Securing the right Thailand health insurance is the single most important step you will take for your financial security and well-being as an expat. A…

Securing the right Thailand health insurance is the single most important step you will take for your financial security and well-being as an expat. A comprehensive medical plan is your personal safety net, guaranteeing access to top-tier medical care without the threat of a devastating bill. It is the key to truly enjoying everything the Land of Smiles has to offer with complete peace of mind.

Why Expat Health Insurance in Thailand Is Non-Negotiable

Welcome to your new life in Thailand. As you settle in, one task is more critical than any other: arranging your medical coverage. While the country is renowned for its affordability, a sudden illness or accident can lead to staggering medical bills, especially within the private healthcare system that most expats rely on.

This is where proper expat medical insurance becomes essential. It’s not merely about covering a worst-case scenario; it’s about ensuring you have a seamless, high-quality healthcare experience from the moment you need it. Without a robust plan, you are left to navigate a complex system alone, often facing language barriers and the stress of paying for everything upfront.

The Two-Tiered Healthcare System

Thailand operates two parallel healthcare systems, and understanding the distinction is crucial for any expat.

- Public Healthcare: While available, the public system often involves long wait times, crowded facilities, and significant language barriers. For most expats, it is not a practical choice for serious medical issues.

- Private Healthcare: Thailand is a global medical tourism hub for a reason. It boasts private hospitals with state-of-the-art technology, English-speaking staff, and world-class specialists. Facilities like Bumrungrad International and Bangkok Hospital offer exceptional care, but this quality comes at a premium price.

A simple consultation might be affordable out-of-pocket, but a multi-day hospital stay for an unexpected illness like dengue fever or a motorbike accident can easily exceed $10,000 USD. This is precisely why a comprehensive health plan is not a luxury—it’s a necessity for every expat. For a broader perspective on coverage for a global lifestyle, an ultimate guide to digital nomad health insurance offers relevant insights that apply to expatriates as well.

Your Financial and Medical Lifeline

Your insurance policy is more than just a payment method; it is your advocate. The best international plans offer direct billing, meaning the hospital communicates directly with your insurer. This is a game-changer, freeing you from the burden of paying massive sums out of pocket and then dealing with the hassle of reimbursement.

A proper Thailand health insurance plan acts as both a shield for your savings and a key to accessing world-class medical facilities without hesitation. It transforms a potential financial disaster into a manageable event.

Ultimately, investing in the right coverage is about managing risk. It allows you to confidently use Thailand’s excellent private medical infrastructure, knowing that your health and your finances are protected, no matter what happens. This foundation of security is what truly enables you to thrive in your new home.

Comparing Local vs. International Health Insurance for Expats

When researching health insurance for your life in Thailand, you face an immediate choice: a local Thai policy or a comprehensive international plan? This decision fundamentally shapes your healthcare experience as an expat.

The lower price of a local plan can be tempting, but it’s vital to understand the trade-offs. The choice is akin to selecting between a flimsy spare tire and a full-sized replacement—one might suffice for a short emergency, but only the other provides genuine, long-term security.

