")

For expats, the best medical evacuation insurance isn’t some simple travel add-on; it’s a non-negotiable part of a secure global lifestyle. Think of it as a financial and logistical lifeline, typically featuring coverage limits north of $1 million, round-the-clock access to a global assistance network, and the flexibility of both air and ground transport to get you to high-quality medical care when local facilities just won’t cut it.

Defining the Best Medical Evacuation Insurance for Expats

When you live abroad long-term, your healthcare needs change dramatically compared to someone on a short vacation. The best medical evacuation insurance for an expat is built for this reality. It functions as a highly specialized safety net, acknowledging the hard truth that the nearest hospital in your host country might not meet international standards of care for a serious illness or injury.

This type of insurance is fundamentally different from the limited coverage you might find tacked onto a standard travel policy. For expats, it’s all about guaranteeing access to world-class medical treatment, no matter where you’ve set up your life. Its core purpose is to coordinate and pay for your transport to a more suitable medical facility—which could be in a neighboring country or all the way back home.

Key Components of a Strong Expat Policy

A truly robust policy is built on several key pillars that provide comprehensive protection. These are the features that separate a basic, flimsy plan from one genuinely suited for the expat life. Understanding them is the first step in making a smart decision. For a deeper dive, feel free to explore our complete guide to expat medical coverage.

The real value of a dedicated expat evacuation plan isn’t just the money—it’s the coordination. You’re not just buying a flight; you’re getting a team of medical and logistics experts who manage your care from the moment of crisis until you are safely in a capable facility.

To help you size up your options, I’ve put together a table that breaks down the essential features you should be looking for in any premier expat plan.

Core Features of Premier Medical Evacuation Plans for Expats

This table outlines the essential features and ideal benchmarks for evaluating medical evacuation insurance policies designed for long-term expatriate life.

| Essential Feature | Benchmark for Expats | Why This Matters Abroad |

|---|---|---|

| Coverage Limit | $1,000,000 or higher | Covers the staggering cost of air ambulances and specialized medical teams. |

| Global Assistance | 24/7 multilingual support | Guarantees immediate help and coordination during a crisis, day or night. |

| Transport Options | Air & ground ambulance | Provides the flexibility to use the most appropriate transport for your situation. |

| Repatriation of Remains | Included up to a set limit | Eases the logistical and financial burden on your family during a difficult time. |

| Bedside Visit | Coverage for one family member | Allows a loved one to be with you during a medical emergency in a foreign country. |

| Pre-existing Conditions | Clear policy on acute onset | Defines coverage for sudden flare-ups, a crucial detail for many expats. |

How Expat Evacuation Insurance Actually Works

If you’re an expat, you need to know that medical evacuation insurance is a completely different beast from the basic coverage tacked onto a standard travel insurance plan. For a tourist on a two-week holiday, medevac is a small add-on. For an expat living abroad, it’s a non-negotiable, life-saving core feature of your international health plan.

And the stakes are enormous. The global growing medical evacuation market is exploding because expats and global citizens are waking up to the fact that a single air ambulance flight can easily cost anywhere from $25,000 to over $100,000. Without the right plan, that’s a financially crippling bill.

The real value of a dedicated expat plan isn’t just about covering that flight cost. It’s about activating a highly coordinated, 24/7 global assistance team. When you make that emergency call, you’re not just getting a reimbursement—you’re getting a team of medical directors, logistics experts, and crisis coordinators who manage every single detail of your transport and care.

Decoding Key Evacuation Terminology for Expats

To really understand what you’re buying as an expat, you have to speak the language of the insurers. These aren’t just buzzwords; they define the exact scope of your coverage in a crisis. Getting them straight is the first step in finding the best medical evacuation insurance for your life abroad.

- Medical Evacuation: This is the big one for expats. It means getting you from a place with inadequate medical care to the nearest facility that can properly treat you. That could be a hospital in the next big city or even in a neighboring country.

- Repatriation: This is more specific. It means transporting you all the way back to your home country for medical treatment. It’s often the preferred option for longer-term recovery, putting you close to your family and your home healthcare network.

