So, you’re an expat wondering what this whole international health insurance thing is going to cost. The short answer? It can be anywhere from $200…

So, you’re an expat wondering what this whole international health insurance thing is going to cost. The short answer? It can be anywhere from $200 to over $1,000 a month.

The truth is, there’s no single price tag. Your final premium isn’t a fixed number but a personalized calculation based on who you are, where you’re moving, and what you need for your life abroad.

What Expat Medical Insurance Actually Costs

Let’s get right to it. The cost of expat medical insurance isn’t a simple, one-size-fits-all figure. Think of it less like buying something off the shelf and more like having a custom suit made—it’s tailored specifically to your measurements as an expatriate.

One expat might snag a basic plan for a few hundred bucks a month, while another, needing more comprehensive coverage for their family, might be looking at over a thousand. It all comes down to a handful of key factors that we’ll dig into here. The goal isn’t just to find the cheapest plan, but to secure the best value for the coverage you genuinely need to feel safe and sound abroad.

Solving the Price Puzzle for Expats

To get a real handle on what your expat insurance might cost, you have to see it as a puzzle with a few key pieces. Each piece represents a different part of your expat life and the specific plan you build.

Before we dive deep, here’s a quick overview of what drives your final premium. Think of this as your cheat sheet for understanding the moving parts of your expat insurance quote.

Quick Guide to Expat Insurance Cost Factors

This table breaks down the main drivers that influence your insurance premium. We’ll explore each one in more detail below.

| Cost Factor | Impact on Premium | Why It Matters for Expats |

|---|---|---|

| Age & Medical History | High | These are the core risk factors for insurers. Older age or past health issues often mean higher costs. |

| Destination Country | High | Healthcare prices are wildly different around the world. Moving to the U.S. will cost more than moving to Thailand. |

| Coverage Level | High | Do you need just the basics (hospital stays) or the full works (dental, vision, check-ups)? Your choice here is a huge price lever. |

| Deductible & Cost-Share | Medium | A higher deductible (what you pay first) will lower your monthly premium, but means more out-of-pocket costs when you need care. |

| Underwriting Type | Medium | Plans that review your health history upfront (full medical underwriting) often offer better, more secure coverage for pre-existing conditions. |

As you can see, you have a surprising amount of control over the final price. The choices you make as an expat directly shape the balance between your monthly premium and your out-of-pocket expenses.

This guide will walk you through each of these puzzle pieces, one by one. We’ll use real-world expat examples and practical tips to show you how to build a plan that gives you solid protection without draining your bank account.

By learning how these variables work together, you can strategically design a plan that offers robust coverage at a price you can live with. It’s all about finding that sweet spot between comprehensive protection and affordability.

By the end, you’ll have a clear roadmap to navigate these factors and find quality medical coverage that fits your expat life, giving you the peace of mind you deserve.

Read More: A Guide to Health Insurance for American Expats

The 7 Core Factors Driving Your Expat Insurance Premiums

Trying to figure out your expat medical insurance cost can feel a lot like booking a flight. The final price depends on where you’re going, the class you pick, and even when you book. It’s the same with insurance—your premium isn’t some random number. It’s a carefully calculated figure based on a handful of core factors that paint a picture of your personal risk and coverage needs.

Get a handle on these seven key drivers, and you’ll be in a much better position to find that sweet spot between rock-solid protection and a monthly cost that doesn’t break the bank. Let’s pull back the curtain and break this pricing puzzle down, piece by piece.