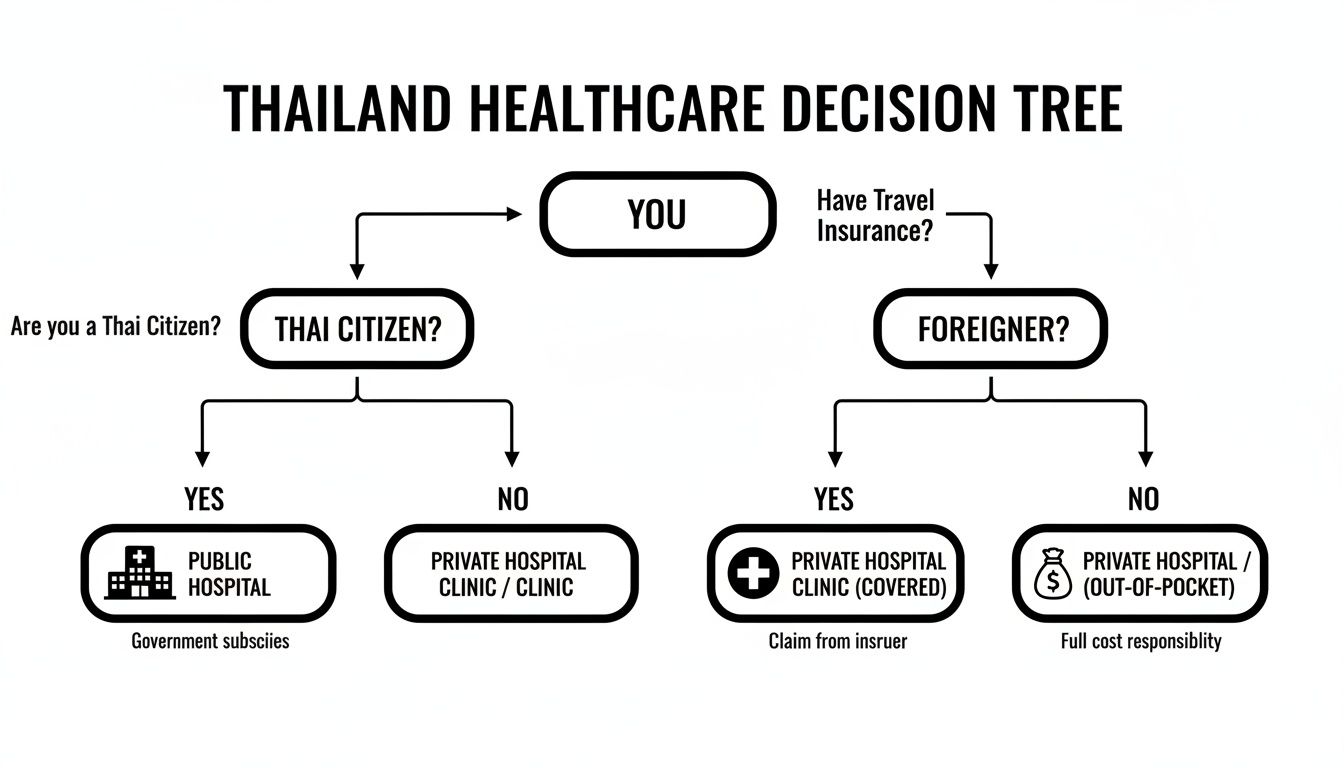

This flowchart visualizes the healthcare choices available, highlighting where public and private insurance fit for residents and foreigners.

As shown, the path for most expats leads directly to private healthcare. This makes the decision between a local or international private plan the most critical one you’ll make.

The Limitations of Local Thai Insurance Plans for Expats

Local Thai insurance policies are designed for the domestic market. While they may appear to be a bargain, they often come with severe limitations that can leave an expat dangerously exposed during a medical crisis.

These plans typically have much lower coverage limits, with caps that can be less than THB 1 million (approximately $30,000 USD). A major accident or complex surgery at a leading Bangkok private hospital could easily surpass that limit, leaving you responsible for the remainder of a massive bill.

Furthermore, local policies often have strict age cutoffs for new applicants and may refuse to renew your coverage as you get older, particularly after a significant claim. This lack of guaranteed renewability creates immense uncertainty, especially for retirees. Expats can also face administrative challenges, from policy documents written only in Thai to claims processes that require upfront payment and later reimbursement.

Why International Health Insurance Is the Standard for Expats

For the vast majority of expats, an international health insurance plan is the only option that delivers genuine security and peace of mind. These plans are specifically designed for a global lifestyle, offering a level of protection that local policies cannot match. They are the gold standard for anyone serious about safeguarding their health and savings while living abroad.

The advantages directly address the primary concerns of expatriates:

- High Coverage Limits: International plans typically offer annual limits of $1 million USD or more, ensuring you are fully covered for even the most expensive treatments, from cancer care to major cardiac surgery.

