")

So, you’re moving abroad. It’s an exciting thought, but there’s one critical detail that often gets overlooked until it’s too late: health insurance. Let’s be clear: health insurance for American expats isn’t just a nice-to-have; it’s a specialized shield designed for long-term global living. Why? Because the domestic U.S. health plan you have right now—whether from your employer or the ACA marketplace—offers little to no real coverage once you’re overseas.

This gap leaves you financially exposed to everything from a routine check-up to a serious medical emergency. The only reliable way to protect yourself and your savings is to secure a dedicated expat medical insurance plan built for the realities of life abroad.

Why Your US Health Plan Falls Short Abroad

Think of that health insurance card in your wallet. It feels like a safety net, right? Unfortunately, that net has a massive hole in it the second your new home is outside the United States. Domestic insurance is fundamentally built for the American healthcare system—its networks, its billing codes, and its borders.

Relying on a U.S. plan overseas is like using a state driver’s license to cross international borders. It’s simply not the right tool for the job. This isn’t just an inconvenience; it’s a massive financial gamble that can turn a manageable health issue into a full-blown crisis.

To give you a clearer picture, let’s break down the core differences.

US Domestic vs. Expat Medical Insurance at a Glance

This table lays out the fundamental mismatch between what your U.S. plan offers and what you actually need as an expat.

| Feature | Typical U.S. Health Plan | Expat Medical Insurance |

|---|---|---|

| Geographic Coverage | Limited to the U.S.; emergency coverage abroad is minimal and rare. | Global or regional coverage, designed for living in other countries. |

| Provider Network | U.S.-based network of doctors and hospitals (HMO, PPO, etc.). | Extensive international network of providers with direct billing. |

| Routine & Preventive Care | Covered within the U.S. network. | Covered globally, allowing for regular check-ups in your host country. |

| Direct Billing | Only available at in-network U.S. providers. | Standard feature at in-network international hospitals. |

| Medical Evacuation | Not typically included. | A core benefit for transport to adequate medical facilities. |

| Policy Duration | Annual, tied to U.S. residency or employment. | Long-term and annually renewable, designed for a global lifestyle. |

| Ideal For | Individuals and families living inside the United States. | Expats, digital nomads, and global retirees living outside the U.S. |

As you can see, these two types of insurance are built for entirely different worlds. One is for staying put, the other is for living globally.

The Geographic Limitations of Domestic Coverage

The root of the problem is geography. Your U.S. insurer’s network of approved doctors and hospitals simply doesn’t exist overseas. For an American living abroad, this creates a domino effect of problems:

- No In-Network Access: Finding a local doctor who is “in-network” with Blue Cross Blue Shield of Texas is next to impossible in Tokyo or Lisbon. This means you’re paying out-of-pocket for virtually everything.

- Reimbursement Nightmares: Even if your plan has some flimsy out-of-network emergency benefit, you’re in for a world of hurt. You’ll be navigating a maze of paperwork, currency conversions, and language barriers just to get a fraction of your money back—months later.

- Paying Upfront for Everything: Imagine needing emergency surgery that costs tens of thousands of dollars. With a domestic plan, you’ll be expected to pay that entire bill on the spot and then try to get reimbursed. It’s a recipe for financial disaster.

This reality makes it painfully clear: a completely different approach to healthcare is non-negotiable for expat life.

Relying on a US-based health plan abroad is a gamble with your health and finances. Specialized health insurance for American expats is not an optional upgrade; it’s a fundamental requirement for a secure life overseas.

The Scale of the Coverage Gap

To understand why this gap is so vast, you just have to look at how U.S. healthcare is structured. Employer-sponsored plans, which cover around 154 million Americans (53.7% of the insured population), are designed to function only within the U.S. system. They inherently exclude or poorly reimburse foreign medical care, leaving expats dangerously exposed. You can find more U.S. health insurance statistics on Statista.com.

Domestic plans simply aren’t built for global logistics. They don’t have the international partnerships, billing agreements, or support infrastructure to provide seamless care in another country. This is precisely where specialized expat medical insurance steps in, offering a safety net designed from the ground up for the unique challenges and opportunities of living abroad.

The Hidden Gaps in Your US Insurance Plan When You’re Overseas

Thinking you can rely on your good old US health insurance while living abroad is a common mistake, but it’s a gamble you don’t want to take. Your policy might mention “emergency overseas coverage,” but in the real world, that fine print hides a minefield of gaps that only become obvious when you’re in a real crisis.