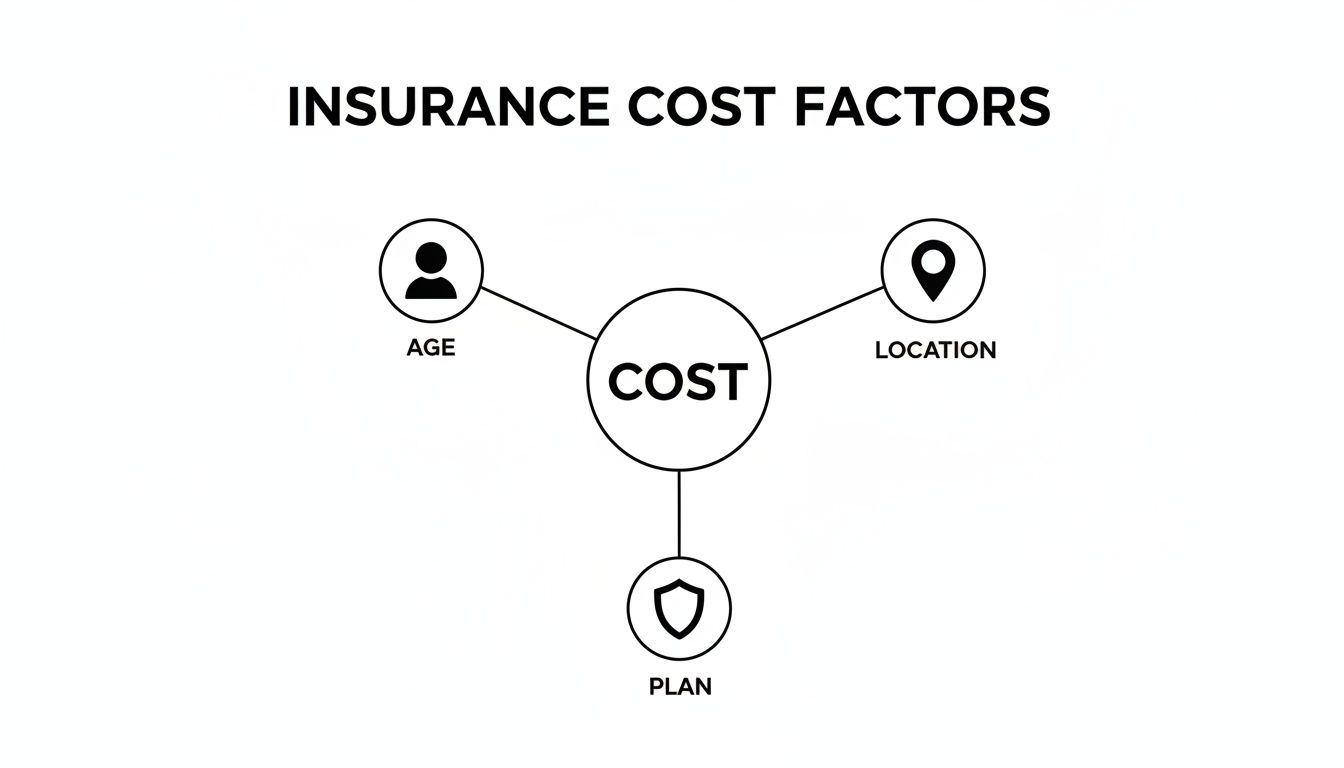

This map gives you a bird’s-eye view of the main elements that come together to determine your final cost.

As you can see, the foundational pillars of your premium are your personal profile (age), where you’ll be living as an expat (location), and the specifics of what you want covered (your plan).

1. Age: The Undeniable Baseline

Age is the most straightforward factor in the insurance world. From an insurer’s point of view, younger people are simply less likely to need major medical care. As we get older, the statistical probability of developing health conditions and needing more frequent or complex treatments goes up.

Think of it as the starting point for your premium calculation. A 28-year-old digital nomad will almost always pay a lower base premium than a 65-year-old retiree, even if every other detail is identical. It’s not personal; it’s just the statistical reality that underpins all health insurance pricing.

2. Your Expat Destination Country

Where you decide to call home as an expat has a massive impact on your international health insurance cost. Healthcare prices are wildly different around the globe. A medical procedure in the United States, for instance, can easily cost ten times more than the exact same one in Portugal or Thailand.

Insurers tackle this by grouping countries into pricing zones based on the average cost of medical care.

- High-Cost Regions: The USA, Hong Kong, Singapore, and Switzerland are notorious for their expensive healthcare systems, which pushes premiums up for any plan that includes them.

- Mid-Cost Regions: Many Western European nations like Spain, Germany, and France usually fall into this middle tier.

- Low-Cost Regions: Countries across Southeast Asia and Latin America typically have much more affordable healthcare, and that translates directly to lower insurance costs.

