Imagine this: you’re living the dream as an expat in a foreign country, but then the unthinkable happens—a serious medical emergency. This is the exact…

Imagine this: you’re living the dream as an expat in a foreign country, but then the unthinkable happens—a serious medical emergency. This is the exact moment medevac travel insurance becomes your most critical asset. It’s not your typical health insurance that covers hospital bills. Instead, it’s a lifeline that handles the incredibly complex and expensive logistics of getting you from a place with inadequate care to a hospital that can save your life.

What Is Medevac Insurance and Why Expats Need It

For anyone building a life in a new country, a solid safety net is non-negotiable. We all get health insurance, but many expats overlook a crucial piece of the puzzle: a plan for when local healthcare just isn’t enough. That’s where expat medical insurance with strong medevac coverage steps in, and it’s absolutely essential.

Think of medevac as a specialized logistics service for your well-being. A standard health plan covers the “what”—your diagnosis and treatment. Medevac insurance handles the “where,” making sure you get to the right facility for that treatment, no matter how far or how expensive the journey.

This isn’t about getting a more comfortable hospital room. An emergency medical evacuation is triggered by pure necessity. It happens when your local doctor and the insurer’s medical team both agree that the current hospital can’t provide the level of care needed to save your life or prevent permanent harm.

The Financial Lifeline for Global Citizens

The price tag on a medical evacuation can be astronomical. We’re talking about arranging an air ambulance, assembling a medical crew, navigating flight clearances, and coordinating ground transport. This can easily soar past $100,000, and often much more, depending on where you are and your condition. Without specific coverage, a single medical event could wipe you out financially.

This isn’t a niche concern, either. The global market for this protection has hit USD 5.8 billion, a number driven by the growing community of expats and digital nomads who understand the stakes. As this figure from the medical evacuation insurance market shows, medevac coverage is no longer an optional extra; it’s a fundamental part of living abroad.

For expats, the need is even sharper. You might be in a country with a fantastic healthcare system for routine issues, but it might lack the top-tier specialists for something like severe trauma or a rare cardiac event.

A medevac plan is more than just a financial backstop; it’s your key to a global emergency response network. When a crisis hits, your insurer becomes a command center, handling every single logistical nightmare so you can focus on one thing: getting better.

What Medevac Coverage Typically Includes

While the fine print always varies, any quality expat medical insurance plan will deliver a core set of medevac services built for critical moments:

- Emergency Transportation: This covers the cost of an air or ground ambulance to get you to the nearest medical facility that’s equipped to handle your specific emergency.

- Medical Escort: A trained medical team travels right alongside you, providing in-transit care with all the necessary gear and medicine to keep you stable.

- Logistical Coordination: The insurer manages everything from hospital admissions and flight clearances to speaking with the medical teams on both ends of the transfer.

- Repatriation of Remains: In the tragic event of a death, this benefit handles the significant cost and complex process of bringing remains back to your home country.

For an expat, this kind of coverage delivers profound peace of mind. It takes what could be a chaotic, terrifying experience and turns it into a managed, professional process, ensuring that distance from world-class care never puts your health at risk.

Standalone Medevac vs Integrated Expat Health Plans

When it comes to getting medical evacuation coverage, expats are at a fork in the road. This decision really shapes your entire healthcare safety net while living abroad. Do you buy a standalone medevac plan, or do you opt for a comprehensive expat medical insurance policy that already has medevac built in? Getting the difference is crucial to protecting yourself and your family.

Here’s a simple way to think about it. A standalone medevac plan is like having a dedicated ambulance service on speed dial. It’s incredibly good at one specific, critical job: getting you from a place with inadequate care to a top-notch hospital in an emergency. But once you arrive, its job is done. You’re on your own for the actual medical bills.

On the other hand, an integrated expat health plan is like having a full-service concierge for your health. It not only arranges the emergency transport (the evacuation) but also covers the hospital stays, surgeries, and follow-up care once you get there. Which one is right for you? It really boils down to what health coverage you already have in place.

