When you start looking for the best rated international health insurance, you quickly realize a simple five-star review barely scratches the surface. For expats, the…

When you start looking for the best rated international health insurance, you quickly realize a simple five-star review barely scratches the surface. For expats, the best plans aren’t just about a flashy rating; they’re a masterful blend of an insurer’s rock-solid financial stability, exceptional claims handling, and a genuinely global medical network. That’s what ensures you’re covered, no matter where your journey as an expatriate takes you.

Unpacking What “Best Rated” Really Means for Expats

When you’re living abroad, “best rated” means something entirely different. It’s not about popularity—it’s about reliability for your expat life. It’s a measure of an insurer’s ability to come through for you when you need it most. True quality is found in the details, from how a company coordinates an emergency medical evacuation for an expat to how quickly and fairly they process a routine claim from a foreign country.

This is a market that’s growing fast, which tells you just how many expats need dependable global coverage. The global health insurance market is on track to hit USD 5.45 trillion by 2035, a massive leap from where it stands today. This boom highlights the rising demand from expats who can’t afford to gamble with their health protection while living overseas. You can find more insights on this market growth on Precedence Research.

Core Pillars of a Top-Rated Insurer for Expats

For an expat, a high rating is built on a few key pillars that have a direct impact on your life abroad. It’s critical to look past the marketing fluff and focus on what truly defines an insurer’s performance and dependability. These are the elements that separate a merely adequate plan from the best-rated international health insurance options for the expatriate community.

- Financial Strength: This is the bedrock. It tells you if the insurer can actually pay claims, even during a large-scale crisis. Ratings from agencies like A.M. Best or Standard & Poor’s are your objective look into this stability.

- Customer Service & Claims Processing: A top-tier provider offers responsive, 24/7 multilingual support and a claims process that is straightforward and efficient. Quick reimbursements and clear communication aren’t just nice-to-haves; they’re essential for an expat.

- Global Network & Direct Billing: The best insurers have sprawling networks of hospitals and clinics that allow for direct billing. This is huge for expats, as it minimizes your out-of-pocket costs and the administrative headaches that come with them.

A top rating is a signal of trust. It means the insurance company has a proven history of financial solvency and a real commitment to its policyholders, which is absolutely critical when you’re thousands of miles from home.

To help you cut through the noise, I’ve put together a table that breaks down the most important factors that go into an insurer’s rating, all from an expat’s point of view.

This table summarizes the critical components that contribute to an insurer’s overall rating and reliability for expatriates.

Key Rating Factors for Expat Health Insurance

| Rating Factor | Why It Matters for Expats | What to Look For |

|---|---|---|

| Financial Stability (A.M. Best) | Ensures the insurer can pay large, unexpected claims without any issues, safeguarding your financial future during a medical crisis abroad. | Look for carriers with an “A” (Excellent) rating or higher, which signals a strong balance sheet and solid operational performance. |

| Claims Payout Speed | Fast and fair claims processing reduces financial stress and makes sure you get reimbursed promptly for medical expenses incurred in a foreign country. | Seek out insurers known for 48-hour or 5-day claim processing times and positive customer reviews about payment speed. |

| Network Accessibility | A wide, accessible network of high-quality hospitals and doctors in your host country means you get the care you need, where you need it, often without paying upfront. | Verify the provider’s network in your specific country of residence, paying close attention to the availability of direct-billing facilities. |

Ultimately, these factors are what transform a policy on paper into real-world peace of mind. They are the true markers of a “best-rated” insurer for anyone living the expat life.

What Really Matters in an Expat Health Plan?

When you’re hunting for the best rated international health insurance, it’s easy to get dazzled by glossy brochures and big promises. But the real worth of a policy for an expatriate isn’t in the marketing—it’s buried in the details. For any expat, understanding these core criteria is the difference between having genuine security and just a false sense of it.

You have to look past the sales pitch and dissect what a plan actually offers. This means digging into the coverage limits, knowing the exclusions inside and out, checking the medical network where you actually live, and understanding how emergency services really work. A remote worker bouncing around Southeast Asia has completely different needs than a retiree settling down in Mexico, so a one-size-fits-all plan just won’t cut it for expats.

Annual Coverage Limits: What Does “Unlimited” Really Mean?