The single biggest way to slash your premium is often to pick a plan that excludes coverage in the USA. The sky-high cost of American healthcare means that simply adding it can sometimes double your monthly payment.

3. Your Level of Coverage

Next up is deciding just how much protection you actually want as an expat. This is a bit like choosing between a basic car insurance policy that only covers major crashes and a premium one that handles everything from tiny dents to rental cars.

Your options generally fall into a few buckets:

- Inpatient-Only Plans: These are the most basic and affordable options. They cover the big stuff—costs that come with being admitted to a hospital, like surgery, overnight stays, and major treatments.

- Comprehensive Plans: These are pricier but cover a much wider range of services. They include all the inpatient care plus outpatient services like doctor visits, specialist appointments, prescription drugs, and diagnostic tests.

- Optional Add-ons: You can customize your plan even further with riders for things like dental, vision, maternity, or annual wellness checks. Just remember, each one you add will nudge your premium higher.

4. Deductibles and Cost-Sharing

A deductible is simply the amount of money you agree to pay out-of-pocket for your medical care before your insurance company starts chipping in. Think of it as your initial share of the bill.

Choosing a higher deductible is a classic trade-off: you take on more financial risk upfront in exchange for a lower monthly premium. On the flip side, a low deductible means your insurance kicks in faster, but you’ll pay more each month for that privilege. This is one of the most powerful levers you can pull to get your monthly budget just right.

5. Geographic Area of Coverage

This is closely tied to your destination, but it’s more about the breadth of your coverage. Do you need a plan that has your back anywhere in the world, or will you be staying put in a specific region? Excluding high-cost countries like the U.S. can lead to savings of 30-50%.

The scope you choose should match your expat lifestyle and travel habits. A globetrotting digital nomad needs a very different plan than an expat who’s settling down for good in Mexico. These choices also influence which doctors and hospitals are in your network, a key difference between PPO and HMO-style plans. To learn more about that, check out our guide on understanding international health networks for expats.

6. Medical History and Underwriting

Underwriting is the process insurers use to get a clear picture of your health and medical background. If you have pre-existing conditions—like diabetes, heart disease, or chronic back pain—the insurer might charge a higher premium, specifically exclude coverage for that condition, or in some cases, decline the application.

Being upfront about your health history from the get-go is crucial. A fully underwritten plan, where you disclose everything at the start, gives you much more security and clarity down the road about what is and isn’t covered.

7. The Global Insurance Market

Finally, bigger economic forces are at play. The global health insurance market is now a massive $1.96 trillion industry. A big part of that growth comes from medical inflation, which often climbs two to three times faster than general inflation in many developed countries. This worldwide trend is exactly why having solid expat insurance is such a critical financial tool—it protects you from those soaring medical bills you might face abroad.

Real-World Cost Scenarios for Different Expats

Theory is one thing, but seeing real numbers makes it all click. To bridge the gap between cost factors and your actual budget, let’s walk through how international health insurance cost actually plays out for different types of expats around the world.

These scenarios bring the whole pricing puzzle to life. By looking at a young freelancer, a family, and a retiree, you can get a better feel for where you might land on the spectrum and see firsthand how age, location, and coverage choices lead to wildly different price tags.

For these examples, we’re making a few assumptions—like each person is in good health and has chosen a plan that excludes the USA to keep premiums more affordable. This helps us focus squarely on the core variables we’ve been talking about.

Scenario 1: The Young Freelancer in Southeast Asia

First up is Alex, a 28-year-old digital nomad setting up shop in Thailand. Alex is healthy and mainly wants solid protection for emergencies or major medical issues, without paying for bells and whistles that aren’t necessary right now. The goal is to be smart with money but avoid the massive risk of being uninsured.

Because healthcare in Southeast Asia is generally more affordable, insurance premiums reflect that. Alex decides on a plan focused on the essentials—hospital stays, surgeries—and opts for a higher deductible to keep the monthly payment down.

- Age: 28

- Location: Thailand (Worldwide excluding USA)

- Needs: Major medical and emergency coverage.

- Cost Strategy: Higher deductible, inpatient-focused plan.

For a young expat like Alex, the cost is quite manageable. An essential plan might start around $150 per month, while a more comprehensive option that includes regular doctor visits could be closer to $275 per month.

