")

Relying on your health insurance from back home while you’re living overseas is a massive financial gamble. The simple truth is that these plans are built with geographical borders in mind and are rarely accepted for medical care in other countries. When you move abroad, your home plan essentially stays behind, leaving you completely exposed to potentially huge out-of-pocket bills for everything from a routine check-up to a serious emergency.

Why Your Home Health Plan Won’t Work Abroad

It’s one of the most common—and costly—assumptions expats make: that their existing health insurance will just travel with them. Unfortunately, that’s almost never how it works. A domestic health plan is designed to function within a very specific ecosystem—one country’s healthcare system, its network of doctors, and its unique regulatory rules.

Think of it like a cell phone that’s locked to a specific carrier. It works perfectly within its home network, but the moment you cross an international border, it loses signal and can’t connect. Your domestic insurance policy acts the same way; it loses its “signal” abroad, making it unable to communicate with foreign hospitals and clinics.

The Problem with Provider Networks

The heart of any domestic health plan is its network of hospitals, clinics, and specialists. Insurers hammer out specific, negotiated rates with these providers to keep costs under control. When you step outside this pre-approved network—especially in another country—you’re immediately tagged as an “out-of-network” patient.

This triggers two major problems:

- No Direct Billing: Foreign hospitals have no working relationship with your home insurer. This means they will almost always demand you pay the full cost upfront before you can even be treated.

- Sky-High Costs: Even if your plan offers some token reimbursement for out-of-network care, it’s usually just a tiny fraction of the total bill. You’ll be on the hook for the rest.

Trying to file a claim after the fact is a bureaucratic nightmare. You’re looking at a mountain of international paperwork, currency conversions, and translated medical records, with absolutely no guarantee of approval. To really grasp these limitations, check out our deep dive into why U.S. health insurance doesn’t work abroad.

Relying on a domestic plan overseas is like trying to use the wrong key for a lock. No matter how much you jiggle it, it simply won’t open the door to local healthcare access. You need a key specifically designed for global use—which is exactly what expat medical insurance provides.

Navigating Foreign Healthcare Systems

On top of all that, every country has its own unique healthcare system, billing practices, and legal requirements. Your domestic insurer simply isn’t built to navigate these foreign complexities. They don’t have relationships with international providers or any real understanding of the local standards of care.

This fundamental disconnect is why specialized expat medical insurance isn’t just a nice-to-have; it’s an absolute necessity. It’s built from the ground up for a global lifestyle. It offers worldwide coverage, direct payment arrangements with international hospitals, and 24/7 assistance from people who actually understand the challenges of getting care far from home. It’s the only real way to make sure your health and your finances are secure, no matter where your journey takes you.

