

So you’ve zeroed in on your dream retirement spot. Fantastic. Now for the next big piece of the puzzle: getting the legal right to actually live there. This is where you’ll wade into the world of visas and residency permits. For many, this part feels like a bureaucratic nightmare, but it’s entirely manageable once you know the lay of the land.

Think of it less like a maze and more like a series of gates you need to pass through. Most countries that welcome retirees have created specific visa paths just for people like us—folks who can support themselves without taking a local job. At its core, the process is about proving you won’t be a financial drain on their public systems, including healthcare.

Understanding Common Retiree Visa Types

While every country has its own lingo and rules, most retiree-friendly visas boil down to two main types. Getting your head around these will help you figure out which path is right for you.

- Pensionado Visas (Pension-Based): These are tailor-made for anyone receiving a guaranteed, lifelong pension from a government or private company. The main thing you’ll need to prove is a steady monthly pension check hitting your bank account.

- Rentista Visas (Passive Income-Based): Don’t have a traditional pension? No problem. This option is for people who live off other passive income sources, like investment returns, rental properties, or annuities.

The real difference is just where your money comes from. A Pensionado visa is a slam dunk if you have Social Security or a corporate pension. The Rentista visa, on the other hand, offers a lot more flexibility if you’re living off your nest egg.

The biggest mistake I see people make is underestimating how much time and paperwork this takes. Start gathering your documents at least six months before you even think about applying. Things like FBI background checks and proof of health insurance can drag on for much longer than you’d expect.

Just imagine swapping the high cost of living in the U.S. for a sun-drenched life in Panama. Thanks to its famous Pensionado Program, launched way back in 1987, retirees there can cut their expenses by up to 70%. This program offers permanent residency to anyone with a guaranteed pension of just $1,000 a month—or $750 for couples—and it comes with some incredible discounts on top of that.

What to Expect During the Application Process

Getting through the application itself involves a few key stages, from gathering your paperwork to finally getting that residency card in your hand. The specifics will vary, of course, but the general flow is pretty consistent from one country to another.

You’ll almost always kick things off at the consulate or embassy of your chosen country while you’re still in the States. This means putting together a hefty application package with all your documents, which usually need to be officially translated and authenticated.

Here’s a quick rundown of the documents you’ll almost certainly need to provide:

- Proof of Income: Bank statements, letters from Social Security, or brokerage statements showing your investment portfolio.

- Valid Passport: Make sure it has at least a year left before it expires.

- Criminal Background Check: This is typically an FBI check that needs to be apostilled (a form of international authentication).

- Proof of Health Insurance: An increasingly common requirement. You’ll need to show you have a comprehensive policy that covers you in your new country.

- Medical Certificate: A simple letter from your doctor stating you’re in good health.

Once your initial visa gets the green light, you’ll travel to your new country to finish everything up. This last leg of the journey usually means registering with the local immigration office, getting fingerprinted, and finally, receiving your official residency card.

Of course, once you’ve picked your spot, you’ll need to dig into the local rules. For example, if you’re eyeing the UAE, you’d want a specific guide on how to get a residence visa in Dubai to understand those nuances.

The whole process demands patience and organization. If you get ahead of the requirements and give yourself a generous timeline, you’ll navigate the path to legal residency without pulling your hair out and get started on your adventure abroad.

Why Expat Medical Insurance Is Non-Negotiable

Of all the moving pieces in your retirement plan, nothing carries more weight than sorting out your healthcare. It’s easy to get swept up in the excitement of lower living costs and sunny beaches, but a single, unexpected medical bill can wipe out your nest egg faster than anything else.

This is where so many aspiring expats get it wrong—they dangerously underestimate their healthcare needs.

A common gamble is assuming the local public healthcare system will be enough. While many countries have excellent, affordable care, new residents often face long waits to qualify. In some cases, you might never get full coverage, especially for pre-existing conditions. Frankly, relying on this is a high-stakes bet with your health and financial future.

This is exactly why a dedicated, long-term expat medical insurance plan isn’t just a nice-to-have; it’s the bedrock of a secure retirement abroad. It’s the difference between true peace of mind and that nagging anxiety about what happens if you get sick.

This Isn’t Your Typical Travel Insurance

Let’s clear up a common—and costly—misconception. There’s a world of difference between short-term travel insurance and a real international health plan. Travel insurance is for temporary trips. It’s designed to patch you up after an emergency, like a broken bone from a fall or a sudden illness. It was never built for the day-to-day health needs of someone actually living in another country.

For starters, travel policies almost never touch pre-existing conditions, routine check-ups, preventative screenings, or managing a chronic illness. For any retiree, those are the absolute essentials. A proper expat medical plan, on the other hand, works just like the comprehensive insurance you’re used to back home, but with a global reach.

Relying on travel insurance for long-term living is like using a spare tire to drive cross-country. It might work for a little while, but it’s not designed for the journey and is bound to fail when you need it most.