- Direct Billing Networks: Leading international insurers have established direct billing agreements with Thailand’s premier private hospitals. This means the hospital bills the insurer directly, so you aren’t forced to find huge sums of money out-of-pocket during a medical emergency.

- Worldwide Portability: Your coverage travels with you, whether you’re visiting family back home or taking a vacation to a neighboring country. This global protection is a core feature that local plans lack. You can explore how these networks function by understanding PPO vs. HMO plans abroad.

- Guaranteed Lifetime Renewal: This may be the single most important feature for long-term expats and retirees. As long as you continue paying your premiums, the insurer cannot cancel your policy due to your age or claims history. It provides security for life.

The growing preference for comprehensive private coverage is reshaping the market. The Thailand healthcare insurance sector is projected to reach USD 15,629.1 million in revenue in 2025 and is expected to nearly double by 2033. The fact that private insurance is the largest and fastest-growing segment indicates a clear demand for superior coverage.

Choosing an international plan is not a luxury; it is about securing a functional, reliable safety net. It ensures that if the worst happens, your biggest worry is getting better, not going broke.

Ultimately, the choice reflects your risk tolerance and long-term plans. For a short stay, a local plan might suffice. But for any expat building a life in Thailand, a high-quality international health insurance policy is the only responsible way to ensure complete protection.

Meeting Thailand Visa Insurance Requirements for Expats

For many expats, securing health insurance in Thailand is not just a smart financial decision—it’s a mandatory requirement for obtaining and maintaining a long-stay visa. Thai Immigration has become increasingly strict, tying long-term residency to proof of adequate medical coverage. This makes your choice of insurance policy a critical component of your application.

Navigating the regulations can feel challenging, as rules can change. However, the underlying principle is simple: the Thai government wants to ensure that foreign residents can cover their medical expenses without burdening the public system. This means your insurance policy must meet specific minimums to be accepted.

Visa-Specific Insurance Mandates

The exact insurance requirements depend on the visa category you are applying for. The rules for a retiree are different from those for a long-term professional, so it’s essential to get the details right for your specific situation.

Here is a summary of the requirements for two popular long-stay visas for expats:

- Retirement Visas (Non-Immigrant O-A and O-X): A primary choice for retirees. Applicants must have a health insurance policy showing at least THB 3 million (approximately $100,000 USD) in coverage for inpatient hospital treatments.

- Long-Term Resident (LTR) Visa: Aimed at affluent individuals, skilled professionals, and certain retirees, this visa has a higher standard. Applicants must demonstrate a health insurance policy with a minimum of $50,000 USD in coverage or provide proof of significant assets.

Failure to meet these minimum requirements will result in an immediate denial of your visa application. This is why selecting a compliant thailand health insurance plan from the outset is so important.

The Risk of Using Local Plans for Visa Applications

A basic local Thai plan might seem to satisfy the minimum coverage amount, but it can be a risky strategy, particularly for retirees. Many local policies lack guaranteed renewability. This means the insurer could refuse to renew your plan as you age or after you file a large claim, leaving you uninsured and jeopardizing your visa at your next annual extension.

An international health insurance plan not only meets Thailand’s visa requirements; it typically exceeds them. More importantly, it provides guaranteed lifetime renewability, which is the key to maintaining your residency status year after year without stress.

To ensure your policy will pass immigration scrutiny, use this checklist:

- Verify Coverage Amount: Does my policy meet or exceed the inpatient minimum for my visa (e.g., THB 3 million for the O-A)?

- Confirm Inpatient and Outpatient Benefits: The rules focus on inpatient care, but ensure your policy clearly defines what is covered.

- Check Geographic Coverage: The policy must state that it covers you in Thailand for the duration of your stay.

- Obtain Official Documentation: Your insurer must provide an official certificate of insurance formatted specifically for Thai Immigration.

