")

How To Compare Expat Medical Insurance Plans

When you lay expat medical insurance plans side by side, what really stands out are annual and lifetime limits, how extensive the provider network is, evacuation support, premium drivers, and rules around pre-existing conditions. This side-by-side view gives expats and employers a clear path to weigh premium-friendly, higher-deductible options against richer coverage with heftier price tags.

To map your priorities onto plan features, start by answering where and how you travel—whether that’s remote postings, frequent city hops, or corporate relocations.

Key Factors To Weigh

- Coverage Limits: Annual and lifetime maximum payouts.

- Network Access: Number of in-network hospitals and specialists worldwide.

- Evacuation Coverage: Emergency air and ground transport benefits.

- Deductible Options: Higher deductibles generally lead to lower premiums.

- Pre-Existing Condition Rules: Waiting periods, exclusions, and underwriting criteria.

- Pricing Drivers: Age, region of cover, and choice of billing currency.

Core Criteria Explained

These six attributes influence both your yearly premiums and how reliable your coverage is when you need it. In many cases, the evacuation benefit becomes the make-or-break difference between a mid-range plan and a premium offering.

Quick Comparison Of Top Expat Health Plans

Side-by-side view of leading expat medical insurance plans across core attributes to jump-start your decision process.

| Plan Name | Coverage Type | Deductible Range | Network Access | Evacuation Coverage | Estimated Monthly Premium |

|---|---|---|---|---|---|

| Cigna Global Gold | Full Global | $0–$2,500 | 1.5M+ providers | $500,000 air & ground | $250–$350 |

| GeoBlue Xplorer Select | Worldwide incl. US | $500–$5,000 | Major US hospitals | $250,000 | $200–$300 |

| Allianz Worldwide | Worldwide excl. US | $250–$5,000 | 1M+ providers | $500,000 | $220–$330 |

| William Russell Platinum | Worldwide | $0–$3,000 | Extensive EU & Asia | $750,000 | $280–$380 |

| Bupa Premier | Worldwide excl. US | $500–$5,000 | 900,000+ facilities | $200,000 | $230–$320 |

This snapshot helps you weed out plans that don’t match your top needs—whether that’s zero-deductible options, a broad US network, or ultra-high evacuation limits.

Scenario Trade-Offs

High evacuation limits can add roughly 15% to your premium, while choosing a lower deductible can push annual costs into the $500+ range.

Budget Considerations

Opting for “Worldwide Excluding USA” coverage often cuts premiums by 20%. Your choice of billing currency can swing monthly payments, thanks to exchange-rate fluctuations. Local tax rules may also nudge your total cost up or down.

Tip: Traveling frequently outside major cities? Investing in higher evacuation coverage can save you tens of thousands in emergency transport fees.

Next Steps After A Quick Comparison

Once you’ve narrowed your list, request personalized quotes from each provider. Verify actual network lists through a broker or carrier portal. Finally, match plan features to your mobility pattern and budget to lock in the best fit.

Understanding Expat Medical Insurance Options

When you compare a domestic health policy to what’s available for expats, the differences become clear almost immediately. Expat medical plans are built around a world that doesn’t stop at national borders. They demand careful side-by-side analysis to find the right fit.