Picture this: you have an accident in Spain and need urgent surgery. You hand over your US insurance card, but the hospital staff just shakes their head. They have no idea who your provider is and demand €30,000 upfront before they’ll even wheel you into the operating room. This isn’t some made-up horror story; it’s how things often work. Suddenly, you’re on the hook for the entire bill, just hoping you’ll get some of it back from your insurer months later.

The Real-World Nightmare of Getting Care

Even if your plan promises to reimburse you for out-of-network costs, the day-to-day logistics are a nightmare. When a medical issue pops up, there’s no 24/7 global support line to call. Instead, you’re hit with a wall of practical problems that make getting decent care feel almost impossible.

- Trapped by Time Zones: Need to get an MRI pre-authorized? Good luck. Your insurer’s office in Chicago is closed for the next eight hours. These kinds of delays can stall critical treatments and put your health on the line.

- The Currency Conversion Mess: You pay a hospital bill in Thai Baht. Your insurer only deals in US dollars, leaving you to figure out the complicated currency conversions. You’ll almost certainly lose a chunk of money in the exchange.

- Lost in Translation (and Paperwork): To file a claim, you’ll likely need to get all your medical records translated. On top of that, you have to fill out complex forms that the local hospital staff has never seen before. The burden of managing it all falls squarely on your shoulders, right when you’re at your most vulnerable.

These aren’t just small headaches. They are major roadblocks that prevent you from getting the care you need, when you need it.

A domestic health plan is built for a domestic healthcare system. Expecting it to work flawlessly overseas is like trying to use your house key to start your car—it’s the wrong tool for the job, and the results can be disastrous.

The Medicare Black Hole

For American retirees, the problem is even simpler and more severe. Medicare, the health plan for over 65 million Americans, provides almost zero coverage outside the United States. With a few very rare exceptions, your Medicare card is just a useless piece of plastic once you move abroad.

This leaves millions of Americans retiring in popular spots like Mexico, Portugal, or Costa Rica completely unprotected. A simple fall could result in a hospital bill that wipes out their savings, with no help from their US-based plan.

This hard reality makes one thing crystal clear: specialized health insurance for American expats isn’t just a “nice-to-have.” It’s a fundamental requirement for a secure and stable life abroad. It’s designed to fill all the gaps your domestic plan leaves behind, offering direct-billing networks, multi-lingual support, and the kind of financial security that actually fits an international life.

Understanding Your Expat Medical Insurance Options

Figuring out international health coverage can feel overwhelming, but it really just comes down to a few core types of plans. Each one is built for a specific purpose. The trick is to match the policy to your actual life as an American abroad and avoid the classic mistake of picking a plan that doesn’t fit your long-term needs.

Think of it like choosing a vehicle. You wouldn’t take a scooter on a cross-country road trip or use a moving truck for a quick run to the grocery store. In the same way, the insurance that’s perfect for a two-week vacation is dangerously wrong for someone living overseas for a year or more.