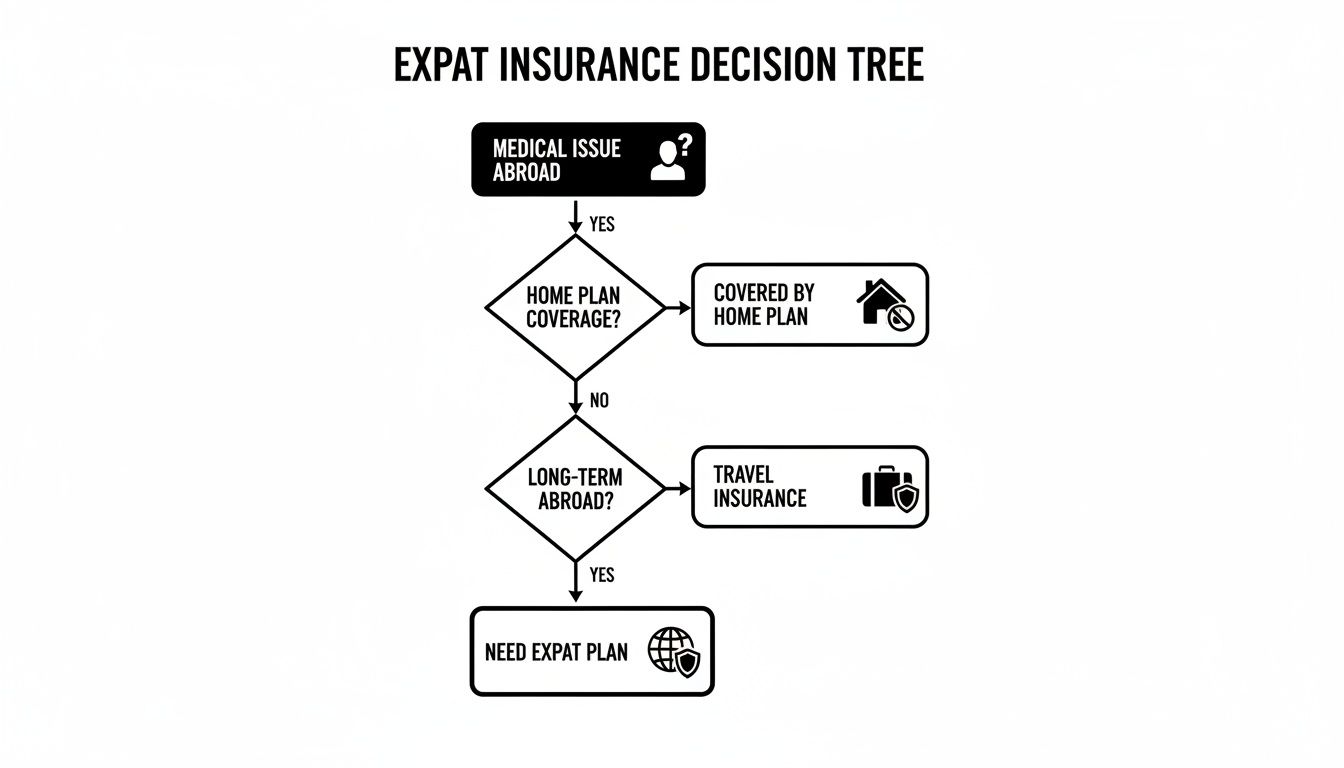

Choosing the Right Type of International Medical Plan

Picking the right international medical plan isn’t just about ticking a box before you leave; it’s about matching your coverage to the reality of your life abroad. The best policy is always the one that fits the length and style of your journey. After all, a two-week vacation has completely different needs than a multi-year relocation, and your insurance should reflect that.

This simple decision tree gets right to the heart of why a specialized plan is often non-negotiable once you realize your domestic insurance won’t cover you overseas.

As you can see, once a medical issue pops up and your home plan says “no,” your only real path forward is a dedicated international plan. The big question then becomes: which one is right for you?

Short-Term Travel Medical Insurance

Think of travel medical insurance as your temporary safety net. It’s designed for unexpected emergencies that can derail a trip, making it perfect for vacations, business travel, or any international stay lasting from a few days up to a year. Its sole purpose is to handle unforeseen accidents or sudden illnesses.

What it isn’t designed for is routine care. These plans almost always exclude things like preventive check-ups, ongoing treatments for chronic conditions, or annual wellness visits. It’s a fantastic, cost-effective solution for short trips, but it’s not built for someone actually living abroad.

Long-Term Expat Medical Insurance

Now, if you’re making a new country your home for one year or more, you need a true expat medical insurance plan. This is the heavy-hitter, designed to act just like the comprehensive health plan you’d have back home, but with a global footprint. These policies cover the full spectrum of your healthcare needs.

This typically includes:

- Inpatient Care: Hospital stays, major surgeries, and other significant medical procedures.

- Outpatient Care: Routine doctor’s visits, specialist appointments, and prescriptions.

- Wellness and Preventive Services: Many plans will cover annual physicals, screenings, and vaccinations.

- Optional Benefits: You can almost always add on extras like dental, vision, and maternity coverage.

A long-term expat policy becomes your primary medical plan while living overseas. It’s built for the long haul, giving you peace of mind that both emergencies and everyday health needs are covered, no matter where you find yourself.

Emergency Medical Evacuation Plans

Sometimes, the nearest clinic just isn’t equipped to handle a serious injury or illness. That’s where emergency medical evacuation insurance comes in. It’s a specialized policy that covers the staggering cost of transporting you to the closest high-quality medical facility. This can be a standalone plan, but more often, it’s a critical feature baked into a comprehensive expat policy.

Considering an air ambulance can easily top $100,000, this coverage is a must-have for anyone living or traveling in remote areas or in countries with less-developed healthcare systems.

Group Plans for International Employees

For companies with employees working overseas, group expat medical insurance is the simplest and most effective solution. These plans offer consistent, high-quality medical coverage for the entire global team, ensuring every employee has reliable access to care. It streamlines the administrative work for the employer and gives workers and their families total confidence in their health security while on assignment.