The annual limit is the absolute maximum an insurer will pay for your medical care in a policy year. Some plans cap out at $1,000,000 or $2,000,000, while others, like Cigna’s Platinum plan, proudly offer “unlimited” coverage. But for an expat, what does “unlimited” actually get you?

Typically, it means there’s no ceiling on the total payout for eligible medical costs. Great. However, that doesn’t mean every procedure is a free-for-all. Policies are riddled with sub-limits for specific services like maternity care, dental work, or mental health treatment.

An “unlimited” annual benefit looks fantastic on paper, but for an expat, the sub-limits are where the truth lies. A plan might cover millions in theory but only offer a few thousand for a specific treatment you know you’ll need abroad.

Think about it this way: an expat retiree worried about potential heart issues should be looking for a plan with sky-high limits for hospital stays and surgery, not just a flashy overall maximum. On the flip side, a young digital nomad might care more about solid outpatient services and emergency coverage. The key is to match the plan’s structure to your own expat health profile.

Navigating Exclusions: The Fine Print That Can Cost You

Every single insurance policy has exclusions—a list of things the plan simply will not cover. Skipping over this section is one of the most common and costly mistakes an expat can make. This is where you see what your coverage is truly made of.

Here are the big ones for expats to watch out for:

- Pre-existing Conditions: This is a huge deal. Some insurers, like AXA, might not cover pre-existing conditions at all on their individual plans. Others might offer coverage after a waiting period or for an extra premium.

- Adventure Sports: Planning to ski the Alps or scuba dive off the coast of Thailand? Your standard expat policy probably won’t cover you if something goes wrong. High-risk activities almost always require a special add-on, or “rider.”

- Specific Treatments: It’s a given that elective cosmetic surgery is out. But some plans also exclude things like fertility treatments, alternative therapies, or procedures they consider experimental.

Knowing these exclusions upfront saves you from shock when a claim is denied. For example, if you manage a chronic condition like diabetes, finding a provider with favorable terms for pre-existing conditions isn’t just a preference—it should be your number one priority when comparing the best rated international health insurance plans for expats.

Medical Networks and Evacuation: Your Lifeline on the Ground

A massive medical network looks impressive, but it means nothing if the affiliated hospitals in your expat city are inconvenient or have a terrible reputation. Before you sign anything, check the insurer’s network in your specific location. You’re looking for providers that offer direct billing, which is a game-changer for expats. It means the hospital bills the insurer straight away, so you’re not stuck paying a huge bill upfront and waiting weeks for reimbursement.

Emergency medical evacuation is another feature expats can’t afford to overlook. This service gets you to the nearest top-notch medical facility when local care isn’t good enough. If you’re a retiree in a remote part of Mexico, you need to know your policy has rock-solid evacuation benefits. An air ambulance can easily cost over $100,000. And be sure to check the fine print: who gets the final say on whether you’re evacuated—you or the insurance company? That single detail can change everything in a crisis.

Comparing Top International Health Insurance Providers for Expats

Choosing between the top-tier international health insurance carriers can feel a bit like splitting hairs. On the surface, they all offer global coverage, but the best plan for you isn’t a one-size-fits-all product. It’s the one that clicks with your specific needs as an expat.

Let’s move past the glossy brochures and get into a real, nuanced comparison of industry leaders like Cigna Global, GeoBlue, and IMG. We’ll focus on what truly sets them apart for the expat community—their network strengths, how flexible their plans are, and who they’re really built for. This is how you make a choice you won’t regret.