Factors Driving Expat Coverage

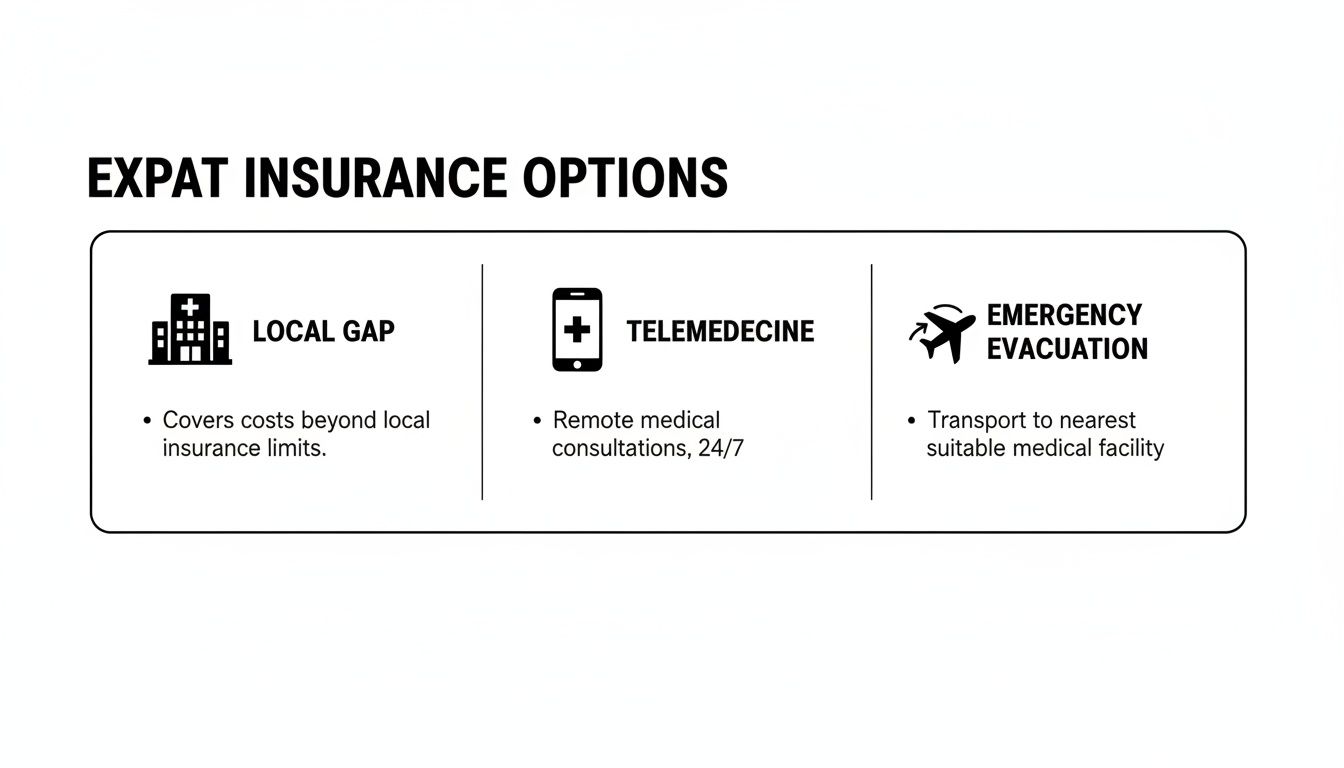

Public systems overseas may treat residents generously — but they often exclude expats or tack on steep co-pays. That leaves significant coverage gaps.

Meanwhile, many employers require group plans or evacuation riders. On top of that, telemedicine is filling a critical role for routine care when you’re miles from the nearest clinic.

Key drivers include:

- Coverage Gaps in Local Systems: Missing treatment or very high co-pays

- Employer Requirements: Mandatory group enrolment and reporting

- Telemedicine Access: Virtual consultations across borders

- Evacuation Support: Air and ground medical transport

- Regulatory Influence: Local laws reshaping plan benefits

Plans that include robust evacuation features can cost roughly 10% more. So your itinerary or work location should guide which riders you choose.

Common Plan Structures

Individual and group policies set the stage in different ways. Features like lifetime limits, co-pay tiers, and deductibles determine how much you pay out of pocket.

| Structure | Individual Policy | Group Policy |

|---|---|---|

| Enrollment | Underwriting per member | Collective risk underwriting |

| Limits | Custom annual and lifetime caps | Uniform limits across members |

| Cost Sharing | Tiered co-pay options | Standard co-pay and deductible |

Understanding these building blocks is essential for an apples-to-apples comparison.

Key Insight: Local regulations often mandate outpatient or dental add-ons, shifting costs depending on the country.

Worldwide premiums climbed to about $1.96 trillion in 2024. The United States alone accounts for 68% ($1.3 trillion) of that total, compared with China ($150.3 billion), the Netherlands ($71.9 billion), Germany ($59.8 billion), and France ($52.5 billion). Read the full research at Inube Solutions.

Those macro figures must be balanced with your personal risk profile and local requirements.

Regional Regulation Impact

Every country writes its own rules. Some insist on outpatient or maternity benefits in a base plan. Those mandates can shape both cost and access.

Others forbid portability, enforce nationality exclusions, or impose currency controls.

Key regulatory factors include:

- Required Coverage Items: Outpatient, dental, or maternity services in certain markets

- Portability Rules: Residency requirements and cross-border claim limits

- Currency Controls: Premium payments and claim reimbursements

Provider networks also vary by local accreditation and partnerships. Age, region, deductible, and optional riders are all premium drivers.

Telemedicine can offset routine care expenses — but only if the insurer has solid global platforms. These nuances set premium quotes and network access in direct tension.