The Focused Power of Standalone Medevac Plans

A standalone medevac travel insurance policy is a specialist’s tool. Its only job is to cover the mind-boggling logistics and costs of emergency medical transport. This is often the perfect choice for expats who already have solid local health insurance where they live.

Think of an American retiree living in Mexico. They might have an excellent local plan that covers all their day-to-day doctor visits and minor issues. But they want a dedicated safety net to fly them back to a hospital in Houston or Miami if a real crisis hits. That’s where a standalone plan shines.

These plans are usually more affordable than a full health plan and come with very high—or even unlimited—benefit limits just for the transportation piece.

Key features you’ll find in standalone plans:

- Dedicated Evacuation Focus: The entire policy is built around one thing: emergency transport, often managed by 24/7 crisis response teams.

- High Coverage Limits: It’s not uncommon to see limits of $1,000,000 or more, earmarked purely for evacuation and repatriation costs.

- Works Alongside Existing Insurance: It’s designed to plug the transportation gap that local health plans or even some travel medical policies have.

The main catch is a big one: it doesn’t pay a dime for the medical care you receive after you land. Those hospital bills are entirely on you or your primary health insurance.

The All-in-One Security of Integrated Expat Health Insurance

For most expats, an integrated expat medical insurance plan is the more seamless and secure route. This kind of policy rolls comprehensive global medical coverage and a robust medical evacuation benefit into one package. In a crisis, the same company coordinates both your flight and your medical care, making sure nothing falls through the cracks.

This all-in-one approach is a huge stress reliever. You make one phone call, and a single, unified response kicks into gear. There’s no need to play coordinator between two different insurance companies while you’re in the middle of a medical emergency.

An integrated expat medical insurance plan creates a seamless safety net. It ensures that your evacuation and your treatment are managed by the same team, under the same policy, preventing dangerous coverage gaps and simplifying the entire crisis-to-care journey.

This setup is ideal for expats who don’t have other health insurance or whose local plan just isn’t up to snuff for a major medical event. It offers true peace of mind, because you know that from the moment of the incident to your final recovery, one trusted source is managing your health and finances. It’s the go-to choice for anyone looking for a single, reliable answer for their well-being abroad.

Comparing Medevac Coverage Options for Expats

Deciding between a standalone plan and an integrated policy can feel complex. This table breaks down the key differences to help you see which approach aligns better with your needs as an expat.

| Feature | Standalone Medevac Plan | Integrated Expat Health Insurance |

|---|---|---|

| Primary Purpose | Emergency medical transportation and repatriation only. | Comprehensive health coverage including inpatient, outpatient, and emergency evacuation. |

| Medical Bill Coverage | No. Does not cover hospital bills, surgery, or follow-up care after transport. | Yes. Covers the full spectrum of medical treatment, subject to policy limits. |

| Best For | Expats with existing, robust local health insurance who only need to cover the transport gap. | Expats needing a single, all-in-one solution for both medical care and emergency transport. |

| Coordination in Crisis | Requires you or your family to coordinate between the medevac provider and your health insurer. | Seamless coordination. One call to one company handles both evacuation and medical care. |

| Cost | Generally lower premiums since the coverage is highly specialized and limited. | Higher premiums due to its comprehensive nature, covering all aspects of healthcare. |

| Typical Benefit Limit | High limits ($500,000 to Unlimited) specifically for transport-related expenses. | A single, high overall policy limit (e.g., $2,000,000+) that covers everything, including evac. |

| Ease of Use | Can create complexity during an emergency by involving multiple insurance providers. | Simple and straightforward. One policy, one point of contact for the entire event. |

Ultimately, the choice hinges on your existing safety net. If you have a great local health plan but it won’t fly you home, a standalone medevac plan is a smart, targeted addition. But if you’re looking for one policy to handle everything from a check-up to a catastrophic emergency, an integrated expat medical insurance plan is the clear winner for complete peace of mind.