- Transport to Nearest Adequate Facility: Pay close attention to this phrase, as it’s a standard clause in most policies. It means the insurance company gets to decide what “nearest” and “adequate” mean, and their choice might not be what you’d prefer.

- Transport of Choice: This is a premium feature, but it’s a game-changer for expats. It gives you the power to choose the hospital you’re evacuated to—even one back home—regardless of whether a closer “adequate” facility exists.

These terms are absolutely not interchangeable. A plan that only covers transport to the nearest adequate facility gives you far less control than one that includes repatriation or transport of choice. We break this down even further in our guide to emergency air evacuation insurance costs and coverage.

A Real-World Expat Scenario

Let’s make this real. Imagine an expat, John, working on a project in a remote part of Southeast Asia. He takes a bad fall and suffers a serious injury. The local clinic is small; it doesn’t have the surgeons or advanced imaging equipment to handle his case.

This is where his expat medical insurance with evacuation coverage kicks into high gear.

- The Emergency Call: John or a coworker immediately calls the 24/7 assistance number on his insurance card, providing his policy details and explaining the situation.

- Medical Assessment: The insurer’s medical director gets on the phone with the local doctor. They quickly confirm John’s condition and agree that the clinic is not equipped to provide the necessary care.

- Logistics Coordination: As soon as the evacuation is deemed medically necessary, the logistics team takes over. They arrange for a ground ambulance, fully equipped, to get John to the closest airstrip that can handle the evacuation aircraft.

- Air Ambulance Dispatch: At the same time, an air ambulance is scrambled. On board is a specialized medical crew, like a critical care nurse and a paramedic. The coordination team handles all the red tape—flight clearances, visas, and landing permissions.

- Bedside-to-Bedside Transfer: The flight crew meets John, manages his care during the flight, and stays with him until he’s safely admitted to a major, pre-vetted hospital in a regional hub like Singapore.

- Continuous Monitoring: Throughout the process, the assistance team keeps John’s family updated and stays in touch with the receiving hospital to ensure his care is on track.

In a situation like this, the insurance did far more than just pay for a flight. It orchestrated a complex, high-stakes medical mission from start to finish. This removed an incredible logistical and financial weight from John and his family during one of the most stressful moments of their lives. That coordinated response is the true power of a top-tier expat evacuation plan.

Comparing Top Medical Evacuation Insurance Providers for Expats

Choosing the right medical evacuation insurance isn’t about finding the cheapest plan—it’s about finding a true partner for your life abroad. For expats, this decision goes far beyond what a typical tourist needs. You’re not just covering a two-week vacation; you’re securing a safety net for your long-term health in a foreign country.

While giants like IMG Global, Cigna Global, and GeoBlue dominate the expat insurance field, they each bring a completely different philosophy to the table. One might be perfect for a digital nomad hopping across Southeast Asia, while another is built for a family putting down roots in the Middle East. It all comes down to the fine print of their international medical plans.

You have to look at their experience with long-term care, how they handle pre-existing conditions, and whether they include non-medical security evacuations. The stakes are high. An air ambulance from Europe back to the U.S. can easily top $50,000 without the right coverage.

IMG Global: A Focus On Flexibility for Expats

IMG Global has built its name on flexible, customizable plans that really resonate with the modern expat. Their biggest strength is offering different tiers of coverage, so you can pick and choose benefits to fit your actual needs and budget without paying for things you don’t want.

A key feature for expats is how they seamlessly integrate medical evacuation into their broader international health plans. This means one policy and one point of contact for everything from a routine check-up to a full-blown emergency flight. For expats who value simplicity, that’s a huge win.

IMG is a fantastic fit for expats whose lives aren’t static—think digital nomads, entrepreneurs, or anyone who travels frequently between their home and host countries. Their global network is vast, so you’re almost always near a qualified medical facility.

IMG’s Unique Value: Their modular approach lets you build a plan that truly fits your life. It’s ideal for expats who don’t fit a neat little box and need coverage that can adapt as their circumstances change.

Cigna Global: A Legacy of Global Care for Expats

When you think of a global insurance powerhouse, you think of Cigna. They are known for an enormous, directly-contracted network of hospitals, which for an expat means a much higher chance of direct billing. No one wants to be fumbling with credit cards during a medical emergency.