To help you visualize where you might fit, the table below offers a quick, side-by-side comparison of these plan types. For a deeper dive, check out our guide comparing expat medical insurance vs. travel insurance.

Comparing International Medical Insurance Plans

Here’s a side-by-side comparison to help you quickly identify which plan type matches your international journey.

| Plan Type | Ideal For | Typical Duration | Primary Focus |

|---|---|---|---|

| Short-Term Travel Medical | Tourists, vacationers, and short business trips. | Up to 1 year | Acute emergencies and unexpected illnesses. |

| Long-Term Expat Medical | Expats, retirees, and digital nomads living abroad. | 1+ year (renewable) | Comprehensive inpatient and outpatient medical care. |

| Medical Evacuation | Anyone in a remote area or a country with limited care. | Varies | Emergency transport to an adequate medical facility. |

| International Group Plans | Companies with employees based in multiple countries. | Ongoing | Consistent, quality healthcare for a global workforce. |

At the end of the day, picking the right plan starts with an honest look at your life abroad. Are you on a temporary adventure, or are you putting down new roots? Answering that one question will point you directly to the policy designed to protect you best.

What a Strong Expat Medical Insurance Policy Includes

Looking at an insurance policy can feel like trying to read a different language, full of jargon and tiny print. But figuring out what’s inside is the only way to know you’re actually protected. A solid expat medical insurance plan isn’t just one single thing; it’s built from several core pieces, and each one plays a vital role in keeping you safe and financially secure while you’re living abroad.

Think of it like packing a backpack for a long, unpredictable journey. Some parts are the non-negotiable frame that gives it structure, while others are specialized pockets you add based on where you’re going and what you’ll be doing.

Let’s unpack the essentials.

The Foundation: Inpatient and Outpatient Care

At the heart of any quality plan are two types of coverage. They work together to handle everything from a minor bug to a major medical crisis.

Inpatient Care is the absolute cornerstone of your policy. This is for any treatment that requires you to be admitted to a hospital. We’re talking about the big stuff:

- Major surgeries and the procedures that go with them

- Overnight hospital stays (usually in a semi-private room)

- Intensive care unit (ICU) costs

- Diagnostic tests like MRIs or CT scans that happen while you’re admitted

Outpatient Care covers all the medical needs that don’t require a hospital stay. This is your day-to-day health maintenance, like routine doctor’s visits, appointments with specialists, prescription drugs, and lab work. Some bare-bones plans might only cover inpatient care to keep the price down, but a truly effective expat policy needs both.

Lifesaving Benefits: Evacuation and Repatriation

For many expats, especially those living in more remote spots or in countries with developing healthcare, these benefits are completely non-negotiable. They act as a critical safety net when local hospitals just aren’t equipped to handle a serious illness or injury.

Emergency Medical Evacuation covers the often-shocking cost—sometimes over $100,000—of getting you to the nearest medical facility that can give you the right level of care. Repatriation, on the other hand, covers the cost of getting you all the way back to your home country for treatment if it’s medically necessary.

These two benefits alone can stop a medical crisis from turning into a full-blown financial catastrophe. They are a true hallmark of a reliable expat plan.

Customizing Your Coverage: Key Policy Terms

Beyond the core benefits, a few key terms define how your plan actually works and how much you’ll end up paying out-of-pocket. Getting these right is how you match a policy to your budget and comfort level with risk.

- Deductible: This is the amount you pay for your medical care before your insurance company starts chipping in. If you have a $1,000 deductible, you’re on the hook for the first $1,000 of your medical bills. A higher deductible usually means a lower monthly premium.

- Coinsurance/Copay: This is your share of the costs after you’ve met your deductible. A copay is a flat fee (like $25 every time you see a doctor), while coinsurance is a percentage (for example, you pay 20% of the bill, and the insurer pays the other 80%).

- Coverage Area: This simply defines the geographic region where your plan will cover you. Common options include “Worldwide” or “Worldwide excluding the USA.” Because U.S. healthcare is incredibly expensive, choosing a plan that excludes it can dramatically lower your premium.

By carefully balancing these elements, you can build a plan that gives you serious protection without being a massive financial burden. The goal is to find that sweet spot where your premium is manageable, but your potential out-of-pocket risk is kept in check.