What Triggers a Medical Evacuation

Picture this: it’s late at night in a small coastal town, and an expat suddenly feels the terrifying symptoms of a stroke. The local clinic is small, and the staff is doing their best, but they simply don’t have the neurological specialists or diagnostic tools to handle something this severe. This is the exact moment an expat medical insurance plan with medevac goes from being a document in a folder to a critical lifeline.

So, how does the whole process actually get started? It all boils down to one guiding principle: medical necessity. An evacuation isn’t something you can request because you’d prefer a hospital in another city. It’s a carefully orchestrated response to a certified medical crisis, activated only when the local facilities are deemed inadequate to save your life or prevent permanent harm.

It all begins with a single, urgent phone call.

The Chain of Command in a Crisis

Let’s stick with our expat’s story. The very first step is to call the insurer’s 24/7 emergency assistance hotline. That one call sets a complex chain of events into motion, turning a chaotic emergency into a managed, step-by-step process.

The assistance team’s first move is to get in touch with the local doctor treating the patient. They need to understand the diagnosis, the patient’s current condition, and what resources are available on-site. This isn’t just a simple check-in; it’s a professional consultation where the local physician provides their initial assessment, confirming the severity of the stroke and the clinic’s limitations.

The decision to evacuate is never made in a vacuum. It is a professional consensus between the attending physician on the ground and the insurance provider’s medical director, who both must agree that the current level of care is insufficient to produce a positive outcome.

Once the report from the local doctor comes in, it gets escalated to the insurance company’s own medical director. This person is the key decision-maker. Their job is to review the case from a clinical standpoint and officially confirm that the local standard of care is inadequate for the patient’s needs. If they agree, the evacuation is officially triggered.

The Decisive Factors for Approval

For an insurer to give the green light and launch an evacuation, several specific criteria have to be met. Knowing these triggers helps you understand exactly when and why your medevac travel insurance benefit kicks in.

The process is clear and logical:

- Initial Diagnosis: A licensed physician must diagnose a serious medical condition that demands a specific level of care—in our example, an acute stroke.

- Assessment of Local Facilities: The doctor on the scene has to certify, usually in writing, that their hospital or clinic cannot provide the necessary treatment. This could be due to a lack of specialized equipment (like an MRI machine), a shortage of expert staff (a neurosurgeon), or inadequate intensive care capabilities.

- Insurer’s Medical Director Review: The insurer’s own medical team analyzes the case notes and the local physician’s assessment. They make the final call that, based on the medical facts, an evacuation is essential to protect the patient’s life and health.

- Logistical Go-Ahead: The moment medical necessity is confirmed, the assistance team takes complete control. They become a logistical command center, arranging the air ambulance, the flight crew, all the medical clearances, and coordinating every detail with the receiving hospital.

This structured, professional process ensures that this powerful—and expensive—benefit is reserved for true emergencies. It guarantees that an expat facing a dire situation gets the life-saving transport they need, precisely when they need it most.

