")

So, you’re planning that dream retirement abroad? What an exciting chapter. You’ve likely spent countless hours picking the perfect spot, figuring out the lifestyle, and sorting through finances. But there’s one piece of the puzzle that, if overlooked, could bring the whole thing crashing down: your health coverage.

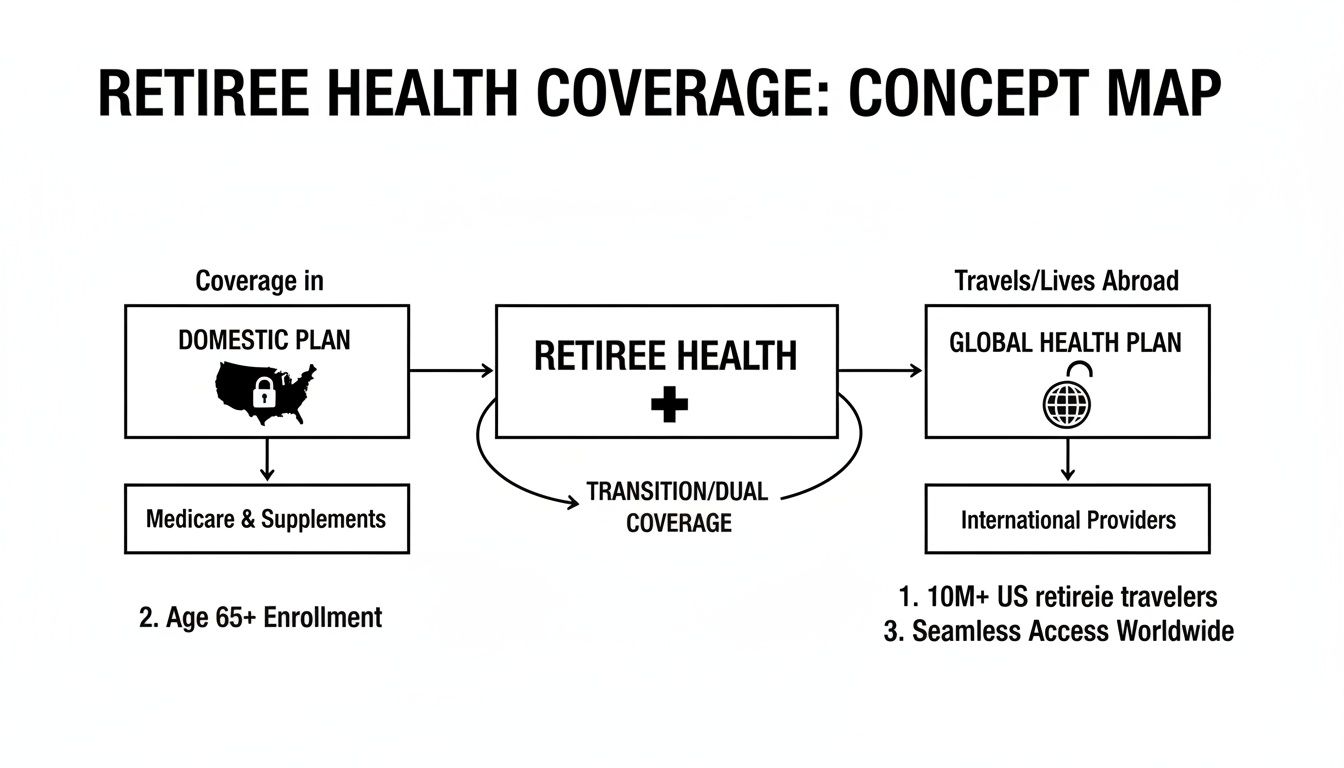

Many retirees make the dangerous assumption that their trusty health plan from back home, like Medicare, will simply pack its bags and come along for the ride. That’s a huge misconception. Your domestic insurance is designed for one country and one healthcare system only.

Think of it this way: your local library card is a golden ticket in your hometown, opening up a world of resources. Take it to another country, though, and it’s just a useless piece of plastic. You need a global access pass. Expat medical insurance for retirees is that pass, built from the ground up for expats living long-term outside their home country. It’s your connection to a worldwide network of doctors and hospitals, safeguarding both your health and your retirement savings.