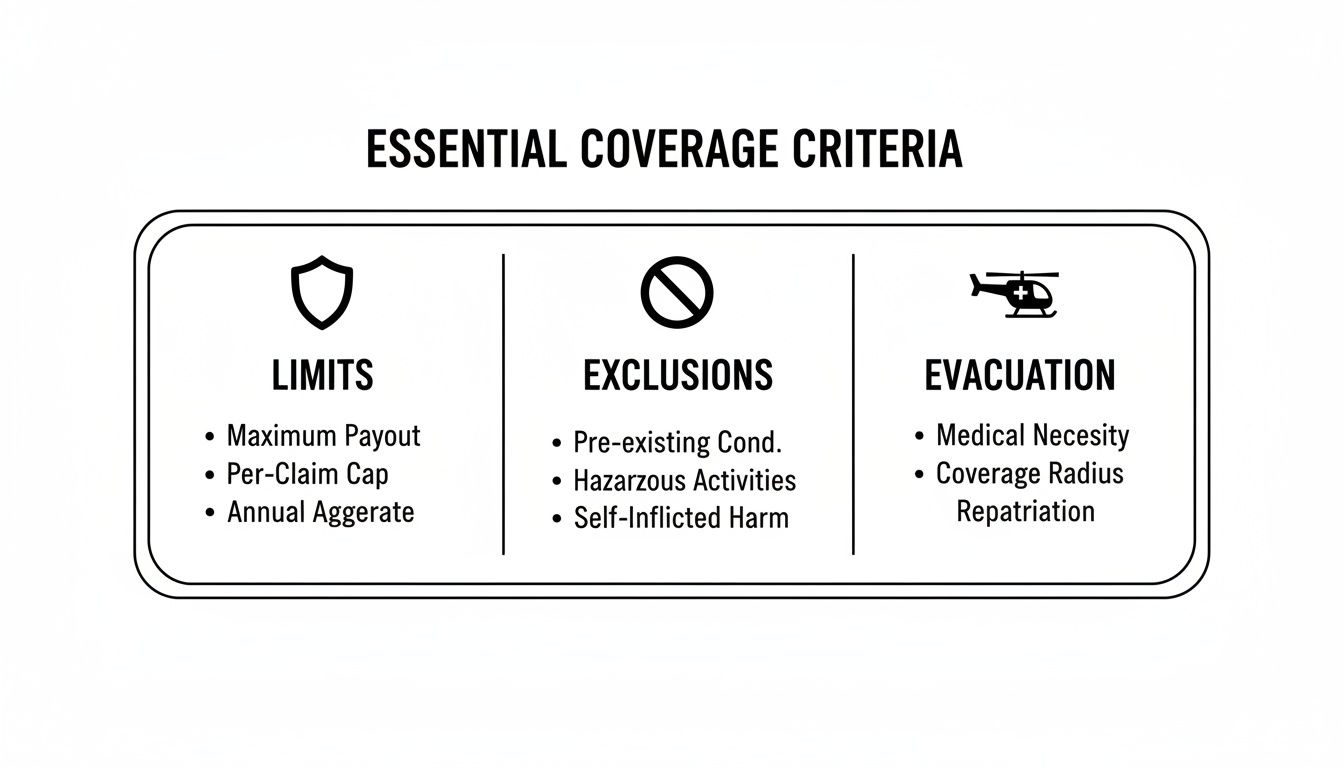

When you’re comparing policies, there are three non-negotiables you have to get right: coverage limits, exclusions, and emergency evacuation. This infographic breaks down why they’re so critical for expatriates.

As you can see, the strongest policies strike a careful balance between generous coverage limits, crystal-clear exclusions, and a rock-solid plan for getting you to safety in an emergency.

To help you see how the big players stack up, here’s a high-level look at their core strengths for the expat market.

Feature Comparison of Leading Expat Health Insurance Carriers

This table offers a snapshot of how Cigna Global, GeoBlue, and IMG compare across the metrics that matter most to people living and working abroad. Think of it as your starting point for digging deeper into the details.

| Feature | Cigna Global | GeoBlue | IMG Global Medical |

|---|---|---|---|

| Primary Audience | Global citizens & expats needing high flexibility | U.S. citizens living or working abroad | Budget-conscious expats, digital nomads, travelers |

| Key Strength | Massive direct-billing network in 200+ countries | Seamless access to the BCBS network in the U.S. | Wide range of customizable, budget-friendly plans |

| Plan Structure | Modular (core plan + optional add-ons) | Comprehensive, all-inclusive plans | Flexible tiers with customizable deductibles & riders |

| U.S. Coverage | Optional add-on, can be expensive | Included, a core feature of the plan | Optional add-on |

| Ideal For | Expats who travel frequently or live in developed areas | American expats who return to the U.S. for visits | Expats needing specific riders (e.g., adventure sports) |

While this table gives you the basics, the real value is in understanding the story behind these features. Let’s explore what makes each of these providers a top choice for different kinds of expats.

A Deep Dive Into Cigna Global

Cigna Global is a powerhouse for a reason. Their massive, well-established direct-billing network is a huge deal for expats. In over 200 countries, you can often get medical care without fronting the cash and chasing reimbursements—a common headache with lesser plans.