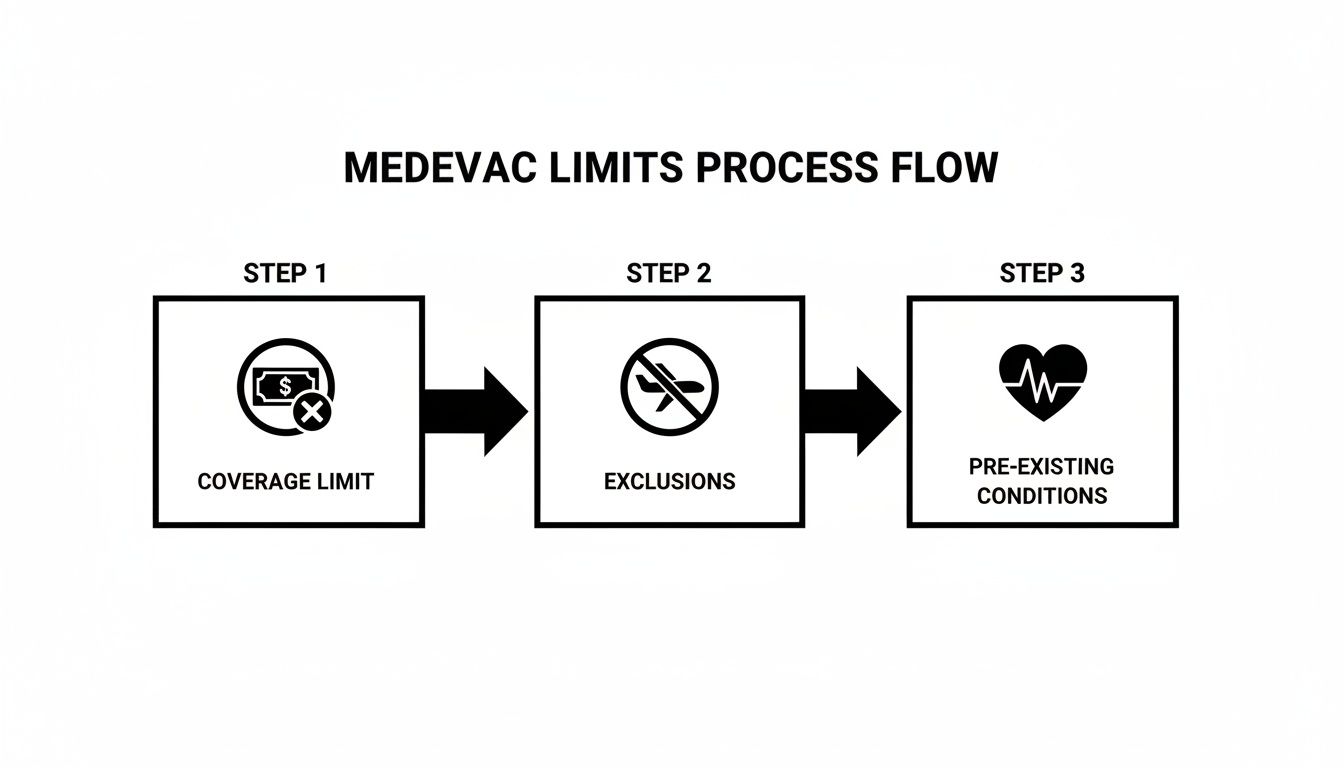

Understanding Your Policy Limits and Exclusions

The fine print in an insurance policy can feel like a maze, full of technical terms and numbers that are hard to connect to the real world. But when it comes to expat medical insurance, these details aren’t just fine print—they’re the rules that will dictate your care during a crisis.

Getting a handle on your coverage limits, what’s excluded, and how pre-existing conditions are treated is the only way to avoid a truly devastating financial surprise.

Think of your coverage limit as the total budget your insurer has set aside for your emergency. One policy might offer a $500,000 limit for evacuation, while a comprehensive expat medical insurance plan might have a total benefit of $2 million that includes medevac. In a minor situation, that half-million might seem like more than enough. But a complex evacuation involving a specialized air ambulance, a full medical team, and cross-continental flights can obliterate that amount surprisingly quickly.

The Critical Role of High Coverage Limits

A serious medical evacuation isn’t cheap. Just the air ambulance can run anywhere from $20,000 to over $250,000, depending on your location, your condition, and the distance to a hospital that can actually help you. For expats in remote corners of the globe, those costs can soar even higher.

This is exactly why a high coverage limit is non-negotiable.

Choosing a plan with a low limit to save a few dollars on premiums is a massive gamble. If your evacuation costs more than your policy’s cap, you are on the hook for the difference, period. A high-limit policy, ideally $1,000,000 or more, ensures that cost won’t be the reason you don’t get the life-saving transport you need.