Why Your Home Country’s Insurance Just Won’t Cut It

Let’s be blunt: most domestic health plans, especially government-run programs like Medicare in the U.S., offer virtually zero coverage once you move abroad. Relying on them is a recipe for disaster, leaving you exposed to massive out-of-pocket bills and serious gaps in care right when you need it most.

A proper expat medical plan isn’t a nice-to-have add-on; it’s a fundamental replacement for your old insurance. These policies are specifically designed with a retiree’s unique needs in mind, packing in features you’ll rarely find in short-term travel insurance or any domestic plan.

It’s a classic mistake to confuse short-term travel insurance with a real expat health plan. Travel insurance is for covering emergencies on a two-week vacation. An expat medical insurance plan is for your actual life—handling everything from a routine check-up to critical care as a resident of a new country.

What to Look for in a Real Expat Medical Plan

A solid expat medical plan should be a comprehensive safety net, ready for any possibility. Every retiree should make sure their policy includes these core components:

- Comprehensive Hospital Stays: This covers your inpatient care, surgeries, and major treatments, usually in high-quality private hospitals where you won’t face long public system waits.

- Emergency Medical Evacuation: This is non-negotiable. If you have a serious medical event and the local facilities can’t provide the care you need, this feature covers the cost of transporting you to the nearest capable hospital. That flight alone can cost tens of thousands of dollars.

- Access to Specialist Care: You need the freedom to see specialists for new health issues or to manage ongoing conditions without being stuck on a waiting list for months.

- Prescription Drug Coverage: This ensures the medications you rely on are covered and accessible in your new home base.

On a practical note, managing your finances smoothly from another country is also key. Getting a handle on things like how to open a US bank account as a non-resident can make paying for your insurance and other expenses much simpler.

How Expat Medical Insurance Really Works

To really wrap your head around expat medical insurance, it helps to stop thinking of it as an add-on. It’s not a supplement; it’s a full-blown replacement for the health plan you’ve relied on back home.

Think of it this way: your domestic insurance plan is like a key that only opens your front door. An expat medical plan, on the other hand, is the master key—it’s designed from the ground up to work in hospitals and clinics all around the world.

This kind of insurance is built for the long haul of living abroad, completely different from a short-term travel policy you’d buy for a two-week vacation. It provides solid, ongoing coverage for both unexpected emergencies and regular, everyday care, making sure you’re protected no matter where your retirement adventure leads.

The Critical Gaps Your Home-Country Coverage Leaves Behind

Many American retirees get a nasty surprise when they discover their trusted Medicare plan becomes virtually useless the moment they move overseas. It’s a hard truth, but with very few and specific exceptions, Medicare Parts A, B, and D do not cover healthcare services you receive outside the United States.

This isn’t a small gap; it’s a massive, dangerous hole in your financial safety net. A simple check-up or, worse, a serious hospital stay would be a 100% out-of-pocket expense. We’re talking about costs that could easily run into thousands, if not hundreds of thousands, of dollars.

Even the Medigap plans people buy to fill Medicare’s gaps offer flimsy protection abroad. While some policies might include a foreign travel emergency benefit, it usually comes with a lifetime cap of just $50,000 and a steep deductible. That’s barely enough to handle one serious incident, let alone a true medical crisis.

To put this all into perspective, take a look at the key differences between your options.

Comparing Healthcare Options for Expat Retirees

This table breaks down how each type of insurance stacks up when you’re living outside your home country. It clearly shows why relying on domestic plans is a risky bet for any long-term expat.

| Coverage Feature | Medicare | Domestic Private Insurance | Expat Medical Insurance |

|---|---|---|---|

| Global Coverage | No, except in rare, specific cases | Very limited, usually emergency-only | Yes, designed for global or regional coverage |

| Routine & Preventive Care Abroad | Not covered | Not typically covered | Yes, a core feature of most plans |

| Prescription Drugs Abroad | Part D does not apply | Not covered | Yes, often an included or optional benefit |

| Medical Evacuation | Not covered | Not covered | Yes, a standard and critical feature |

| Choice of Doctors/Hospitals | N/A abroad | N/A abroad | Access to a global network of providers |

| Direct Billing | N/A abroad | N/A abroad | Yes, with in-network providers |

As you can see, only a dedicated expat health plan is built to handle the realities of retiree life abroad, offering the comprehensive, flexible coverage you actually need.

This visual really drives the point home: your healthcare strategy has to shift from a local mindset to a global one to match your new lifestyle as an expatriate.