Read More: A Guide to Expat Medical Insurance for Long-Term Global Living

Scenario 2: The Expat Family Relocating to Europe

Now, let’s meet the Millers: a couple, ages 45 and 43, with two kids aged 8 and 11. They’re moving to Spain for a new job and have a completely different set of needs. They need a robust plan that covers everything from routine pediatrician visits to unexpected illnesses and specialist appointments.

With four people to cover, their premium will naturally be higher. They’re looking for a mid-range, comprehensive plan that balances a reasonable deductible with broad benefits, so the whole family has access to quality private care without long waits.

- Ages: 45, 43, 11, 8

- Location: Spain (Worldwide excluding USA)

- Needs: Comprehensive inpatient and outpatient care for four people.

- Cost Strategy: Mid-range deductible, inclusive family benefits.

An expat family plan is a significant investment. For the Millers, a basic plan might be around $650 per month, but a fully comprehensive plan with better benefits could easily range from $900 to $1,200 per month.

Scenario 3: The Retiree in Latin America

Finally, there’s Susan, a 65-year-old retiree moving to Costa Rica to enjoy the “Pura Vida” lifestyle. As an older adult, her top priority is securing top-tier medical coverage for any age-related health concerns and potential emergencies. Peace of mind is the name of the game.

Susan wants a comprehensive plan with a low deductible to keep her out-of-pocket costs predictable. Given her age, her baseline premium is the highest of our three scenarios—a direct reflection of the increased statistical risk insurers see in older age groups.

It’s a simple reality in the insurance world: premiums tend to jump significantly after age 60. This is because the likelihood of needing more frequent and complex medical care rises, making great coverage an essential financial safeguard for expat retirees.

- Age: 65

- Location: Costa Rica (Worldwide excluding USA)

- Needs: Comprehensive coverage with low out-of-pocket costs.

- Cost Strategy: Low deductible, robust benefits for chronic care management.

For an expat retiree like Susan, a solid plan is non-negotiable. An essential policy might cost around $450 per month, but the comprehensive, low-deductible plan she really wants would likely be in the $700 to $950 per month range.

Estimated Monthly Premiums for Different Expat Profiles

Putting it all together, this table summarizes the estimated monthly premium ranges for our three expat profiles. It clearly shows how age, family size, and location directly impact the final international health insurance cost. These figures are illustrative, of course, and your actual quote will depend on the specific plan you choose.

| Expat Profile | Region | Essential Plan (Higher Deductible) | Comprehensive Plan (Mid-Range) |

|---|---|---|---|

| 28-Year-Old Freelancer | Southeast Asia | $150 – $200 | $275 – $400 |

| 45-Year-Old Family of 4 | Spain, Europe | $650 – $800 | $900 – $1,200 |

| 65-Year-Old Retiree | Costa Rica | $450 – $600 | $700 – $950 |

As you can see, there’s no single answer to the question, “How much does it cost?” The price is deeply personal and is shaped entirely by your unique expat situation.

Practical Ways to Lower Your Expat Insurance Premiums

Knowing what drives your international health insurance cost is one thing, but putting that knowledge into action is where the real savings begin. You actually have a surprising amount of control over your final premium. With a few smart adjustments, you can make your coverage significantly more affordable without giving up the protection you truly need.

This isn’t about cutting corners on your health. It’s about being strategic and making informed choices that align your policy with your actual expat lifestyle and budget, striking that perfect balance between security and savings.

Choose a Higher Deductible

The most direct lever you can pull to lower your monthly premium is opting for a higher deductible. Think of the deductible as the amount you agree to pay out-of-pocket for medical care before your insurance plan kicks in to cover the rest.

By agreeing to handle a larger initial portion of your costs, you’re reducing the insurer’s immediate financial risk. In return, they offer you a lower monthly payment. This is a fantastic trade-off for generally healthy expats who want solid protection against major medical events but don’t expect to file frequent, minor claims.

Exclude USA Coverage

It’s no secret that the United States has the most expensive healthcare system in the world, by a long shot. Including it in your coverage area can cause your premiums to skyrocket—sometimes even doubling the cost.