When you’re facing a medical emergency, the last thing you should worry about is the cost of the flight. A robust coverage limit isn’t a luxury; it’s the core of what makes an expat medical insurance plan an effective safety net, ensuring decisions are based on medical need, not budget constraints.

This need for higher limits is backed by global trends. The medical evacuation insurance market is driven by an increasing awareness among expats and global citizens about the high costs of emergency transport. More people are opting for comprehensive plans with substantial benefits to avoid catastrophic out-of-pocket expenses.

Common Exclusions You Need to Know

Just as important as what your policy covers is what it doesn’t. These are the exclusions, and they vary wildly from one plan to another. Ignoring them can lead to a denied claim at the worst possible moment.

Here are some of the most common exclusions to watch for in an expat medical insurance policy:

- Extreme or Adventure Sports: Many standard policies won’t touch injuries from activities they consider high-risk, like scuba diving, mountaineering, or paragliding. If you’re an adventurous expat, you’ll need to find a policy with a specific adventure sports rider.

- Travel to High-Risk Countries: Policies often exclude coverage in countries with active travel warnings from government bodies like the U.S. State Department. This could include regions dealing with political instability, war, or civil unrest.

- Self-Inflicted Injuries: Incidents resulting from substance abuse, illegal activities, or intentionally hurting yourself are almost universally excluded from coverage.

Navigating Pre-Existing Conditions

For expats—especially retirees or anyone with chronic health issues—pre-existing conditions are a huge deal. A pre-existing condition is any medical issue you had before your policy started, whether it was formally diagnosed or not. Most expat medical insurance plans have very specific rules about this.

Many policies have a “look-back period,” often from 90 days to several years. They won’t cover an evacuation for a condition that wasn’t stable or had changes in treatment during that time. It’s absolutely crucial to be upfront about your health history when you apply. Hiding a condition could lead to your claim being denied for misrepresentation.

For those with ongoing health concerns, finding a plan designed to handle these complexities is vital. Our detailed guide on medical travel insurance for pre-existing conditions offers deeper insights to help you find the right coverage. Reading your policy carefully and asking direct questions about this clause is the only way to be sure you’re truly protected.

The Evacuation Journey: From Crisis to Care

When a medical crisis hits you far from home, the path from that terrifying moment to a top-tier hospital can feel like an impossible maze. But with the right expat medical insurance, what seems like a nightmare becomes a highly coordinated, manageable process. It’s a story of logistical precision, designed from the ground up to get you from crisis to care safely and efficiently.

It all kicks off with one urgent phone call to your insurance provider’s 24/7 assistance hotline. That single call is the trigger, instantly activating a dedicated team of medical and logistics experts. Your insurer transforms from a policy document in your desk drawer into an active command center for your health.

From First Call to Wheels Up

The first thing the assistance team does is get in touch with the local doctors treating you. They need a clear picture of your diagnosis, your stability, and what the local facility can and cannot do. Once the local physician confirms they can’t provide the necessary care—and the insurer’s own medical director agrees it’s a “medical necessity”—the evacuation gets the green light.

From that moment on, a logistical ballet begins. This team becomes your advocate, handling every last detail so you and your family can focus on one thing: getting better.

Their checklist is massive:

- Medical Coordination: Acting as the bridge between the hospital you’re leaving and the one you’re going to, ensuring a perfectly seamless medical handover.

- Aircraft Charter: Finding and chartering the right medically-equipped aircraft. This could be a helicopter for a short hop or a long-range jet for an international flight across continents.

- Flight Clearances: Securing all the necessary permits, landing rights, and even diplomatic clearances to cross international borders without a hitch.

- Visa and Passport Assistance: Sorting out any urgent visa arrangements for you and, if needed, a family member traveling with you.

The In-Flight Medical Team

An air ambulance isn’t just a private jet; it’s a flying intensive care unit. The coordination team assembles a flight crew and a medical team specifically for your condition. You might have a flight physician, a critical care nurse, and respiratory therapists on board, all working with advanced life-support systems.