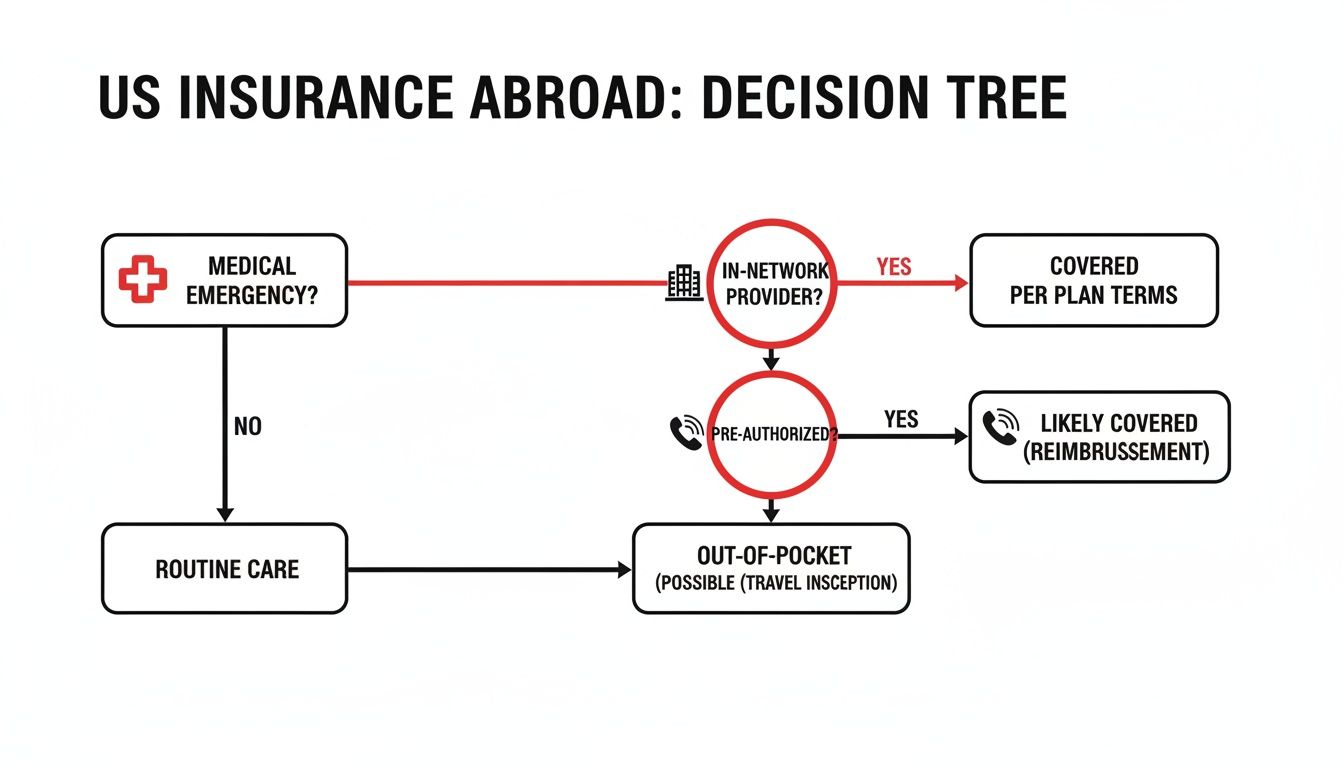

This decision tree shows just how complicated—and often impossible—it is to rely on a U.S. plan for a medical emergency abroad. You can see all the different points where coverage can break down.

As you can see, trying to use domestic insurance overseas throws up huge roadblocks, from finding an in-network doctor to getting pre-authorizations approved. More often than not, it leads to you paying the entire bill out-of-pocket.

International Major Medical Insurance: Your Global Primary Plan

For anyone living abroad, the most important coverage you can have is International Major Medical Insurance. This is the real deal—a long-term solution designed specifically for expats. Think of it as a direct replacement for your employer-sponsored plan back home, but with a global footprint.

These plans are built to cover everything. We’re talking routine doctor visits, preventive care, major hospital stays, surgeries, and even managing chronic conditions. They provide comprehensive, renewable coverage that acts as your primary health safety net in your new country and, in many cases, worldwide.

An International Major Medical plan is your foundation for a secure life abroad. It’s designed for residency, not just a trip, giving you the robust, long-term coverage you need to handle both everyday health and unexpected crises with confidence.

Travel Insurance: A Short-Term Emergency Fix

Here is where so many people get it wrong. Travel Insurance is designed for one thing and one thing only: short-term trips. It’s perfect for a vacation or a business trip, usually for any journey under 90 days. Its main job is to cover sudden emergencies—like an unexpected illness or a freak accident—and get you stable enough to fly home for proper treatment.

It is completely inadequate for actually living abroad. Travel insurance almost never covers:

- Routine or preventive care: Forget about annual check-ups, screenings, or vaccinations.

- Pre-existing conditions: Most policies will exclude any ongoing medical issues you already have.

- Long-term treatment: It’s not built for managing chronic illnesses or any kind of ongoing care.

Relying on travel insurance while you’re an expat leaves you dangerously exposed. It’s a temporary solution for a permanent lifestyle change.

Medical Evacuation Insurance: Your Lifeline Home

Sometimes, the best medical care just isn’t available where you are, especially if you’re living in a remote area or a developing country. That’s when Medical Evacuation Insurance becomes an absolute lifeline. This specialized policy pays for emergency transportation to the nearest top-tier medical facility, which might be in another city or even another country entirely.

For example, imagine suffering a serious injury while living in a rural part of Southeast Asia. An evacuation plan would cover the cost of an air ambulance to a world-class hospital in Bangkok or Singapore. Without it, you’d be on the hook for a bill that could easily top $100,000. It’s an essential piece of any expat’s financial protection, and thankfully, many international major medical plans already include it.