Their plans are famously modular. You begin with a core inpatient plan and then layer on optional benefits for outpatient care, wellness, dental, and vision. This “build-your-own” approach lets you craft a policy that fits you perfectly, whether you’re a young professional or an expat family with kids. The Cigna Platinum plan, for instance, comes with unlimited annual benefits, which is hard to beat for total peace of mind.

Cigna’s greatest asset is its global reach and administrative muscle. If you’re an expat who travels a ton or lives somewhere with a good private healthcare system, their direct-billing network is an absolute game-changer. It just simplifies everything.

Of course, this level of service and flexibility tends to come with a premium price tag. The coverage is fantastic, but it might be more firepower than a budget-conscious expat really needs.

GeoBlue: The Top Choice For U.S. Expats

GeoBlue, an independent licensee of the Blue Cross Blue Shield Association, has expertly carved out a powerful niche: serving U.S. citizens living abroad. Their killer feature is seamless access to the Blue Cross Blue Shield (BCBS) network back in the United States. This is a massive advantage for American expats who go home for visits or plan to move back one day.

Imagine a U.S. retiree in Panama. With GeoBlue, they can fly home and see their trusted BCBS network doctor with the same ease as if they had a domestic plan. GeoBlue’s top-tier plans, like the Xplorer Premier, offer unlimited annual benefits and often cover pre-existing conditions after a waiting period—a critical feature for many expats.

They also provide a carefully selected network of English-speaking doctors and elite facilities abroad, all easily accessible through a slick mobile app. This intense focus on quality and convenience makes them a leader among the best rated international health insurance providers for the American expat community.

IMG: Flexible and Accessible Plans for Expats

International Medical Group (IMG) has earned its reputation for flexibility and offering a wide spectrum of plans that cater to different budgets and needs. From basic emergency coverage to comprehensive plans like their Global Medical Insurance Platinum level, IMG truly has something for everyone—digital nomads, missionaries, and long-term expats included.

A major advantage with IMG is the ability to tweak your deductibles and coverage limits, which gives you direct control over your premium costs. They also offer optional riders for specific activities like adventure sports, a huge plus for more active expats. This makes them a fantastic choice if you want solid protection without paying for benefits you’ll never use. For a more detailed breakdown, check out our overseas health insurance comparison guide.

While North America has long been the dominant force in the health insurance market—projected to hold a 62.41% share in 2025—the ground is shifting. The Asia-Pacific region is now the fastest-growing market, with countries like India showing a staggering 18.5% CAGR. This explosive growth is pushing providers like IMG to constantly expand their networks and services in these emerging expat hotspots.

Ultimately, choosing between Cigna, GeoBlue, and IMG comes down to you. Your citizenship, destination, health, and budget will steer you toward the provider whose unique strengths are the best match for your life abroad.

Matching Your Insurance to Your Expat Lifestyle

There’s no such thing as the “best” international health insurance plan for everyone. It’s deeply personal. The perfect plan for a young digital nomad hopping around Europe would be a terrible fit for a retiree settling down in Costa Rica. The goal is to stop thinking in generic terms and start matching a policy’s real-world strengths to the specific demands of your life as an expat.

A plan’s true value isn’t just in its high-level ratings; it’s in how its features solve your problems. This means taking a hard look at your destination, your day-to-day life, and your family’s needs to make sure your coverage is a perfect fit for your expat journey, not just a generic safety net.

The Digital Nomad in Europe

For the digital nomad bouncing between European cities, the game is all about visa compliance and getting quick, flexible access to care. Most Schengen Area countries demand proof of medical insurance for any long-stay visa, usually requiring a minimum of €30,000 in coverage.

So, a top plan for this expat lifestyle has to check that official box while also being practical for someone constantly on the move.

- Schengen Visa Compliance: The policy must clearly state it meets or beats the minimum coverage needed for visas and residency permits. No ambiguity allowed.

- Strong Telehealth Services: Being able to get a virtual consultation 24/7 is a lifesaver for small issues. It means getting medical advice without derailing your travel or work plans.

- Broad European Network: You need a provider with a deep network of clinics and hospitals across multiple countries to keep out-of-pocket payments to a minimum.

The Expat Retiree in Latin America

A retiree moving to Latin America has a completely different checklist. The focus shifts from mobility to long-term health management, solid coverage for chronic conditions, and an ironclad emergency support system—especially if you’re living outside a major city.