A solid plan from a provider like Cigna or GeoBlue is tailored for the expatriate life. It ensures you have access to quality care for everything from an annual physical to complex surgery, letting you choose your doctor and hospital from a massive global network.

What “Comprehensive” Really Looks Like

When you start digging into international health insurance for retirees, you’ll find plans that cover a huge spectrum of medical needs. A quality plan doesn’t just protect you from a catastrophe; it actively supports your health and well-being in your new home.

Here’s what a good policy should always include:

- Inpatient and Outpatient Care: This covers the big stuff like hospital stays and surgeries, but also specialist visits and diagnostic tests.

- Chronic Condition Management: For retirees managing conditions like diabetes, high blood pressure, or heart disease, this coverage is absolutely critical for ongoing care.

- Preventative Services: Think annual check-ups, cancer screenings, and vaccinations—the very things that keep you healthy long-term.

- Emergency Services: From ambulance rides to emergency room visits, this has you covered no matter where you are.

- Prescription Drug Coverage: Getting the medications you need is a crucial piece of the puzzle that many local or travel plans simply ignore.

This level of coverage gives you a seamless healthcare experience, letting you focus on enjoying your retirement instead of worrying about how to pay for a doctor’s visit. You can build a relationship with a primary care doctor in your new country, just like you would at home.

The Lifeline You Can’t Afford to Skip: Medical Evacuation

Perhaps the most overlooked—yet vital—part of any expat health plan is medical evacuation coverage. This becomes absolutely essential if you retire to a more remote or rural spot, where local clinics might not be equipped to handle a serious injury or a complex medical event.

Imagine you’ve settled into a charming coastal village. The local clinic is fine for minor things, but what if you have a heart attack or get into a serious car accident? You’ll need to be transported—fast—to a major city with a top-tier hospital. Without evacuation coverage, the cost of an air ambulance can easily top $100,000. That’s a devastating, unbudgeted hit.

A real-world scenario brings this home. Costa Rica, for example, is a top retirement destination, attracting over 25,000 U.S. retirees. But its rural infrastructure can be challenging, making reliable medical evacuation a must-have after an accident. This is where a company like Expat Global Medical shines, with over 30 years of experience serving retirees through plans from providers like GeoBlue and Best Doctors. These plans often feature 24/7 support and air ambulance services to major U.S. medical centers with up to $1 million in coverage.

This coverage is your ultimate safety net. It ensures that in a worst-case scenario, you get the best possible care without bankrupting your retirement fund to do it.

Comparing Healthcare Options for Overseas Retirees

To make the best decision, it helps to see how the different healthcare strategies stack up for a retiree living abroad long-term. It quickly becomes clear why a dedicated expat plan is the only sensible choice.

| Coverage Type | Best For | Key Limitation for Retirees |

|---|---|---|

| Travel Insurance | Short trips (under 90 days), unexpected emergencies. | Does not cover pre-existing conditions, routine care, or chronic illness management. |

| Local Public System | Basic care for legal residents (after a waiting period). | Access can be slow, quality varies, and may not cover all treatments or specialists. |

| Expat Medical Insurance | Long-term residency, comprehensive global coverage. | Higher premium cost, but provides complete protection and peace of mind without coverage gaps. |

When it comes down to it, choosing the right healthcare plan is the single most important decision you’ll make for your financial and personal security abroad. It’s the one area where cutting corners can have life-altering consequences. Investing in a robust expat medical insurance plan isn’t just an expense; it’s an investment in a healthy, secure, and worry-free life overseas.

Managing Your Finances and Taxes Across Borders

Successfully funding your retirement abroad is about much more than just hitting a savings number. It’s about building a smart financial system that works across different currencies, banking rules, and tax laws. Think of your financial strategy as the engine that powers your new life—without a good one, even the best-laid plans can sputter out.

One of the first practical hurdles you’ll face is simply getting access to your money without getting eaten alive by fees. Relying on your US bank account for everything is a rookie mistake that leads to sky-high ATM withdrawal fees and terrible exchange rates. Those little charges bleed your retirement fund dry over time.

The solution? A flexible, cross-border banking setup.

Building Your International Banking Foundation

First things first: open a local bank account in your new country as soon as your residency status allows. This will make paying for everyday things like rent, groceries, and utilities infinitely simpler and cheaper.

From there, you’ll need a way to move money from the US to your new local account efficiently. This is where modern transfer services like Wise (formerly TransferWise) or Revolut are a game-changer. They offer far better exchange rates and lower fees than a traditional wire transfer.

Over the years, most expats I’ve known have settled on a three-account system that just works:

- Your primary U.S. bank account: Keep this open. It’s essential for Social Security direct deposits and any other US-based income or bills.

- A local bank account in your new country: This becomes your hub for all day-to-day living expenses.