Regional and Local Plans: Focused Coverage

Finally, not every expat needs coverage that spans the entire globe. If you plan on staying put in one country or region for the long haul, there are a couple of other options that might work well.

- Regional Plans: These policies cover you within a specific geographic zone, like Europe or Latin America. They’re often a bit more affordable than a full-blown worldwide plan.

- Local Plans: In many countries, you can buy a private health plan meant for residents. While they can be cost-effective, these plans won’t cover you if you travel outside that country. You might also run into language barriers or find that the standards of care are different from what you’re used to.

The bottom line is that your lifestyle dictates your insurance needs. Whether you’re a globe-trotting digital nomad, a retiree settled in one place, or a corporate assignee, matching your life to the right plan is the first and most important step.

To help you visualize the options, we’ve put together a simple table that breaks down which plan works best for different situations.

Which Expat Medical Insurance Plan Is Right for You?

| Plan Type | Best For | Coverage Duration | Key Feature |

|---|---|---|---|

| International Major Medical | Long-term expats, digital nomads, retirees living abroad | Annual, renewable (long-term) | Comprehensive health coverage, like a domestic plan but global. |

| Travel Insurance | Tourists, vacationers, short business trips | Per trip (typically under 90 days) | Emergency medical care and trip-related issues like cancellations. |

| Medical Evacuation | Expats in remote areas or countries with limited healthcare | Annual or per trip | Covers emergency transport to a capable hospital, which can cost six figures. |

| Regional/Local Plan | Expats staying within one country or specific region | Annual, renewable | More affordable, but coverage is geographically restricted. |

Choosing the right type of insurance is the bedrock of a safe and financially secure life abroad. Once you know which category you fall into, you can start comparing specific policies and providers to find the perfect fit.

What Drives the Cost of Your Expat Medical Insurance

Figuring out the price tag on health insurance for American expats isn’t as mysterious as it sounds. Think of it like booking a custom trip—the final cost really comes down to the destinations you pick and the upgrades you add. Once you get a handle on the main factors, you can find that perfect sweet spot between solid coverage and a price that feels right.

A few key variables shape your monthly or annual premium. Knowing what they are puts you in the driver’s seat, allowing you to tailor a plan that fits your health needs and your wallet. Let’s pull back the curtain on what really drives the cost.

Age and Location Your Two Biggest Factors

No surprise here: your age plays a big role. As we get older, we’re statistically more likely to need medical care, so insurers use age as a baseline for risk. It’s a standard part of the calculation across the board, and you’ll see premiums naturally rise over time.

But where you decide to hang your hat as an expat has just as big of an impact. The price of healthcare varies wildly around the globe. A plan covering you in Switzerland, where medical costs are sky-high, is going to be far more expensive than one for Thailand or Mexico. For example, the average annual cost for health insurance in Mexico is around $5,485, but that can leap to over $8,300 in a high-cost hub like Hong Kong.

Your Coverage Area Worldwide vs Regional

The geographic scope of your plan is another major lever you can pull to adjust your costs. Insurers offer a few different options, and your choice will directly move the needle on your premium.

- Worldwide Coverage: This is the top-tier, most expensive option. It covers you literally anywhere on the planet.

- Worldwide Excluding the USA: A hugely popular choice for American expats, and for good reason. U.S. healthcare is notoriously pricey, so excluding it from your plan can lead to massive savings—often cutting your premium by 30-50%.

- Regional Coverage: If you know you’ll be staying within a specific part of the world, like Europe or Southeast Asia, a regional plan can be a seriously cost-effective move.

Choosing the right coverage area is all about matching the policy to your actual life. If you have no plans to return to the U.S. for medical care, excluding it is one of the smartest financial decisions you can make.

The single most effective way for many American expats to lower their insurance premium is by choosing a “Worldwide excluding the USA” plan. This simple adjustment can make high-quality global coverage much more affordable.

Policy Structure Deductibles and Benefits

Finally, the nuts and bolts of your plan play a huge role in the final price. Think of these as the fine-tuning dials on your policy.

Your deductible is what you pay out-of-pocket before your insurance kicks in. A higher deductible means you’re taking on more of the initial risk, which brings your monthly premium down. On the flip side, a lower deductible gets your insurance paying sooner but means a higher premium. There’s no right or wrong answer here; it’s a personal call based on your finances and comfort with risk.