Their evacuation coverage is robust and deeply embedded within their comprehensive health policies. Cigna is often the provider of choice for corporate clients and expat families who are looking for stability and a proven, reliable track record. Their 24/7 global assistance teams are some of the best in the business, staffed by people who have managed every complex international medical case imaginable.

Cigna’s policies also tend to be more accommodating of pre-existing conditions, although this usually comes with a higher premium. For expats managing chronic health issues, the peace of mind that Cigna offers is often worth every penny. You can find several of their plans in our guide to the top 10 international health insurance plans for expats.

Cigna’s Unique Value: Cigna delivers a premium, high-touch service backed by one of the largest healthcare networks on the planet. This makes them a go-to for expats who prioritize seamless, top-tier care and are willing to invest in that reliability.

GeoBlue: Premier Choice for U.S. Expats Abroad

GeoBlue has a very specific and powerful niche: providing top-tier coverage for U.S. citizens living abroad. Their standout feature is unparalleled access to the elite Blue Cross Blue Shield network back in the United States. For any American expat who wants the option to be flown home for treatment, this is a game-changer.

Their plans are designed with the American consumer in mind, using familiar terminology and structures that are easy to understand. GeoBlue’s global network is also highly curated, focusing on facilities that meet Western standards of care. It’s about quality over quantity, which is incredibly reassuring when you’re in a country with a mixed-bag healthcare system.

On top of that, GeoBlue frequently includes coverage for political unrest and security evacuations. This makes their plans a very strong option for professionals working in politically volatile regions, offering a complete safety net for both medical and security crises.

GeoBlue’s Unique Value: For U.S. expats, GeoBlue is in a class of its own. The ability to tap into the Blue Cross Blue Shield network back home is a benefit that no other international insurer can truly match.

Comparing Leading Medical Evacuation Providers for Expats

To help you see the differences more clearly, we’ve put together a quick comparison of these top-tier providers. This table breaks down their core strengths and shows who they are best suited for in the expat community.

| Provider | Maximum Evacuation Benefit | Key Strengths for Expats | Best Suited For |

|---|---|---|---|

| IMG Global | Often up to $1,000,000 or more | Highly customizable plans; integrated health and evacuation; good for varied budgets. | Digital nomads, entrepreneurs, and expats seeking flexible, tailored coverage. |

| Cigna Global | Typically unlimited within core plans | Massive direct-billing network; strong corporate reputation; comprehensive benefits. | Expat families and corporate assignees who want premium, hassle-free service. |

| GeoBlue | Generally $500,000 to unlimited | Access to the U.S. Blue Cross Blue Shield network; strong security evacuation benefits. | U.S. citizens living abroad who prioritize the option of returning home for care. |

Ultimately, the best provider depends entirely on your personal situation as an expat—your citizenship, your health, your lifestyle, and where you plan to live. By understanding what makes each of these companies unique, you can make a much more informed decision.

Matching Your Expat Profile to the Right Coverage

The best medical evacuation insurance isn’t a one-size-fits-all product. What works perfectly for a young digital nomad could be a disaster for a retired couple managing long-term health needs. The key for any expat is to stop thinking about generic plans and start matching specific policy features to their actual life abroad.

By looking at a few common expat profiles, we can see how different lifestyles and priorities demand very different kinds of coverage. Your age, health, family, and where you’re living all play a huge role. Let’s walk through three real-world expat scenarios to see how this works in practice.

Scenario 1: The Retired Expat Couple in Southeast Asia

Imagine an American couple in their late 60s living a quiet life as expats in a coastal town in Thailand. One of them has a pre-existing heart condition. While they love the lifestyle, they know the local clinic isn’t equipped for a serious cardiac event. Their biggest worry is getting back to a world-class hospital in Bangkok or, even better, their trusted specialists back in the U.S. if something goes wrong.

For this expat couple, a few policy features are absolutely essential:

- Rock-Solid Pre-Existing Condition Coverage: This is their top priority. They need a plan that explicitly covers the acute onset of a chronic condition. Without it, an evacuation for a heart issue could be denied, leaving them with a life-altering bill.