They manage every single aspect of your care while in transit, from administering medication to constantly monitoring your vitals. The aircraft essentially becomes a mobile extension of the hospital ward, ensuring you remain stable throughout the entire journey.

The whole evacuation journey is a testament to incredible coordination. From the flight crew in the cockpit to the ambulance waiting on the tarmac at your destination, every step is pre-planned and executed with military precision by your provider’s team.

This whole process is governed by the fine print in your policy. The infographic below breaks down the key factors—coverage, exclusions, and pre-existing conditions—that will shape your evacuation journey.

Understanding these core policy elements is absolutely crucial for a smooth, fully covered evacuation.

Arrival and Seamless Handover

The final leg of the journey is just as meticulously planned. As the air ambulance prepares for landing, the team has already arranged for a ground ambulance to be waiting right there on the tarmac. Your medical records have been sent ahead, and the receiving hospital is fully prepped for your arrival. There’s no waiting around in an emergency room; you’re transferred directly to the right department for immediate care.

This peek behind the curtain reveals the true value of a solid expat medical insurance policy. It’s not just about a flight. It’s about a fully managed, end-to-end system of care built to deliver you to safety when it matters most. For a deeper look into the specifics, you can learn more about various travel medical air evacuation options and see how they fit different expat lifestyles. It’s all about letting you focus on recovery while the experts handle the rest.

How to Choose the Right Medevac Plan for Your Life Abroad

Picking the right expat medical insurance isn’t just about ticking a box. It’s about tailoring your protection to your unique life overseas. After all, the needs of a retiree enjoying the quiet life in Costa Rica are worlds apart from those of a young expat family living in Dubai.

Thinking through this process turns what feels like a confusing decision into a confident choice. It all starts with taking a hard look at your personal situation. Where are you located? How remote is it? What’s the quality of the local healthcare? What kind of activities are you doing? This quick self-audit helps you map out your risks and points you straight to the kind of coverage you actually need.

Key Questions to Ask Every Provider

When you start comparing policies, you need to go in armed with the right questions. The answers you get will pull back the curtain on the true value—and limitations—of each plan. This is how you cut through the marketing jargon to find a policy that will genuinely have your back in a crisis.

Make sure you get crystal-clear, direct answers to these crucial questions:

- Evacuation Destination: Will this policy only get me to the “nearest adequate facility,” or do I have the option to be flown back to my “home country” or a “hospital of choice”? This is probably one of the biggest differentiators between plans.

- Family and Companion Coverage: If I’m hospitalized, will the plan cover the cost for a family member to fly out and be with me? And can a companion travel with me during the evacuation itself?

- Pre-existing Conditions: What is the exact look-back period for pre-existing conditions? And how, specifically, does this policy define a “stable” condition? For anyone with a chronic health issue, this detail is non-negotiable.

- Triggering the Benefit: Who makes the final call on whether an evacuation is “medically necessary”? Is it the local doctor, your insurance company’s medical director, or some combination of both? You need to understand this chain of command before you ever need to use it.

Choosing a plan is an exercise in foresight. You are preparing for a potential crisis, and your policy’s fine print will become the operational manual for that emergency. A plan that allows for home country return, for instance, offers a level of comfort and control that a “nearest facility” clause simply cannot.

Matching the Plan to Your Expat Profile

Different lifestyles demand different kinds of coverage. A one-size-fits-all approach just doesn’t fly when you’re comparing a globetrotting digital nomad with a corporate executive on a long-term assignment.

For the Digital Nomad in Southeast Asia:

Your world is all about flexibility and moving between countries with wildly different healthcare standards. A standalone medevac plan with a high limit, bundled with a solid travel medical policy, probably gives you the perfect mix of affordable protection for a true emergency.