A structured expat medical insurance comparison breaks down these variables. Side-by-side analysis ensures you match carriers fairly on the most critical criteria.

Criteria for apples-to-apples comparison:

- Network Size: In-network facilities and specialists worldwide

- Emergency Evacuation Limits: Financial caps and logistical support

- Pre-Existing Condition Policies: Waiting periods, exclusions, and rates

- Premium Drivers: Age, region, deductible level, and currency factors

This framework positions expats to interpret carrier details with confidence.

Comparing Leading Expat Medical Insurance Carriers

Choosing expat medical insurance isn’t just about landing the lowest premium. You have to map out coverage ceilings, emergency evacuation support, global provider networks, rules around pre-existing conditions, and how companies handle claims.

For retirees, the depth of a hospital network in Europe or Asia often outweighs minor premium savings. Digital nomads, by contrast, prioritize seamless portability and robust telemedicine options.

Below, you’ll find a structured breakdown of top carriers, focusing on nuanced trade-offs instead of one-size-fits-all pros and cons.

Read More: Hospital Bills Abroad: How Travel Medical Insurance Saves Travelers Thousands

Coverage Limits And Plan Types

Coverage limits define how much your insurer will pay before you face out-of-pocket bills. To illustrate, Cigna Global offers unlimited lifetime benefits—ideal if you anticipate major treatments or chronic care.

Allianz Worldwide caps annual payouts at $5 million, striking a middle ground between manageable premiums and financial peace of mind. William Russell lets you pick between $2.5 million and $5 million yearly limits, while GeoBlue’s Xplorer series spans $1 million up to unlimited benefits in its Premier tier.

Matching a plan to your personal health profile means balancing expected claims against budget constraints. A family might favor a mid-tier cap to control premiums while covering routine pediatric visits.

Detailed Carrier Comparison Across Key Criteria

We often find that a side-by-side view brings clarity. Here’s a snapshot of how leading carriers measure up:

| Carrier | Plan Type | Coverage Limit | Evacuation Coverage | Network Access | Deductible | Pricing Driver |

|---|---|---|---|---|---|---|

| Cigna Global | Gold, Platinum | Unlimited lifetime | $500k air & ground | 1.5M providers | $0–$2,500 | Age, region, plan tier |

| Allianz Worldwide | Diamond Care | $5M annual | $500k | 1M providers | $250–$5,000 | Deductible level |

| GeoBlue Xplorer | Essential, Select | $1M–unlimited | $250k–$500k | Major US-based | $500–$5,000 | US coverage inclusion |

| William Russell | Silver, Gold | $2.5M–$5M annual | $750k | Extensive EU & Asia | $0–$3,000 | Geographic scope |

| Bupa Premier | Select, Elite | $1.6M–$4.7M annual | 200k | 900k facilities | $500–$5,000 | Network partners |

This table unpacks where each insurer shines—whether your priority is top-tier evacuation cover or a broader global network.

Evacuation And Network Strength

When you’re off the beaten path, evacuation benefits—which range from $200k to $750k—can be the line between a manageable bill and financial ruin. Equally crucial is a broad, vetted network: Cigna and William Russell each list over 1 million in-network providers, while Bupa ties together 900,000 facilities.

Consumer priorities shift with destination. In parts of Africa or Southeast Asia, a hefty air ambulance benefit may top your checklist. In Europe, easy hospital access might trump higher evacuation limits.

Key points to weigh:

- Evacuation caps versus premium impact

- Quality ratings of main hospitals in your residence

- Pre-approval steps and 24/7 emergency hotlines

“A 600,000-mile global network is only valuable if your insurer coordinates quickly in a crisis.”

Pricing Drivers And Pre-Existing Conditions

Age, location, deductible choice, and optional riders largely dictate premium costs. On average, younger applicants see about 20% lower rates. Adding maternity cover can boost premiums by 15%.

Rules around pre-existing conditions vary dramatically. Some insurers impose waiting periods up to 24 months, while others attach exclusion riders that limit benefits. Always disclose your full medical history to sidestep claim denials.

To dive deeper into each carrier’s strengths, check out our guide on the best global health insurance providers.

Service Quality And Claims Support

The efficiency of claims processing often makes the difference between stress and smooth sailing. Focus on:

- Average turnaround times (days)

- Availability of multilingual, 24/7 support lines

- User-friendly online portals for submissions

Carrier A, for instance, resolves most claims in 3 days, whereas Carrier B may take up to 10 days—a factor that directly affects your out-of-pocket exposure.