- Repatriation of Choice: A basic plan might only fly them to the “nearest adequate facility,” which could be a hospital in a country they don’t know. They need a premium plan that guarantees repatriation to their home country or a hospital of their choosing. This ensures they get back to the doctors who know their history.

- High Coverage Limits: An air ambulance with ICU-level care is incredibly expensive. A coverage limit of at least $1,000,000 is a must to cover all the medical and logistical costs without a second thought.

For retired expats managing health conditions, the fine print on pre-existing conditions and repatriation isn’t just a detail—it is the policy. Trying to save money by cutting corners here is a gamble they can’t afford to take.

Scenario 2: The Expat Digital Nomad in Latin America

Now, let’s picture a 28-year-old software developer living as a digital nomad, hopping between Colombia, Peru, and Ecuador. She’s healthy and active, often working from small mountain towns. Her risks aren’t chronic diseases but accidents—a bad fall while hiking, a scooter crash, or a sudden illness like dengue fever far from a major city.

Her expat insurance needs are completely different from the retired couple’s. She needs flexibility and a rapid, expert response.

- Adventure Sports Rider: Many standard policies won’t cover injuries from trekking at altitude or even riding a motorbike for fun. She needs a policy that includes an adventure sports rider so she’s protected during her weekend adventures.

- A Proven 24/7 Global Assistance Network: Because she might be in a remote location, the insurance provider’s ability to coordinate a tricky evacuation is critical. She should look for providers known for their logistical expertise in challenging terrain.

- Flexible and Extendable Coverage: As a nomad, her plans change constantly. She needs a policy she can buy or extend while already abroad, giving her the freedom her lifestyle demands.

Scenario 3: The Expat Family in the UAE

Finally, consider an expat family on a corporate assignment in Dubai—two parents in their 40s with a couple of young kids. Their company provides a good local health plan, but they worry about the “what ifs.” What if one of their children develops a rare condition that requires a pediatric specialist in Europe or the United States?

They need to focus on comprehensive, family-oriented benefits that plug the gaps in their corporate insurance.

- Family-Specific Benefits: The right plan for them must include things like transport for an accompanying family member and the return of minor children. These clauses are designed to keep the family together during a medical crisis.

- Choice of Hospital Rider: Dubai has fantastic hospitals, but it may not have the single best specialist for a rare pediatric illness. A “transport of choice” option gives them the power to get their child to the best facility in the world, not just the closest one.

- Bedside Visit Coverage: If one parent is hospitalized for an extended period, this benefit could cover the travel costs for a grandparent to fly in and help with the kids. It’s a small detail that provides massive family support.

These expat scenarios make it clear: your personal situation dictates your insurance needs. Once you analyze your own lifestyle, health, and location, you can move past generic checklists and find the specific policy features that will actually give you peace of mind as an expat.

How to Choose Your Expat Evacuation Plan

Let’s be honest: picking the best medical evacuation insurance from a sea of options feels like a chore. But you can cut through the noise by focusing on what really matters—your specific situation as an expat. Where you’re living, your current health, and your family’s needs are the real starting points for finding a plan that actually protects you.

First, take a hard look at the healthcare system in your host country. Are you in a modern hub with world-class hospitals just around the corner? Or are you somewhere remote, where even basic emergency care is hours away? The bigger the gap between local medical services and the standard of care you need, the more robust your evacuation plan has to be.

This isn’t just about preparing for the absolute worst-case scenario. It’s about staying in control as an expat. The real value here is the peace of mind that comes from knowing you have a pre-approved, expert-led plan ready to get you to top-tier medical care if you need it.