Things like comprehensive coverage for pre-existing conditions and a high annual limit for hospital stays are non-negotiable for an expat retiree. And just as critical is a proven medical evacuation network.

For expat retirees, peace of mind comes from knowing that in a serious medical emergency, a plan has the logistical strength to transport them to a center of excellence without hesitation. This feature alone can justify a higher premium.

The best plans for this scenario will also have established relationships with top-tier private hospitals in countries like Mexico, Costa Rica, or Panama, ensuring you get the best local care possible.

The Expat Family in Asia

When an expat family relocates to a major hub like Singapore or Kuala Lumpur, their insurance needs get a lot more complex. A single policy has to work for multiple people at different stages of life, from toddlers to working adults.

Key things for expat families to look for include:

- Comprehensive Maternity Coverage: If you’re thinking of growing your family abroad, you need a plan with solid benefits for prenatal, delivery, and postnatal care. Just be mindful of the waiting periods.

- Pediatric and Wellness Care: Coverage for routine check-ups, vaccinations, and visits to pediatric specialists is absolutely essential for keeping expat kids healthy.

- Dental and Vision Add-ons: These are often optional riders but are incredibly valuable for families, helping to absorb the routine costs of cleanings, braces, and glasses.

The international health insurance market is booming to meet these varied expat lifestyles, fueled by a growing demand for personalized care that crosses borders and the rise of telehealth. Projections show the market growing from USD 1.96 trillion in 2024 with sustained annual growth, reflecting just how seriously expats are taking their global coverage. You can explore more about these market trends in this detailed analysis on Inube Solutions. For more personalized guidance, our guide on how to choose the right expat medical insurance by country offers deeper insights.

Navigating Costs and Avoiding Common Expat Pitfalls

Let’s talk about the true cost of expat medical insurance, because it’s a lot more than just the monthly premium. Several key factors directly influence what you’ll pay, and understanding them is the smartest way to manage your budget without sacrificing quality care abroad.

Your age, current health, and where you’ll be living as an expat are the biggest drivers of your premium. Insurers see age as a primary risk factor, and your destination country matters immensely. For instance, including coverage for the U.S. can jack up your costs by 30-50% simply because of its notoriously expensive healthcare system.

Key Factors That Shape Your Premiums

The real moving parts of your plan—the levers you can pull to adjust your price—are your deductible, co-insurance, and overall benefit limits. Each one is a trade-off between how much you pay upfront versus what you might owe out-of-pocket later on.

- Deductible: This is what you pay for medical care before your insurance plan starts chipping in. A higher deductible, say $5,000, will dramatically lower your monthly premium compared to a plan with a tiny $500 deductible.

- Co-insurance: Think of this as cost-sharing after your deductible is met. An 80/20 co-insurance split means the insurer covers 80%, and you pay the remaining 20% of the bill until you hit your annual out-of-pocket maximum.

- Coverage Area: As I mentioned, excluding high-cost countries like the United States is the single most effective way for an expat to lower their premium. If you don’t plan on needing frequent access to U.S. healthcare, this is an easy win for your wallet.

The real pitfall isn’t the premium you pay; it’s the unexpected bill you receive because you misunderstood your policy’s cost-sharing structure. A low premium might look appealing, but it could mask high co-insurance and a limited network that leaves you financially exposed as an expat.

Learning how these pieces fit together is crucial. You can dive deeper into this with our complete guide to international health insurance cost. It will help you strike a balance that feels right for both your budget and your peace of mind.

Common and Costly Expat Insurance Mistakes

Even with a solid plan, simple oversights can lead to huge out-of-pocket expenses. Just being aware of these common traps for expats is the first step to avoiding them and making sure your insurance actually works when you need it.

One of the most frequent mistakes we see is failing to get pre-authorization for non-emergency procedures. Many of the best-rated international health insurance providers require you to get their approval before a planned hospital stay or major treatment. Skip this step, and you could be looking at a denied claim or a massive reduction in what the insurer agrees to pay.

Another critical error is picking a plan with a weak or limited provider network in your new home country. A cheap plan is no bargain if the only in-network hospital is hours away or has a terrible reputation. Always, always verify the direct-billing network in your specific city to avoid paying huge sums upfront and then waiting weeks for reimbursement. These small details make all the difference in a real medical situation for an expat.