Understanding Policy Exclusions and Pre-Existing Conditions

The real value of any insurance policy isn’t just in what it covers—it’s in what it doesn’t. This is where the fine print, especially the sections on exclusions and pre-existing conditions, becomes incredibly important. Honestly, this is where many expats get caught by surprise, and it’s critical to get a handle on these details to avoid a denied claim right when you need help the most.

Think of exclusions as the built-in rules of the game. They are specific situations, treatments, or conditions the policy simply won’t pay for. Insurers put them in place to manage risk and keep plans from becoming outrageously expensive. While the exact list varies from one carrier to the next, a few usual suspects pop up on almost every expat medical plan.

Common Policy Exclusions to Look For

It’s so important to actually read your policy documents to see what isn’t covered. Most plans are very clear about what they will and won’t pay for.

Here are some of the most common exclusions you’ll run into:

- Elective or Cosmetic Procedures: Any treatment that isn’t medically necessary, like plastic surgery, is almost always on you.

- High-Risk Hobbies: If you get injured while scuba diving, rock climbing, or playing professional sports, you might not be covered unless you buy a special add-on.

- Self-Inflicted Injuries: Harm that results from substance abuse or suicide attempts is typically excluded.

- Fertility Treatments: Services like IVF are usually excluded from standard plans. You’d need a specific maternity rider for this type of care.

- Acts of War or Terrorism: Medical costs that come from these kinds of events are a universal exclusion in standard policies.

To really dig into the nitty-gritty of your policy’s fine print, using a contract review checklist can be a huge help. It gives you a systematic way to make sure you don’t miss anything important.

Navigating Pre-Existing Conditions

So, what’s a pre-existing condition? It’s any medical issue—think asthma, diabetes, high blood pressure—that you were diagnosed with or treated for before your new insurance coverage kicked in. How an insurer handles these conditions is one of the biggest factors you’ll need to consider when picking a plan. They generally take one of two paths.

Full Medical Underwriting (FMU): This is a deep dive into your health history. You’ll provide all your medical details, and the insurer analyzes everything to decide if they can cover your pre-existing conditions. Sometimes they’ll offer coverage with a higher premium or exclude that specific condition.

Moratorium Underwriting: This is a much simpler, “wait-and-see” approach. The insurer doesn’t ask for your full medical history upfront. Instead, they put a waiting period in place, which is often 24 months. If you don’t have symptoms or need any treatment for a pre-existing condition during that time, it might become eligible for coverage afterward.

For example, let’s say an expat has well-managed asthma. With FMU, they might be accepted with full coverage, maybe for a slightly higher price. But under a moratorium plan, any care related to their asthma would likely be excluded for the first two years. Getting familiar with how insurers look at pre-existing conditions for travel and expat insurance can give you a lot more clarity here.

Deciding between these two really comes down to your health background and what you’re comfortable with. Full underwriting gives you certainty from day one, while a moratorium is easier to apply for but comes with those initial limitations. Knowing the difference empowers you to pick a policy that truly fits your needs and won’t leave you with a costly gap in your global medical safety net.

Picking the Right Insurance Provider and Medical Network

Choosing an expat medical insurance policy is only half the battle. The company behind that policy is just as important—maybe even more so. A fantastic plan from an unreliable provider can quickly turn into a nightmare of denied claims and endless frustration. Partnering with a stable, responsive, and reputable insurance carrier is the foundation of your peace of mind and financial security abroad.

Think of your insurance provider as your most critical support line. When a medical issue pops up thousands of miles from home, you need a team that actually answers the phone, processes claims without a fuss, and has the financial muscle to cover your bills, no questions asked.

How to Vet Insurance Carriers

Let’s be clear: not all insurers are created equal. You can get a good feel for a provider’s reliability by looking at a few key things that reveal their stability and how much they actually care about their customers.

- Financial Strength Ratings: Independent agencies like A.M. Best and Standard & Poor’s are the watchdogs of the insurance world. They rate the financial health of these companies. A high rating (like an A or A+) is a strong signal that the carrier can pay claims, even if the global economy takes a nosedive.

- Customer Service Responsiveness: Dive into reviews and testimonials from other expats. How quickly does the provider answer emails or calls? Do they offer 24/7 multilingual support? This is your sneak peek into how they’ll treat you during a real emergency.