Choosing a reputable international plan simplifies this entire process. These policies are designed for expats, easily meet visa regulations, and provide the long-term stability needed to settle in Thailand. For those exploring other residency options, our guide on digital nomad visa requirements also details the role of insurance.

Understanding the Real Cost of Healthcare for Expats in Thailand

While Thailand’s reputation for affordability is well-earned in many respects, this perception can be dangerously misleading when applied to healthcare. A single serious medical event can quickly deplete an expat’s savings if they are uninsured. Understanding the true financial landscape of private medical care is the first step toward effective protection.

The cost of treatment is not static; it is steadily rising due to medical inflation—a global phenomenon where healthcare prices increase much faster than general inflation. Factors like advanced medical technology, new pharmaceuticals, and growing demand for high-quality care continuously drive hospital bills higher.

This trend has a direct impact on insurance premiums. Health insurance costs in Thailand are projected to increase by nearly 10% in 2026 alone. For expats, this makes comprehensive coverage more critical than ever, as even a seemingly adequate local plan can quickly fall short.

A Look at Real-World Hospital Bills

To truly understand the financial risk, it is helpful to examine concrete examples. The bills at top-tier private hospitals in Bangkok, Phuket, or Chiang Mai can be a significant shock to expats accustomed to Thailand’s lower cost of living.

Here are some sample costs for common medical procedures. These are estimates but provide a realistic picture of what an uninsured expat might face.

- Intensive Care Unit (ICU) Stay: A single day in the ICU can easily cost THB 50,000 (about $1,350 USD) or more, excluding doctor’s fees and specific treatments.

- Appendectomy (Appendicitis Surgery): This common but urgent procedure can cost between THB 150,000 and THB 300,000 (roughly $4,000 – $8,000 USD).

- Knee Replacement Surgery: A major orthopedic surgery like this often exceeds THB 500,000 (around $13,500 USD).

- Cardiac Bypass Surgery: This life-saving heart procedure is among the most expensive, with costs frequently surpassing THB 800,000 (over $21,500 USD).

These figures clearly demonstrate why a local insurance plan with a low annual cap of, say, THB 500,000 is often completely inadequate for an expat. One major incident could exhaust your entire year’s coverage, leaving you to pay the rest out-of-pocket.

Key Factors That Determine Your Premium

Understanding the components of your insurance premium helps you budget effectively and make informed choices. While each insurer has a unique formula, several key factors consistently play a major role.

Your insurance premium is not just another monthly expense; it is a calculated investment in your financial security. Choosing a higher deductible or a more limited coverage area can lower the cost, but it also means you are assuming more personal financial risk.

The primary drivers of your premium include:

- Age: This is the most significant factor. Premiums increase with age, reflecting the higher likelihood of needing medical care.

- Coverage Level: A plan with a high annual limit (e.g., $2 million USD) will naturally cost more than one with a $250,000 limit. Comprehensive benefits that include outpatient care, dental, and vision also add to the price.

- Deductible and Co-payment: Opting for a higher deductible (the amount you pay yourself before the insurer contributes) will lower your monthly premium. This is a classic trade-off: a lower fixed cost now for potentially higher out-of-pocket expenses later.

- Area of Coverage: A plan that covers you worldwide, including high-cost countries like the USA, will be more expensive than one limited to Southeast Asia.

By weighing these factors, you can find a balance that fits your budget while providing the protection you truly need. For a more detailed analysis, see our guide on international health insurance costs. Ultimately, viewing your premium as an investment ensures you make a choice that safeguards your future in Thailand.

Must-Have Features for Your Expat Health Plan in Thailand

Navigating the options for Thailand health insurance can be overwhelming. Many plans make bold promises, but not all coverage is created equal. For an expat, certain features are absolutely non-negotiable. They represent the difference between a policy that simply looks good on paper and one that will actually protect you from financial disaster during a medical crisis.