How Insurers Decide: Understanding the Underwriting Process

Because expat medical plans provide such wide-ranging protection, the insurance company needs to get a clear picture of the risk they’re taking on. This is where underwriting comes into play.

Simply put, underwriting is the process an insurer uses to review your application and medical history. Their goal is to figure out if they can offer you a policy and what the premium should be.

Unlike Medicare, which essentially has to accept you, international health insurers require you to fill out a detailed health questionnaire. They’ll ask about your past and present health conditions, any medications you take, and general lifestyle habits.

Honesty is absolutely crucial here. Failing to disclose a pre-existing condition, even one that seems minor to you, could give the insurer grounds to cancel your policy or deny a claim right when you need the coverage most.

Based on your answers, the underwriters assess your health profile. This step is foundational because it determines how your pre-existing conditions will be handled—a vital topic for any expat retiree. Ultimately, the insurer’s goal is to create a sustainable plan that works for both of you, ensuring you have reliable protection for the long term.

Navigating Costs and Pre-Existing Conditions

Alright, let’s get down to brass tacks. We’ve arrived at the two questions every retiree asks: “How much is this actually going to cost me?” and “Will they cover my existing health issues?” These aren’t just minor details; they’re the heart of the matter for any expat.

The price of expat medical insurance for retirees isn’t a simple, off-the-shelf figure. Think of it more like customizing a new car—the final sticker price really depends on the engine you choose, the features you add, and where you plan to drive it.

Several key factors directly shape your monthly premium. Getting a handle on them is the first step to finding a plan that protects your health without derailing your retirement budget.

Decoding the Cost of Your Policy

The premium an insurer quotes you is a carefully calculated number. It’s not pulled out of thin air. Instead, it’s based on a handful of personal details and the specific plan benefits you select.

Here are the biggest drivers of your insurance costs:

- Your Age: This is the most straightforward factor. As we get older, the statistical likelihood of needing medical care goes up, and premiums reflect that.

- Coverage Level: Plans are often tiered. You can get a basic plan that only covers hospital stays or a comprehensive one that includes regular doctor visits, dental, and vision. The more you include, the higher the cost.

- Deductible and Coinsurance: A classic trade-off. If you’re willing to pay more out-of-pocket before the insurance kicks in (a higher deductible), you can significantly lower your monthly premium.

- Geographical Coverage Area: This one is huge. Where you need coverage can have a massive impact on your price—in fact, it’s often the single most powerful tool for managing your costs.

One of the smartest ways to lower your premium is by choosing a coverage area that excludes the United States. Healthcare in the U.S. is notoriously expensive, often costing two to three times more than in other developed countries.

By opting for a “worldwide excluding USA” plan, expat retirees can often cut their premiums by a staggering 30% to 50%. This is a game-changer if you don’t plan on spending much time or seeking medical care back in the States.

For a deeper dive into how these variables play out, check out our full guide on expat health insurance cost. It has calculators and examples that show you exactly how different choices affect the bottom line.

Addressing Pre-Existing Conditions Head-On

For many expat retirees, the real elephant in the room is how an insurer will view their medical history. A pre-existing condition is any health issue you had before applying for coverage—anything from high blood pressure to a past surgery.

It’s helpful to understand the context around common issues, like managing blood pressure, when you approach this topic. Unlike the group plans you might be used to back home, expat medical plans don’t automatically have to cover these conditions. They use a process called medical underwriting, where they review your health history to decide the terms of your policy.

During underwriting, an expert reviews your application and medical records. From there, the insurance company will come back with a decision, which almost always falls into one of four buckets.

The Four Potential Underwriting Outcomes

It’s really important to go into the application process with clear eyes. When you disclose a pre-existing condition, the insurer will typically respond in one of these ways:

- Full Coverage (Accepted as Standard): This is the best-case scenario. If your condition is minor, well-managed, and seen as low-risk, the insurer might offer you a standard policy with full coverage at no extra charge.

- Coverage with a Premium Surcharge: For more significant or chronic conditions, the insurer might approve your policy but add a surcharge—an extra percentage on top of your premium—to account for the higher risk.

- Coverage with an Exclusion Rider: Sometimes, the insurer will offer you a policy but attach an exclusion rider. This means the plan will cover you for everything except for treatments related to that one specific pre-existing condition.