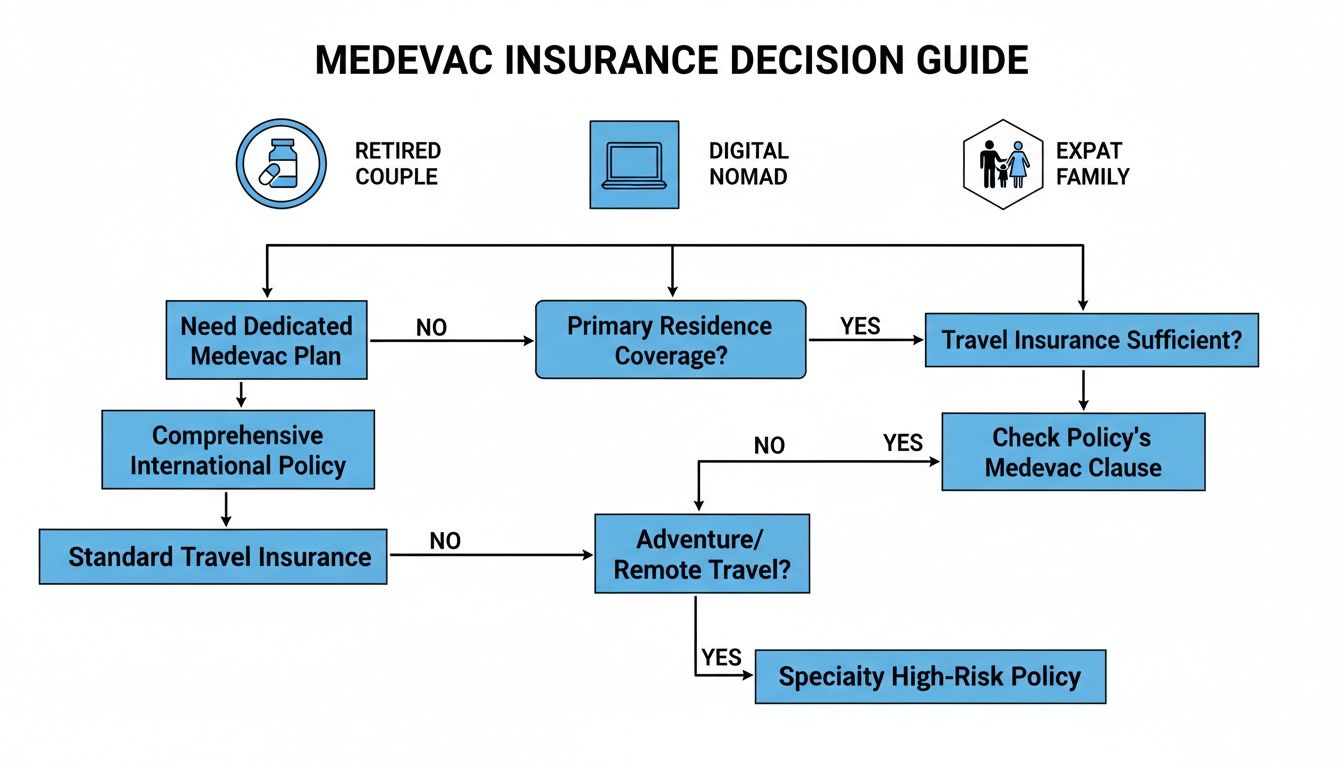

Evaluate Your Personal Expat Risk Profile

Every expat’s life is different, so a one-size-fits-all insurance plan just won’t cut it. A young, healthy digital nomad has entirely different needs than a retiree managing a chronic health condition.

Start by asking some honest questions about your family’s health. Are there pre-existing conditions that absolutely must be covered? Does your lifestyle involve higher-risk activities like scuba diving or mountain trekking that might call for an adventure sports rider? Answering these questions upfront helps you narrow down policies to the ones that fit, preventing dangerous coverage gaps down the road.

This flowchart breaks down the decision-making process for three common expat profiles.

As you can see, your expat lifestyle really drives your priorities. A retired couple might need to focus heavily on pre-existing condition coverage, while a digital nomad working from a remote village needs a provider with proven logistical expertise in tough-to-reach locations.

Scrutinize Policy Details and Provider Networks

Once you know what you need as an expat, it’s time to get into the weeds of the policy documents. Don’t just glance at the coverage limit and call it a day. You need to examine the definitions and, more importantly, the exclusions. A term like “medically necessary” can mean different things to different insurers, so get clarity on that before you sign anything.