Consider this your essential checklist. It goes beyond basic hospitalization to identify the critical elements that provide genuine security for an expatriate. These are the features that ensure your plan will not fail you when it matters most, giving you the confidence to use Thailand’s excellent private hospitals without hesitation.

High Annual Coverage Limits

The first detail to check on any policy is the maximum annual limit—the total amount the insurer will pay for your care in a single year. A local Thai plan might offer what seems like a large number in baht, but this often converts to a surprisingly low figure, sometimes as little as $30,000 USD.

A serious accident or a complex illness like cancer can easily exhaust that limit at a top private hospital in Bangkok. This is why a robust expat plan must offer a minimum annual limit of $1 million USD, with the best plans providing $2 million or more. This high ceiling ensures you are protected against even the most catastrophic medical scenarios.

Emergency Medical Evacuation

Thailand has world-class hospitals, but they are primarily located in major cities like Bangkok and Chiang Mai. If you experience a serious medical emergency while on an island or in a remote province, emergency medical evacuation coverage becomes a literal lifeline.

This feature covers the cost of transporting you from a location with inadequate medical facilities to the nearest hospital capable of handling your condition. This could involve an ambulance ride to Bangkok or even a medical flight to Singapore. Without this coverage, you could face tens of thousands of dollars in transport costs alone, in addition to your hospital bills.

Direct Billing Network Access

Imagine being admitted to a hospital for an emergency and being asked to pay $10,000 USD upfront before treatment can begin. This stressful and often impossible scenario is avoided with a plan that includes a strong direct billing network.

Direct billing means the hospital sends the bill straight to your insurance company. You simply present your insurance card, and the financial arrangements are handled behind the scenes. It is arguably the single most important feature for a stress-free hospital experience.

When comparing plans, don’t just ask if they offer direct billing—ask which specific hospitals in Thailand are part of their network. You want a plan that has agreements with premier facilities like Bumrungrad International Hospital, Samitivej Hospital, and the Bangkok Hospital Group.

Guaranteed Lifetime Renewability

For any expat planning to live in Thailand long-term, especially retirees, this feature is absolutely critical. Guaranteed renewability means that as long as you continue to pay your premiums, the insurance company cannot cancel your policy or refuse to renew it, regardless of your age or how many claims you make.

Many local plans do not offer this guarantee, placing older expats at risk of being dropped from their coverage just when they need it most. An international plan with this protection provides the long-term stability necessary to live in Thailand with true peace of mind, knowing your coverage is secure for life.

Other vital features for expats include:

- Robust Outpatient Care: Covers services that do not require an overnight hospital stay, such as doctor’s appointments, specialist consultations, and diagnostic tests.

- Worldwide Portability: Ensures your plan covers you not only in Thailand but also when you travel to other countries or return home for visits.

- Pre-existing Condition Coverage: While often subject to a waiting period, finding a plan that will eventually cover known health issues is crucial for managing ongoing care.

How to Get Your Expat Health Insurance Coverage

You now understand what constitutes a solid health plan for an expat in Thailand. The next step is to secure one.

Acquiring the right Thailand health insurance is more than just filling out a form. It is a thoughtful process that requires a personalized approach. This roadmap will guide you through the final steps, helping you transform knowledge into a tangible, reliable safety net.

First, take a moment for a personal assessment. What does your life as an expat in Thailand look like? Are you a retiree in Phuket, a digital nomad moving between Chiang Mai and the islands, or a Bangkok-based professional with a family? Your age, lifestyle, health status, and travel habits will all point toward the most suitable type of coverage.

Once you have a clear picture of your needs, the most effective next step is to consult a specialist insurance broker. While you can approach insurance companies directly, a good broker works for you. They act as your expert guide and advocate, offering unbiased advice at no extra cost.

Finding the Right Plan with an Expert Broker

Think of a specialist expat broker as your personal shopper for insurance. Instead of spending days comparing dozens of complex policies from providers like Cigna, GeoBlue, and IMG, a broker will present you with a curated selection of options that match your needs and budget.