Case Study Example

Jane, a 45-year-old expat living in Thailand, required emergency surgery. Thanks to her GeoBlue plan, an air ambulance dispatched under the $500k evacuation benefit arrived swiftly, and the insurer settled hospital costs within 5 days—keeping her personal spend minimal.

Best Practices For Choosing A Plan

- Verify live support hours across your main time zones

- Conduct a mock claim submission through each portal

- Double-check network entitlements with a local broker

- Run a scenario estimate for a significant medical event

Choosing The Right Carrier

Your final decision should mirror your health history, travel frequency, and budget goals. Start by listing your non-negotiables—be it telemedicine, low deductibles, or extensive evacuation cover.

Next steps:

- Simulate a high-cost treatment to gauge out-of-pocket risks

- Test emergency hotlines to assess response speed and clarity

- Rank insurers on a 1–5 scale for each critical criterion

- Revisit your rankings annually or after any major life change

By following this structured approach, you can zero in on the carrier that aligns with your lifestyle—whether that means maximum evacuation support or tight budget controls.

Choosing Plans Based On Expat Profiles

When you line up plan features against expat personas, the comparison stops feeling abstract and suddenly makes sense. Four core profiles help you zero in on the right coverage: Employee, Retiree, Digital Nomad, and Corporate Group.

Each profile demands a unique mix of benefits, networks, and pricing controls—so matching your situation with plan attributes becomes a straightforward exercise.

- Employee: Needs strong in- and outpatient cover, mental health support, and compliance with employer policies.

- Retiree: Prioritizes stable premiums, chronic-care riders, and minimal out-of-pocket costs.

- Digital Nomad: Wants global portability, 24/7 telemedicine, and flexible geographic modules.

- Corporate Group: Looks for centralized billing, uniform underwriting, and easy reporting.

By figuring out your expat profile, you focus only on plans designed to solve your top concerns.

Employee Profile

Employees typically require comprehensive inpatient, outpatient, and mental health cover. Employers often balance benefits and budgets with tiered deductibles and network options.

Adjusting network levels can slash premiums by about 15% without sacrificing core cover.

“A streamlined claims portal and strong local network mean your team gets care fast,” notes a global mobility specialist.

Case Study

Anna, a 34-year-old marketing manager, picked a Gold plan with $1 million inpatient cover and $500k evacuation. Her monthly premium stayed under $300, yet she has access to top city hospitals whenever she needs them.

Key Employee Decision Points

- Balance deductible tiers to suit both employer budgets and employee needs.

- Verify in-country or partner clinic networks at major work locations.

- Add maternity or mental health riders if they fit your workforce profile.

Retiree Profile

For retirees, predictability is everything. Lower deductibles and co-payments help avoid surprise bills as chronic conditions arise.

Learn more about long term retiree options in our guide on international health insurance for retirees.

- Chronic-care riders for diabetes, cardiac or oncology treatment.

- Annual and lifetime limits above $1 million for peace of mind.

- Guaranteed renewability and minimal rate-increase clauses.

- Accredited local providers in top retirement spots.

Case Study

Mark, a 70-year-old retiree in Spain, chose a plan with no deductible and a €1.5M annual limit. The guaranteed-renewal clause and robust chronic-care cover relieved his worry over sudden premium hikes.

Retiree Best Practices

- Lock in low deductibles to keep ongoing treatment costs steady.

- Look for wellness or long-term care add-ons.

- Review yearly cap adjustments to avoid unexpected expenses.

Digital Nomad Profile

Digital nomads need coverage that moves with them. Portability and solid telehealth offerings are non-negotiable.

By selecting “Worldwide Excluding Home,” travellers can cut premiums by 20%, then add or drop regions as plans change.

- Exclude your home country to save on baseline costs.

- Confirm 24/7 telemedicine features for remote consultations.

- Pick a mid-range deductible to balance premiums and out-of-pocket limits.

Case Study

Leo, 29, toggled coverage among Southeast Asia, Europe, and South America modules. Excluding his home country and adjusting regions quarterly trimmed his annual premium by 25%.

“You need plans that let you swap regions quickly—without fresh underwriting,” advises a global mobility advisor.

Corporate Group Profile

When you insure an entire team, simplicity and predictability top the list. Centralized billing and standardized tiers make life easier for finance and HR alike.

| Feature | Group Plan | Individual Plan |

|---|---|---|

| Underwriting | Collective risk basis | Individual health checks |

| Deductible Structure | Flat per member | Flexible per policy |

| Billing | Centralized invoices | Direct to insured |

| Reporting | Standardized reports | Custom statements |

Case Study

TechCorp covered 120 remote employees across five continents under a flat $1,000 deductible group plan. Centralized invoicing and uniform benefits simplified budgeting and ensured everyone got the same level of care.