On top of that, any optional benefits you tack on will add to the price. Some common add-ons include:

- Comprehensive dental and vision care

- Maternity coverage for those planning to start or grow a family

- Wellness benefits like annual health check-ups

By carefully choosing your location, coverage area, deductible, and optional benefits, you can effectively build a custom health insurance for American expats plan. It’s all about knowing which levers to pull to get great protection without breaking the bank.

How to Choose the Right Expat Insurance Plan

Picking the right health insurance for American expats is about a lot more than just finding the lowest monthly premium. Think of it like choosing a business partner for your health. A cheap price tag is worthless if that partner vanishes when a crisis hits, leaving you with a mountain of unexpected bills and a logistical nightmare.

The real goal is to find a policy that delivers genuine peace of mind, not just a policy number. This means you’ve got to look under the hood at the details that truly count—things like the provider network, how they handle claims, and the fine print that spells out what is (and isn’t) covered. A little homework now can save you from massive headaches later.

Evaluate the Provider Network

The strength of an insurer’s network is one of the most critical pieces of the puzzle. A network is simply the group of hospitals, clinics, and doctors that have a direct billing agreement with your insurance company. Sticking with providers in this network is the secret to a smooth, cashless experience.

When you’re comparing plans from carriers like Cigna or GeoBlue, don’t just glance at the network map. You need to dig a little deeper:

- Check for Quality Hospitals: Does the network include top-rated, modern hospitals in your new city? The last thing you want in an emergency is to be stuck with subpar facilities.

- Look for English-Speaking Providers: Especially when you’re just getting settled, having access to doctors who speak your language is a massive relief. Most good expat plans make it easy to find these providers in their directories.

- Assess Accessibility: Are the in-network clinics and hospitals right around the corner, or are they a two-hour drive away? Proximity is a big deal when you’re not feeling your best.

A strong, accessible network makes all the difference. It’s what separates a seamless hospital visit from being forced to pay thousands of dollars out-of-pocket and then chasing a reimbursement.

Scrutinize the Claims and Reimbursement Process

Even with a fantastic network, there will be times you need to see a doctor who is “out-of-network.” When that happens, you’ll typically have to pay the bill yourself and then file a claim to get your money back. A clunky, complicated claims process can turn a minor doctor’s visit into a major source of frustration.

Look for insurers that are known for a straightforward and efficient system. Do they offer a simple online portal or a mobile app for submitting claims? How quickly do they usually pay people back? Reading reviews from other expats is a great way to get the real story on a company’s performance. An insurer that settles claims in 48 hours is a world away from one that takes months.

Understand the Policy Fine Print

The policy document is your contract with the insurer, and it’s crucial to actually read it before you sign anything. This is where you’ll find the nitty-gritty details that can make or break your coverage. Pay close attention to these key terms.

Annual Maximums: This is the absolute most your insurer will pay for your medical care in a single policy year. While a $1 million limit might sound like a lot, a serious medical event could burn through that faster than you’d think. Make sure the maximum is high enough for the healthcare costs in your new country.

Exclusions: Every policy has a list of things it simply won’t cover. Common exclusions include treatment for some pre-existing conditions (or they might have a waiting period), certain elective surgeries, and injuries from high-risk hobbies like skydiving. Knowing these limits upfront prevents devastating surprises down the road.

Choosing the right expat insurance plan is about more than just coverage—it’s about securing a reliable partner for your health and financial well-being. A plan that is clear, accessible, and responsive provides the confidence to fully embrace your new life abroad.

Imagine packing your bags for an exciting new life in Dubai or Mexico, only to realize that a simple accident could wipe out your savings because you skimped on health insurance. There are over 87 million expats living and working around the globe, a staggering number that’s fueling explosive growth in the expat insurance market. Valued at USD 331 million, this market is projected to jump to USD 355 million and keep climbing, thanks to rising global mobility and companies needing to cover their international employees. Learn more about the expanding expat insurance market on IntelMarketResearch.com.

By taking a systematic approach—evaluating the network, understanding the claims process, and reading the fine print—you can confidently compare plans and choose a partner that offers true security for your global journey.

Securing Your Health and Peace of Mind Abroad

You’ve made it this far, which means you’re now miles ahead of most people planning a life abroad. You get why your U.S. health plan just won’t cut it overseas, you can tell the difference between the major types of global coverage, and you know what to look for when picking a policy. Honestly, taking the time to nail down the right insurance is one of the single most important things you can do for a successful, stress-free move.