- An online multi-currency account: This acts as a bridge, allowing you to hold different currencies and make low-cost international transfers whenever you need to.

This structure gives you the agility to manage your money, pay bills in two countries, and shield your savings from wild currency fluctuations. Getting this right is a fundamental step in learning how to retire overseas without the constant financial headache.

Understanding Your U.S. Tax Obligations Abroad

Here’s a reality check that blindsides countless new expats: moving out of the US does not mean you get to stop dealing with the IRS. As a U.S. citizen, you are legally required to file a federal tax return every single year, reporting your worldwide income, no matter where you live.

Now, this doesn’t automatically mean you’ll be double-taxed. The US has provisions in place to prevent you from paying tax on the same income to both your new country and Uncle Sam. The two most critical tools you need to know are the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC).

The biggest financial mistake an American expat can make is assuming they no longer need to file a U.S. tax return. This can lead to significant penalties and complications down the road. Staying compliant from day one is non-negotiable.

The Foreign Earned Income Exclusion allows you to exclude a significant portion of your foreign-earned income from US taxes (it was over $120,000 for the 2023 tax year). But here’s the catch: it only applies to earned income—money you make from working, like from a consulting gig or a small business. It does not apply to passive income like pensions, Social Security, or investment returns.

For most retirees, the Foreign Tax Credit is the far more powerful tool. It gives you a dollar-for-dollar credit for income taxes you’ve already paid to your host country. For instance, if you paid $3,000 in income tax to Portugal, you can generally use that to slash your US tax bill by the same $3,000.

Given how complicated this can get, one of the smartest investments you can make is hiring a tax professional who specializes in expat issues. They can guide you through the maze of forms, help you claim the right credits, and ensure you’re fully compliant. It’s a small price to pay for total peace of mind.

A Few Lingering Questions About Retiring Overseas

Even with the best-laid plans, a few nagging questions always seem to surface right when you’re getting serious about moving abroad. Getting straight answers to these common worries is often the last step you need to feel confident enough to make the leap.

Let’s tackle the big ones we hear all the time from aspiring expat retirees.

Can I Still Get My U.S. Social Security Checks if I Live Abroad?

Yes, absolutely. In nearly every country you’d consider for retirement, this is a non-issue. The Social Security Administration (SSA) regularly sends payments to American retirees living all over the world.

The only exceptions are a handful of restricted countries, like Cuba and North Korea, where payments can’t be sent directly.

To be 100% certain, the SSA has a handy “Payments Abroad Screening Tool” on its website. Just pop in your destination country, and it’ll give you the official policy. Most expats find it easiest to just keep a U.S. bank account open and have their benefits direct-deposited there. It’s a simple, foolproof way to ensure uninterrupted payments. Just remember to keep the SSA updated with any address changes.

Does My U.S. Medicare Cover Me Overseas?

This is a big one, and the answer catches many people by surprise: No, it generally does not.

Medicare is designed to provide coverage almost exclusively within the United States and its territories. Outside of a few extremely rare and specific exceptions, it will not pay for your hospital stays, doctor visits, or prescriptions once you’re living in another country.

This is arguably the most critical gap in an American retiree’s planning. It’s the single most important reason a dedicated, long-term expat medical insurance plan isn’t just a good idea—it’s essential. Without it, you are one accident or illness away from a financial catastrophe, completely exposed to the full cost of your care.

A costly and all-too-common mistake is assuming U.S. healthcare benefits will simply follow you abroad. The hard truth is that Medicare’s geographical limits mean you absolutely must secure a private international plan to protect your health and your nest egg.

What Happens with U.S. Taxes When I’m an Expat Retiree?

Your relationship with the IRS doesn’t end when you get a new passport stamp. As a U.S. citizen, you’re on the hook for filing a U.S. federal tax return every year, and your worldwide income remains subject to U.S. income tax, no matter where you live.

But don’t panic. The system is set up to prevent you from being taxed twice on the same income. You have a couple of powerful tools at your disposal to dramatically lower what you owe:

- Foreign Tax Credit (FTC): This is the go-to for most retirees. It gives you a dollar-for-dollar credit for any income taxes you’ve already paid to your new home country, which directly reduces your U.S. tax bill.

- Foreign Earned Income Exclusion (FEIE): Keep in mind this only applies to earned income—money from a job or self-employment. It doesn’t apply to passive retirement income like Social Security, pensions, or investment withdrawals.

The rules can get tangled quickly. This is one area where professional advice pays for itself. We strongly recommend consulting with a tax professional who specializes in expat issues. They’ll make sure you stay compliant while taking full advantage of every credit and exclusion you’re entitled to.

Your health and financial security are the bedrock of a happy retirement abroad. At Expat Global Medical, we specialize in providing the robust, reliable international medical insurance that delivers true peace of mind. With access to top-tier global carriers and decades of experience, we help you find the perfect plan for your new life overseas. Get your free quote today and take the most important step toward a secure future.