Their value extends far beyond simply providing quotes. A seasoned broker helps you navigate the often-tricky application and underwriting process. They translate insurance jargon, assist with medical disclosures, and ensure your application is presented in the best possible light.

An independent broker’s loyalty is to you, not to a specific insurance company. They are your advocate during the application and, crucially, if you ever have to make a claim or arrange a medical evacuation.

This support becomes invaluable during a medical emergency. When you are sick or injured, the last thing you want to do is debate coverage with an insurer. Your broker steps in, manages communication, and advocates to ensure your claim is handled smoothly and fairly.

Understanding the Market Dynamics

Expert guidance is more important than ever in a constantly evolving market. Thailand’s life and health insurance industry is projected to reach $36.1 billion by 2026, and such rapid growth brings change.

Health insurance premiums are expected to rise by nearly 10% in 2026, driven by medical inflation and emerging health risks. This is where partnering with a specialist like Expat Global Medical, who works with top international providers, truly pays off. They can help you find a plan designed to withstand these rising costs, protecting you from crippling out-of-pocket expenses for top-tier medical care. You can read more about Thailand’s evolving insurance landscape to understand the full context.

By following this structured approach—first identifying your needs, then leveraging the expertise of a broker—you can confidently secure a plan that provides true peace of mind for your life as an expat in Thailand.

Frequently Asked Questions from Expats

When arranging health insurance for a new life in Thailand, it’s natural to have questions. This is unfamiliar territory for most expats. Here, we address some of the most common queries with clear, straightforward answers to help you make an informed decision.

Can I Use Travel Insurance for Long-Term Stays as an Expat?

Absolutely not. Travel insurance is designed for short-term emergencies during a holiday, such as lost luggage or a minor, acute illness. It is completely inadequate for anyone living in Thailand as an expat.

Travel insurance will not cover routine medical care, manage chronic conditions, or provide the comprehensive coverage needed for a serious medical situation. Critically, it will not meet the minimum coverage requirements for long-stay Thai visas, such as the Retirement or LTR visas. To live in Thailand legally and be properly protected, you need a legitimate international health insurance plan.

I’m Young and Healthy. Do I Really Need Expat Health Insurance?

Yes, without question. While it’s easy to feel invincible when you’re healthy, accidents and unexpected illnesses can happen to anyone at any age. A motorbike accident or a severe case of dengue fever can occur without warning.

The cost of treatment at a quality private hospital can be financially crippling, potentially wiping out your savings. A robust health plan acts as a financial shield, protecting you from overwhelming debt and ensuring you receive the best possible medical care immediately.

Think of it this way: health insurance isn’t just for the person you are today. It’s for the person you might become after an unexpected event. It’s all about protecting your future self from a crisis.

What if I Have a Medical Emergency Outside a Major City?

This scenario is precisely why emergency medical evacuation is a non-negotiable feature for any expat health plan. If you have a serious accident or fall ill while in a rural area or on an island with limited medical facilities, this benefit is your lifeline.

It covers the high cost of transporting you—by ambulance or even helicopter if necessary—to a leading hospital in Bangkok or flying you to another country for specialized treatment. For any expat who plans to travel beyond the main urban centers, this is an essential protection.

Should I Buy Directly from an Insurer or Use an Expat Broker?

Using a specialist expat insurance broker is almost always the better choice, and importantly, it costs you nothing extra. While you can purchase a plan directly from an insurance company, a broker works for you, not for the insurer.

They provide unbiased advice, comparing plans from multiple top-tier providers to find the one that best fits your specific needs and budget. A good broker becomes your advocate, especially when you need to make a claim. They help you navigate the paperwork and ensure the process is handled efficiently and fairly. Their expertise simplifies the entire experience, from selecting the right policy to using it when it matters most.

Ready to find a health insurance plan that lets you live in Thailand with true peace of mind? The team at Expat Global Medical has been helping expats secure reliable international coverage since 1992. Get a free, no-obligation quote and personalized advice to protect your health and finances.