The provider’s global assistance network is another make-or-break factor. Remember, you’re not just buying a piece of paper; you’re buying access to a 24/7 crisis management team.

Here are a few key questions to ask any provider you’re considering:

- What is your average response time for dispatching an air ambulance?

- Do you have direct partnerships with hospitals in my region?

- Can you walk me through a real-world example of an evacuation you’ve managed from my host country?

Verifying the strength of the assistance network is essential. An insurer with a proven track record, extensive partnerships, and fast dispatch rates can make all the difference in a life-threatening emergency.

Top providers maintain fleets that service over 150 countries, boasting impressive 95% on-time dispatch rates—a testament to why choosing an operator with a serious global footprint is so critical for any expat.

Common Questions About Expat Medevac Insurance

When you’re planning a life abroad, the details around medical evacuation insurance can feel a bit murky. We get it. To clear things up, here are some straight-talking answers to the questions we hear most often from expats like you.

Does My Expat Health Insurance Already Cover Medical Evacuation?

This is a big one, and the answer isn’t always straightforward. While many comprehensive expat health plans do include an emergency evacuation benefit, you really have to read the fine print. More often than not, this built-in coverage is pretty limited.

Typically, these benefits only cover transport to the “nearest adequate facility.” What does that mean? The insurer picks the hospital, which might be in a neighboring country that’s medically sound but miles away from your family or any support system. A standalone medevac policy or a premium health plan gives you much more say in the matter and comes with much higher benefit limits, often hitting $1,000,000 or more.

These dedicated plans are also where you’ll find “transport of choice” options, letting you get back to a hospital in your home country if that’s what you and your doctors decide is best. Never assume your primary health policy has you fully covered without digging into the specifics.

What Is the Difference Between Medical Evacuation and Repatriation for an Expat?

People often use these terms interchangeably, but in the insurance world, they mean two very different things. Knowing the distinction is crucial for an expat to understand what their policy will actually do in a crisis.

- Medical Evacuation: This is all about getting you from a place with inadequate medical care to the closest facility that can properly treat you. The number one goal is immediate, life-saving care.

- Medical Repatriation: This specifically means bringing you back to your home country (or official country of residence) for medical treatment or to continue your recovery. This is usually the preferred option for longer-term care, keeping you close to family.

A solid medical evacuation plan for expats will spell out coverage for both scenarios. This gives your medical team the flexibility to make the best call when every second counts.

Are My Pre-existing Conditions Covered for an Evacuation?

How a plan handles pre-existing conditions is one of the biggest differentiators you’ll find. Many basic travel policies will simply refuse to cover any emergency that stems from a condition you had before your coverage began.

However, the better plans designed specifically for expats are a bit more sophisticated. Some will cover the “acute onset” of a pre-existing condition—think of it as a sudden, unexpected flare-up that needs immediate attention. Others will offer a full waiver for the condition after you’ve been continuously covered for a set period, like 6 or 12 months.

It’s absolutely critical for expats to be upfront about any chronic conditions when applying. Hiding something can get your claim denied, leaving you holding the bag for an incredibly expensive evacuation bill. Find a plan that acknowledges and addresses your health needs from the start.

Am I Covered in a Politically Unstable Region as an Expat?

This is a common misconception. Standard medical evacuation insurance is for medical emergencies, plain and simple. It almost always excludes evacuations needed because of political events like civil unrest, a coup, or a terrorist attack. If you’re an expat living or working somewhere with a risk of political instability, a standard medevac plan just won’t cut it.

For that kind of situation, you need a completely different type of policy or rider that includes security and political evacuation services. This is a specialized benefit that arranges to get you out of a dangerous non-medical situation. For any expat in a high-risk part of the world, it’s an essential layer of protection.

Beyond the logistics of an evacuation, having reliable international communication methods is just as vital for staying in touch with your family or emergency coordinators during a crisis. Being prepared on that front ensures you can maintain contact when it matters most.

At Expat Global Medical, we help expats sort through these complex details every day. Our team can help you compare plans side-by-side to find coverage that offers real peace of mind, no matter where your journey takes you. Get a free quote today.