How a Specialist Expat Insurance Broker Secures Your Peace of Mind

Let’s be honest: trying to navigate the world of international health insurance on your own can feel like a full-time job. You’re faced with dozens of carriers, policy documents filled with jargon, and an endless list of options. It’s incredibly easy for an expat to make a costly mistake or end up with a plan that doesn’t actually cover what you need.

This is where a specialist broker like Expat Global Medical completely changes the game. We transform a confusing, stressful task into a confident, informed decision for expats.

Instead of just handing you a generic list of plans, we start by understanding your unique expat situation. Where are you going? What’s your lifestyle like? What are your specific health needs and budget? We then match you with top-rated carriers whose strengths align perfectly with what you’re looking for. This saves you countless hours of research and helps you avoid common pitfalls, like choosing a plan with a weak local hospital network.

Lasting Support, Not Just a Quick Sale

The real value of a dedicated broker kicks in long after you’ve enrolled. When you’re an expat, having a steadfast advocate on your side is critical, especially when a crisis hits. This ongoing support is what truly delivers peace of mind, ensuring you’re never left to fight a battle alone against a massive insurance company.

This kind of partnership becomes indispensable when things get complicated:

- Coordinating Difficult Claims: If a claim gets delayed or unfairly denied, your broker steps in. We act as your representative, cutting through the red tape and communicating with the insurer to get things resolved.

- Managing Medical Evacuations: In a serious emergency, we help coordinate the complex logistics of a medical evacuation. This allows you to focus on your health while we ensure the process is handled smoothly for you as an expat.

- Navigating Policy Changes: When it’s time to renew or adjust your coverage, we’re there to provide expert guidance, making sure your plan continues to meet your evolving needs as an expatriate.

Working with a specialist broker means you gain a partner for your entire life abroad. You get an expert who knows the system inside and out and is committed to protecting your interests long after the policy is signed.

Ultimately, choosing your insurance through a specialist ensures you not only get the right plan but also have the expert support to use it effectively. You gain a dedicated ally committed to safeguarding your health and finances, no matter where your global expat journey takes you.

We Hear These Questions All the Time from Expats

Stepping into the world of international medical insurance always brings up a few key questions. We’ve gathered the most common ones we hear from expats to give you clear, straightforward answers and help you feel more confident in your search for the right medical insurance.

Does Best Rated Also Mean Most Expensive?

Not at all. In fact, a truly “best rated” insurer for expats is one that delivers exceptional value—that perfect balance of rock-solid coverage, financial stability, and responsive service, all at a fair price. While the most comprehensive, top-tier plans will naturally come with higher premiums, a specialist broker knows how to find highly-rated options that fit an expat budget.

For instance, we can show you how customizing your deductible or adjusting your coverage area (like excluding the U.S., where healthcare costs are sky-high) can dramatically lower your premium without compromising the quality of your protection.

How Do Top Expat Plans Handle Pre-Existing Conditions?

This is where the top providers really show their differences, and it’s a critical point for expats to get right. Some of the best international health insurance carriers might cover stable, pre-existing conditions after a waiting period, which is often called a moratorium.

Others require full medical underwriting right at the start. They’ll look at your health history and decide whether to cover your condition, exclude it completely, or cover it for an additional premium. Getting expert guidance here is absolutely crucial to finding a carrier whose approach aligns with your specific health needs as an expat.

Finding a plan that properly handles your pre-existing conditions is one of the most important things a long-term expat can do. A mismatch here can lead to massive financial headaches and stress down the road.

Can I Keep My Expat Insurance If I Move to a Different Country?

Yes, and this is one of the core benefits of a quality international health plan. Portability is built into their design. These plans are made for global citizens and expats, allowing you to keep the exact same coverage as you move between countries, as long as they are within your chosen geographical area.

You just need to let your insurer know when you move, because your new country of residence can impact your premium. Plans offering “worldwide” coverage give you the ultimate flexibility, which is perfect for expats who expect to move around or travel a lot for work or fun. It’s how you guarantee consistent, reliable protection, no matter where you call home next.

Finding the perfect expat medical plan is a challenge, but you don’t have to figure it out alone. The experts at Expat Global Medical offer personalized advice to help you compare the best-rated options and lock in coverage that protects both your health and your finances abroad. Get your free quote today.