Think of it as the foundation for your entire adventure. With the right protection in place, you can build your new life with total confidence, knowing you and your family are shielded from staggering medical bills or logistical nightmares. It’s the one thing that truly turns uncertainty into security, freeing you up to focus on the excitement of it all.

From Knowledge to Action

Going from understanding these concepts to actually choosing a plan is a big step. You’ve learned about the comprehensive major medical plans for long-term living, the short-term safety net of travel insurance, and the critical role of emergency transport. Knowing these details gives you the power to see the real value in specific benefits. For instance, if you need a quick reminder, it’s worth understanding exactly what medical evacuation insurance is and how it provides a lifeline in a true crisis. This is the kind of knowledge that helps you pick a plan that genuinely fits your life, not just one that checks a box.

The goal here is simple: solid preparation eliminates fear. By investing a little time now to choose the right insurance, you’re really investing in your own peace of mind for the entire journey ahead.

Your Final Takeaway

The message I want to leave you with is straightforward. Living abroad is an incredible opportunity, but it comes with its own set of responsibilities. Protecting your health is number one, and a domestic U.S. plan is simply not built for that world. A specialized expat medical insurance plan isn’t a luxury—it’s an essential tool for a secure life overseas.

Now it’s time to put what you’ve learned into practice. The very next step is to see what this protection actually looks like for you. Getting a personalized quote is the easiest way to find out just how affordable and accessible real global coverage can be. It’s a simple action that delivers the ultimate payoff: the confidence to start your next chapter fully prepared for whatever comes your way.

Got Questions About Expat Insurance? We’ve Got Answers.

When you’re sorting out life in a new country, insurance questions pop up left and right. It’s totally normal. Here are some of the most common ones we hear from Americans getting ready for their big move, answered in plain English.

Can I Just Keep My ACA Plan While Living Abroad?

Technically, yes, you can keep an Affordable Care Act (ACA) plan. But should you rely on it? Absolutely not. Think of it this way: your ACA plan is built for life in the States. Its network of doctors and hospitals is almost entirely inside the U.S.

That means for day-to-day care, specialist visits, or even most emergencies in your new country, your ACA plan will be of little to no use. Plus, if you give up your permanent U.S. address, you could lose your eligibility anyway. It’s simply not a practical safety net for an expat.

What’s the Difference Between “Coverage Area” and “Network”?

Great question. These two terms get thrown around a lot, and they’re not the same thing. Getting the distinction is key to not getting hit with surprise bills.

- Coverage Area: This is the big picture—the geographic region where your plan is valid. You’ll see options like “Worldwide” or “Worldwide excluding the USA.” If you’re within that massive zone, your plan is active and can cover eligible medical costs.

- Network: This is the specific, curated list of hospitals, clinics, and doctors who have a direct-billing deal with your insurer. You can get care anywhere in your coverage area, but if you go to an “in-network” provider, the process is seamless and cashless.

If you go “out-of-network,” you’ll likely have to pay the bill yourself first and then file a claim to get your money back. Staying in-network just makes life easier.

How Do Expat Medical Plans Handle Pre-Existing Conditions?

This is where things get really different from one insurer to the next. Some plans might flat-out exclude pre-existing conditions. Others will agree to cover them, but only after a certain waiting period has passed.

The more premium plans might offer coverage right away, though you’ll see that reflected in the price. The most important thing you can do is be completely upfront about your medical history when you apply. This is where an experienced broker becomes your best friend—they know which carriers are more flexible and can help match you with a plan that actually fits your health profile.

Do I Really Need Expat Insurance in a Country with Universal Healthcare?

Yes, and we can’t stress this enough. Even if you’re moving to a country celebrated for its public healthcare system, getting a private expat plan is a smart move. For starters, you might not be eligible for the public system the day you land, leaving a dangerous gap in your coverage.

Even once you’re in the system, you’ll likely face long waits for specialist appointments or find that things like dental care and certain prescription drugs aren’t covered. A private expat plan is your fast pass to top-quality facilities and gives you a much wider choice, so you get the care you need, when you need it.

Making these decisions is the first step to building a secure, worry-free life abroad. At Expat Global Medical, our entire focus is on helping Americans find the right plan to protect their health and their savings.

Curious what a plan tailored to your life would look like? Get a free, no-pressure quote and see for yourself.