Corporate Group Tips

- Automate enrollment and renewals to cut administrative time.

- Align benefit tiers with team diversity and regional cost differences.

- Negotiate block discounts for larger headcounts or multi-year deals.

- Audit network adequacy and compliance annually.

Real-world tweaks—like raising deductibles from $500 to $1,500—can reduce premiums by about 12%. By aligning your expat profile with the right plan attributes, you cut through the noise and focus on solutions that really matter.

Next up: compare cost scenarios and request personalized quotes from a trusted broker to lock in your ideal coverage.

Real World Expat Cost And Scenario Comparisons

Crunching real-world numbers shows how age, region, plan tier and deductible all play into your final premium. We’ve laid out three distinct profiles—a 30-year-old in Bangkok, a retiring couple in Spain, and a globe-trotting nomad—to bring the figures to life.

Scenario One: Young Expat In Southeast Asia

At 30, our Bangkok-based consultant opts for a Gold plan with a $500 deductible. Her monthly premium settles at $120, thanks to Thailand’s lower medical fees and a $200k evacuation cap.

Key trade-offs:

- Regional rates in Thailand hover 40% below global averages.

- Mid-tier plans strike a balance between inpatient cover and affordability.

- A moderate deductible makes routine doctor visits more predictable.

In practice, a $50 outpatient visit costs her just $15 out-of-pocket after meeting the deductible. Choosing “Worldwide Excluding USA” coverage trims premiums without skimping on essentials.

Scenario Two: Retiring Couple In Europe

This couple, aged 65 and 62, relocates to Spain and picks a Platinum plan with a €0 deductible. Their euro-denominated premiums run €600 per person each month, reflecting senior rates and continent-wide billing.

They enjoy $1M annual limits, chronic care riders, 24/7 telemedicine and €500 evacuation cover.

“Locking in a no-deductible option can eliminate surprise bills for ongoing treatments,” says a retirement health specialist.

| Feature | Cost Per Person | Deductible | Annual Limit |

|---|---|---|---|

| Monthly Premium | €600 | €0 | €1,000,000 |

| Chronic Care Riders | Included | N/A | Unlimited |

| Telemedicine Availability | 24/7 | N/A | N/A |

| Evacuation Cover | Included (€500) | N/A | N/A |

Their experience highlights how age brackets, currency choice and extra evacuation benefits lift premiums.

Scenario Three: Digital Nomad Traveling Latin America And Africa

Our 28-year-old nomad splits time between Peru, Brazil, Kenya and South Africa. He selects an Essential plan with a $1,000 deductible and $500k evacuation cover.

By rotating region modules each quarter, his annual cost stays at $800. He taps into telemedicine consultations at $30 a pop to handle minor ailments remotely.

Tactics for cost efficiency:

- Exclude the home country to reduce baseline premiums by 20%.

- Swap region modules quarterly to mirror travel patterns.

- Balance deductible size against potential out-of-pocket exposure.

This flexible setup aligns coverage to his ever-changing itinerary.

Comparative Cost Drivers And Trade-Offs

Across these examples, three main drivers emerge:

- Age can boost premiums by up to 30% between young adults and retirees.

- Currency selection may swing costs by around 15% due to exchange-rate shifts.

- Raising the deductible by $500 typically cuts premiums by about 12%.

| Driver | Impact On Premium |

|---|---|

| Age | +30% for retirees |

| Currency | ±15% |

| Deductible | -12% per $500 rise |

Additional best practices:

- Review billing-currency options before you enroll.

- Test emergency hotlines to gauge insurer responsiveness.

- Model high-cost treatment scenarios to estimate your max out-of-pocket.

In 2024, North America holds a 62.15% market share, driven by U.S. spending projected at $660.08B in 2025 and rising to $1,264.33B by 2034 at a 7.51% CAGR. Per-capita spending tops $12,000, versus a global average under $2,500. Learn more at Fortune Business Insights.

Check out our guide on expat health insurance costs at Expat Health Insurance Cost Guide.

These concrete examples should help you forecast expenses, weigh trade-offs and pinpoint the coverage that fits your age, regions and deductible preferences. Request quotes tailored to your profile and travel habits, ensuring you get the most value from your expat medical insurance.