- Claims Process Efficiency: Look for a simple, straightforward claims process. The best providers have online portals and mobile apps that make submitting and tracking claims easy, whether you’re in a bustling city or a remote village.

Direct Billing vs. Pay-and-Claim: Why It Matters

Understanding how a provider’s medical network operates is a huge deal because it directly affects your wallet during a medical event. You’ll run into two main models.

A direct billing network is the gold standard. Here, the hospital or clinic sends the bill for covered services straight to your insurance company. This means you aren’t forced to pay large sums out of your own pocket.

On the flip side, a pay-and-claim model requires you to pay the entire medical bill upfront. You then have to gather all your receipts and submit them to the insurer to get reimbursed later.

Choosing a provider with an extensive direct billing network saves you from the financial stress of fronting thousands of dollars for care. It’s the difference between a minor inconvenience and a major financial headache.

The Role of a Specialized Broker

Trying to navigate this all on your own can feel overwhelming. The global insurance market is massive, and many countries have specific visa rules, like the Schengen Area’s requirement for a minimum of €30,000 in coverage. This is where a specialized broker, like us here at Expat Global Medical, becomes your most valuable ally.

A broker works for you, not the insurance companies. We compare plans from top-tier carriers like Cigna, GeoBlue, and others to find the perfect match for your destination, health needs, and budget. This guidance is more critical than ever in a market that’s booming; the international health insurance sector was valued at USD 31.68 billion and is expected to hit USD 44.29 billion by 2029. You can find more insights on the international health insurance market growth on ResearchAndMarkets.com.

Ultimately, our expertise helps you find a reliable partner you can count on during your global journey.

Answering Your Top Expat Medical Insurance Questions

Deciding on the right global medical coverage can bring up a lot of questions. That’s perfectly natural. This section is all about giving you clear, direct answers to the most common concerns we hear from expats every day. Think of it as your quick-reference guide to clear up any confusion and help you move forward with confidence.

Even with the best plan in hand, unexpected situations can pop up. By getting a handle on how your policy really works, you can navigate those moments without the added stress. Let’s dive into some of the questions we get asked the most.

Can I Keep My Expat Medical Insurance If I Move Again?

Yes, you absolutely can. Portability is a core feature of any good expat medical insurance plan. These policies are built from the ground up to move with you from one country to another, which is one of the biggest things that sets them apart from local, country-specific insurance.

When you’re ready to relocate, you just need to let your insurer know your new country of residence. Your premium might get adjusted up or down to reflect the healthcare costs in your new home, but your coverage itself stays seamless. It’s always a good idea to confirm the details with your provider before you pack your bags to make sure the transition is smooth.

Does My Plan Cover Visits to My Home Country?

This is a great question, and the answer really depends on the specific policy. Many plans do include what’s called “home country coverage,” but it’s usually for a limited time—often between 30 to 90 days per year. This benefit is typically meant for acute medical needs or emergencies that come up during a visit, not for planned check-ups or elective procedures.

If you know you’ll be spending a lot of time back home, especially in a high-cost country like the United States, it’s critical to double-check that your policy offers enough coverage. If it doesn’t, you might want to look into a separate plan just for those trips.

An insurer is the company that underwrites the policy and pays the claims. A broker is an independent advisor who works for you. A specialist broker compares plans from multiple top-rated insurers to find the best fit for your unique situation.

When Should I Apply for Expat Medical Insurance?

The sooner, the better. We strongly recommend starting the application process at least 30 to 60 days before you move or before your current coverage runs out.

Giving yourself this window provides plenty of time for the underwriting process, which is where the insurer reviews your medical history to finalize your policy. Applying early is the single best thing you can do to guarantee you have no gaps in coverage, protecting both your health and your finances from day one of your new life abroad.

Beyond the nitty-gritty of expat medical insurance, it’s smart to understand the bigger picture of staying protected during a move. For some more general advice, you can check out these essential insurance tips for a stress-free move. Having a complete view of your insurance needs helps ensure every part of your relocation is secure.

Figuring out global medical plans doesn’t have to be a headache. At Expat Global Medical, our team of specialists is here to give you clear answers and help you compare top-tier plans from the world’s most trusted insurance carriers. Get your free, no-obligation quote today and take the first step toward securing your health and peace of mind, no matter where you are in the world. Learn more at https://expatglobalmedical.com.