For the Expat Family in Dubai:

You have access to top-notch local healthcare, so your main worry is a catastrophic event that requires specialized care you can’t get locally, or simply the desire to return home for treatment. An integrated expat medical insurance plan that includes a high-limit medevac benefit with a “home country return” option is likely your best bet, keeping everything seamless for the whole family under one policy.

For the Retiree in Costa Rica:

You might have pre-existing conditions that need careful handling. Your priority is finding an expat medical insurance plan with clear, fair terms for stable conditions and a repatriation benefit that guarantees you can get back to your familiar healthcare system and family support network if things go south. For a deep dive, our guide on emergency air evacuation insurance explains costs and coverage breaks this down in much more detail.

Finalizing Your Decision

The market for this kind of protection is growing, especially in the U.S., where the travel insurance industry recently hit $5.8 billion, with 144 specialized businesses in the game. This boom isn’t an accident; it reflects a clear demand from Americans living and working abroad who understand the value of evacuation coverage.

The trend toward comprehensive expat medical insurance plans shows that people are looking for integrated solutions that include medevac. You can explore more data on the U.S. travel insurance market to see how things are evolving. In the end, your decision has to line up with your personal risk profile, your budget, and what lets you sleep at night, ensuring your global life is built on a solid foundation of security.

Frequently Asked Questions

When you start digging into the details of medevac travel insurance, a lot of questions pop up. For expats especially, getting straight, clear answers is the key to building a safety net you can actually rely on when you’re far from home. Let’s tackle some of the most common ones.

Does Medevac Insurance Cover My Hospital Bills After Evacuation?

This is a big one, and the short answer is typically no. A standalone medevac plan is really all about the ride—it’s designed to get you from a place that can’t help you to one that can.

Once you arrive, the medical bills you rack up at the destination hospital are on your primary health insurance. This is exactly why a comprehensive expat medical insurance plan, which bundles both medevac and medical coverage, is often the smartest, most seamless option for anyone living abroad long-term.

Can I Choose Which Hospital I Am Evacuated To?

That’s a critical detail you’ll want to check in your policy wording. Most standard plans will fly you to the “nearest adequate medical facility” capable of treating your condition. It’s practical, but it might not be your first choice.

More premium expat medical insurance plans, however, often include a “hospital of choice” or “home country return” option. If having that control over where you receive care matters to you, make sure it’s spelled out clearly in the policy you buy.

The distinction between evacuation to the ‘nearest adequate facility’ and ‘hospital of choice’ is one of the most significant differentiators in medevac policies. The latter provides a level of control and comfort that many expats find invaluable during a crisis.

Are Pre-Existing Medical Conditions Covered for an Evacuation?

This is where things can get tricky, as coverage for pre-existing conditions varies wildly from one policy to another. Many standalone or travel plans have a “look-back” period and won’t cover an evacuation for an unstable condition that’s changed or needed treatment recently.

On the other hand, many expat medical insurance plans are built specifically for people living abroad and will cover stable, well-managed conditions after an initial waiting period. The golden rule here is to disclose your full health history when you apply. It’s the only way to get the right coverage and avoid the nightmare of a denied claim.

Is Medical Repatriation the Same as Medical Evacuation?

They sound similar, but they’re two different benefits. Getting the distinction right is key to understanding what your expat medical insurance policy actually provides.

- Medical Evacuation: Think of this as the urgent, life-saving transport from a hospital that can’t handle your emergency to a closer, better-equipped one. The goal is immediate, critical treatment.

- Medical Repatriation: This is the journey back to your home country for ongoing care. It usually happens after your condition has been stabilized and you’re cleared for a longer trip.

Some policies roll both into one benefit, while others treat them separately with different limits and rules. Always check the definitions in your plan so you know exactly what you’re covered for.

At Expat Global Medical, we specialize in putting together insurance strategies that protect your life abroad. Whether you’re an expat, digital nomad, or retiree, let us help you find the right expat medical insurance with the medevac coverage you need to give you peace of mind, no matter where you are in the world. Get your free quote and build your safety net today.