Creating An Expat Buyer Checklist And Next Steps

When you’ve narrowed down your top expat medical insurance plans, it’s time to move from research to action. This buyer checklist lays out every essential task—from zeroing in on must-have benefits to locking in coverage well before your departure date.

Buyer Checklist Essentials

- Plan Criteria — Pin down coverage limits, network depth, evacuation benefits, and rules around pre-existing conditions so you know exactly what you’re getting.

- Documentation Pack — Round up passport scans, medical history summaries, proof of residency, and your claim-record templates (see Sample Docs).

- Broker Consultation — Book a sit-down with an industry expert to vet quotes, unpack policy language, and negotiate any available discounts.

- Quote Requests — Secure 3 personalized quotes to compare how age, region, and deductible choices drive your premium.

- Network Vetting — Verify in-network hospitals and telehealth options using carrier portals or your broker’s spreadsheet.

- Service Responsiveness — Test emergency hotlines and submit a mock claim online to gauge typical turnaround times.

- Enrollment Timing — Aim to finalize your plan at least 60 days before travel or move-in to lock in rates and avoid any coverage gaps.

This concise list turns your side-by-side analysis into a clear roadmap you can follow without second-guessing.

Implementing Next Steps

First, stash all your documents in one shared folder and grant access to your broker. Next, lay out the 3 quotes in a simple comparison template to spotlight cost drivers and coverage discrepancies.

Use this table to track each carrier’s responsiveness and network reach at a glance:

| Template Type | Resource |

|---|---|

| Documentation Checklist | Sample Docs |

| Quote Comparison Template | Quote Tracker |

| Broker Questions List | Advisor Guide |

| Network Vetting Sheet | Network List |

Pro Tip Use this checklist alongside our cost scenario module to fine-tune your ideal coverage mix.

Finally, submit your quote requests via our online portal. Track who responds fastest and lock in your preferred plan before the deadline.

Final Verification

Double-check every policy’s fine print for exclusions, co-pay percentages, and renewal terms. Make sure your 24/7 support details are clear, and note any blackout periods or claim-submission cutoffs.

Then, head over to expat forums or review sites for peer feedback. Real-world experiences often reveal service quirks you won’t find in a brochure.

- Download the Buyer Checklist PDF and complete your preferences.

- Email your broker the full documentation pack and arrange a review call.

- Use the comparison table to rank quotes and zero in on your top provider.

- Submit your enrollment form and initial premium payment to lock in your rate.

- Store both digital and paper copies of all policy documents in a secure place.

Follow these steps to move confidently from analysis to dependable coverage. Ready to wrap up your plan? Let’s get you protected.

Frequently Asked Questions About Expat Medical Insurance

When you’re sizing up expat medical insurance, certain questions keep coming back: How solid is the provider network? What happens if you need an emergency evacuation? Can you switch plans mid-term? And how does underwriting actually work?

Take hospital coverage, for instance. Verifying your insurer’s online directory is a good start—but always call the hospital directly to confirm they still participate. That little extra step can save you from unexpected out-of-pocket bills.

If you find yourself in a remote region, most global plans include pre-approved air or ground transport. The moment you realize you need evacuation, dial your insurer’s emergency assistance line. They’ll coordinate everything so you don’t get stuck with the bill.

- Switching Plans Mid Term: Changing insurers before your renewal date usually means fresh underwriting and potentially new waiting periods. Talk through these timing issues with a broker to avoid coverage gaps.

- Pre-Existing Condition Rules: Underwriting hinges on your medical history. Insurers may impose waiting periods or carve out specific conditions, so full disclosure at application ensures you get accurate quotes and smoother claims.

“Always review network lists and emergency protocols before you buy.”

— Expat Global Medical Advisor

Decision Making Tips

To sharpen your comparisons, zero in on the factors that matter most:

- Start With Network Strength: Are top hospitals and specialists in-network?

- Check Evacuation Caps: Know your coverage limits for air or ground transport.

- Understand Underwriting Impact: Spot any waiting periods or exclusions.

Next, map each Q&A against your shortlisted plans in a side-by-side table. This quick visual will highlight where trade-offs live and help you decide fast.

Quick Reminders

Keep this FAQ within easy reach as you compare quotes:

- Confirm provider directories are current and searchable.

- Note evacuation caps and average response times in remote areas.

- Review mid-term change provisions to see if waiting periods apply.

Treat this section as your living reference—and revisit it whenever you need clarity on policy details.

Ready to find your ideal plan? Reach out to Expat Global Medical for personalized advice and quotes.