For most expats who don’t plan on spending significant time or seeking medical care in the U.S., excluding it is a simple yet incredibly powerful way to save money.

One of the most impactful financial decisions an expat can make is opting for a “Worldwide excluding USA” plan. This single choice can lead to savings of 30-50% on your premium, making it a crucial consideration for anyone looking to manage their insurance budget effectively.

Pay Your Premium Annually

Many insurance carriers will give you a discount if you pay your premium for the entire year upfront. It does require a larger initial payment, but this simple move can save you a meaningful amount over the course of the year compared to paying monthly or quarterly.

Why? It simply reduces the administrative hassle and cost for the insurer. If your budget allows for it, paying annually is a straightforward way to lock in a lower overall price for the exact same coverage.

Trim Unnecessary Add-On Benefits

Expat health plans are often built like Legos—you start with a core plan and can add optional benefits like comprehensive dental, vision, or maternity coverage. While these add-ons are invaluable for those who need them, they also tack on extra costs to your premium.

Take a moment and be realistic about what you’ll actually use.

- Dental and Vision: Do you anticipate needing extensive dental work or new glasses this year? Or would paying out-of-pocket for routine check-ups be more cost-effective?

- Maternity: If you aren’t planning to start or expand your family abroad, maternity coverage is an expense you can likely skip.

- Wellness: Perks like gym memberships are nice to have, but you have to ask yourself if they’re worth the added monthly cost.

By carefully selecting only the add-ons you truly need, you can stop paying for services you’re unlikely to use. Navigating these choices is key, and our guide to finding affordable international health insurance offers more detailed insights to help you build a cost-effective plan that’s perfectly tailored to your life and budget.

Alright, you’ve seen how the sausage is made—all the moving parts like age, destination, and deductibles that influence the final price of your plan. Now it’s time to stop dealing in hypotheticals and find out what your specific numbers look like.

Getting a real, hard quote is the only way to shift from ballpark estimates to an actual price tag. It’s a simple process that cuts through the noise and gives you a clear, accurate figure tailored to your life abroad.

Step 1: Gather Your Key Details

Before jumping into a quote tool, it helps to have a few pieces of information ready. Don’t worry, you won’t need a stack of paperwork—just the basics to get started. This makes the whole thing go much faster.

You’ll want to have this on hand:

- Personal Info: Your date of birth, plus the birth dates of any family members you want to add to the policy, like your spouse or kids.

- Your Home Base: The primary country where you’ll be living.

- Coverage Zone: Do you need a plan that covers you everywhere, or are you okay with excluding pricey regions like the USA to save some money?

- Start Date: The day you want your health coverage to officially kick in.

That’s it. Having this ready makes the next step a breeze.

Step 2: Use an Online Quote Tool

With your details in hand, you’re ready to see what your personalized pricing looks like. A good online quote tool is designed to be painless, walking you through a straightforward form that asks for the info you just collected. It guides you from one question to the next without any confusion.

This is your chance to play around with those cost levers we talked about earlier. See for yourself—in real-time—how selecting a higher deductible or removing U.S. coverage can lower your monthly premium. The tool handles all the complex calculations for you instantly.

Getting a quote is a no-strings-attached first step. It’s simply a powerful way to see your options and understand the real-world cost of protecting your health and finances while living overseas.

The best part? You don’t just get one price. You get a lineup of plans from top-tier international insurance carriers, letting you compare them all in one place.

Step 3: Compare Your Plan Options

Once you hit “submit,” you’ll usually be presented with a side-by-side comparison of different plans. This is where you can roll up your sleeves, dig into the details, and find the one that feels right for you.

Here’s what you should be looking at for each option:

- The Premium: The monthly or annual price tag.

- The Deductible: How much you’ll pay out-of-pocket before the insurance starts paying.

- Coverage Limits: The maximum amount the plan will pay for your medical care.

- The Nitty-Gritty Benefits: Does it cover the everyday stuff like doctor visits, prescriptions, and wellness check-ups?

Laying it all out like this makes it easy to spot the trade-offs. You can quickly see which plan offers the right blend of comprehensive coverage and affordability for your budget. The whole point is to give you clarity and confidence, showing you exactly what peace of mind costs.

Ready to see your own personalized numbers? You can get a free, no-obligation quote for your expat medical insurance to compare plans and find the right coverage for your new life abroad.

Got Questions About Expat Insurance Costs? We’ve Got Answers.

When you start digging into expat medical insurance, a lot of questions pop up. It’s totally normal. This section is here to tackle the most common ones we hear from the expat community, giving you straight answers so you can move forward with confidence.

Why Is Expat Insurance So Much More Expensive Than Travel Insurance?

This one comes up all the time. Expats see the price difference between a short-term travel policy and a long-term expat plan and wonder what gives. The easiest way I’ve found to explain it is by comparing a first-aid kit to your family doctor’s office.

- Travel Insurance is your first-aid kit. It’s designed for unexpected emergencies on a trip—think a broken arm while skiing, a nasty bout of food poisoning, or a travel accident. Its job is to patch you up, stabilize the situation, and get you home if needed. It’s purely for short-term crises.

- Expat Medical Insurance is your doctor’s office. This is your primary healthcare for your new life abroad. Yes, it covers emergencies, but it’s also there for the routine stuff: annual check-ups, managing a chronic condition like diabetes, visiting a specialist, and handling all your day-to-day health needs. It’s comprehensive coverage built for the long haul.

Because expat insurance offers such a deeper and broader scope of coverage, the cost naturally reflects that. You’re not just buying an emergency hotline; you’re investing in a complete healthcare system to support your life in a new country.

Can’t I Just Keep My Health Insurance Plan From Home?

It’s tempting to think you can just hang onto your domestic health plan while living abroad, but this is a classic expat mistake that can backfire badly. Most plans from your home country, especially from the U.S., simply aren’t built for long-term overseas living.

Your home plan is tied to a specific network of doctors and hospitals, almost always within your home country’s borders. Step outside that network, and two big problems emerge:

- You’ll Face Massive Out-of-Pocket Bills: Any care you get abroad will be considered “out-of-network.” You’ll likely have to pay the entire bill upfront—which could be thousands of dollars—and then fight for reimbursement later. Good luck with that. The process is slow, frustrating, and you might only get a fraction of your money back.

- You’ll Have Huge Gaps in Coverage: Many domestic plans will only consider covering a “true life-or-death emergency” abroad. They will flat-out refuse to pay for routine check-ups, specialist visits, or ongoing treatments for a chronic condition.

For an expat, relying on a domestic plan is like having a car with no engine—it looks fine on the surface but won’t get you anywhere. The risk of rejected claims and financially crippling medical bills is just too high.

Why Did My Premium Go Up at Renewal Time?

It’s definitely frustrating to see your premium increase when it’s time to renew, especially if you haven’t even filed a claim. But these hikes aren’t random; they’re driven by a couple of predictable, industry-wide forces that impact the international health insurance cost for every expat.

The global health insurance market is a massive, dynamic system, valued at $2.14 trillion and expected to hit $4.45 trillion by 2032. This isn’t just numbers on a page; it reflects the real-world, rising cost of healthcare. North America, for instance, holds 62.15% of the market share, largely because its medical costs are so high, which pulls up the average for everyone. You can dig into the numbers yourself by checking out the full findings on the global health insurance market.

Two key things are pushing those renewal prices up:

- Global Medical Inflation: The cost of everything in healthcare—from new technologies and prescription drugs to a simple hospital stay—goes up every year. This “medical inflation” often outpaces standard inflation by a long shot. Insurers have to adjust their premiums just to keep up.

- Age-Band Adjustments: As we talked about earlier, age is one of the biggest factors in pricing your risk. As you get older, you eventually move into a new age bracket, which automatically comes with a higher base premium.

These increases are just a standard part of the health insurance world, reflecting the ever-rising cost of providing quality medical care globally. Knowing why it happens can help you budget for it and avoid any unwelcome surprises.

At Expat Global Medical, our whole mission is to cut through the confusion and help you find the right health coverage for your life abroad. We make it simple to compare top-tier plans and secure real protection that actually fits your budget.

Ready to see what your options look like? Get a free, personalized quote today and take the first real step toward protecting your health and your wallet, no matter where your adventure takes you.