- Application Denial: In rare cases where a condition is considered too high-risk, unmanaged, or complex, the insurer may decline to offer coverage altogether. While this is the outcome nobody wants, it is also the least common.

The key to navigating this is total honesty. You have to disclose everything on your application. Hiding a condition is a sure-fire way to have your claims denied or your entire policy canceled later on. By understanding these potential outcomes, you can approach the process with confidence and find the best possible protection for your new life abroad.

Must-Have Features in Your Expat Health Plan

A quality expat medical plan is so much more than a safety net for a big surgery. Think of it as a complete support system for your health and well-being while living abroad, built to handle everything from routine check-ups to life-or-death emergencies. Knowing which features are absolutely non-negotiable is the key to picking a plan that genuinely has your back.

When you’re looking over a policy, it’s a bit like inspecting a new house. You wouldn’t just make sure the roof is solid; you’d also check the plumbing, the wiring, and the foundation. In the same way, a strong expat health plan is built on several core components that need to be robust and reliable.

The Lifesaving Duo: Evacuation and Repatriation

Picture this: you’ve retired to a tranquil coastal village in Southeast Asia. The local clinic is perfectly fine for minor scrapes, but after a serious fall, you find out you need complex orthopedic surgery they simply can’t perform. This is the exact moment when medical evacuation becomes the most critical benefit you could possibly have.

- Medical Evacuation: This feature pays to transport you from where you are to the nearest medical center that can give you the advanced care you need. That could mean a flight to a major city in the next country over or even all the way back home. Without insurance, these transport costs can easily soar past $100,000.

- Repatriation of Remains: Nobody wants to think about it, but this coverage is vital. It handles the enormous logistical and financial weight of returning a person’s remains to their home country if they pass away abroad.

Without this coverage, you’re stuck with an impossible choice: settle for inadequate local care or face a financially crippling transportation bill. Given the stakes, this is arguably the single most important feature of any expat medical plan. For a deeper dive, you can learn more about what is medical evacuation insurance in our detailed guide.

A common mistake is thinking travel insurance evacuation coverage will suffice for long-term living. It won’t. Expat plans are built for residents, not tourists, offering much higher limits and ensuring you’re covered for serious medical events that require extensive care and transport.

Access to Quality Care: Provider Networks

A fantastic insurance plan doesn’t mean much if you can’t find a good doctor or hospital that will actually accept it. That’s why a broad and dependable provider network is so important. These are the hospitals, clinics, and specialists that have a direct billing relationship with your insurer.

Using an in-network provider makes everything smoother. The hospital typically bills the insurance company directly, saving you from having to pay huge sums out-of-pocket and then chase down a reimbursement.

Direct Billing vs. Reimbursement Explained:

- Direct Billing (Cashless Service): This is the goal. You go to an in-network hospital, show your insurance card, and only pay your deductible or copay. The insurer handles the rest directly with the hospital.

- Reimbursement: You pay the entire medical bill yourself upfront. Then you have to submit a claim with all the receipts to your insurer, who reviews it and eventually sends you a check or bank transfer.

While reimbursement is always an option, having a strong network that enables direct billing dramatically cuts down on the financial stress during an already stressful medical situation.

Core Benefits for Everyday Health

Beyond emergencies, your plan needs to support your day-to-day health. These features are what allow you to manage your health proactively and affordably, helping you maintain a great quality of life in your new home.

Make sure any comprehensive plan you consider includes these essentials:

- Prescription Drug Coverage: This covers the cost of medications, whether for managing a chronic condition or for a short-term illness.

- Specialist Access: Good plans ensure you can see specialists—like a cardiologist, endocrinologist, or dermatologist—without needing a referral from a general doctor. This saves time and gets you to the right expert faster.

- Wellness and Preventive Care: Many top-tier plans now include benefits for routine physicals, cancer screenings, and other preventive services. This helps you stay on top of your health and catch potential problems early.

These benefits are what turn a policy from a simple emergency backup into a true health partner, giving you the tools to live a long, healthy, and secure life as an expat.

Healthcare Realities in Popular Retirement Havens

Picking your perfect retirement spot is about so much more than sunshine and fantastic food. You have to get real about the day-to-day practicalities, and nothing is more practical than healthcare. How a country’s healthcare system works—its quality, how you get in, and what it costs—will directly shape your quality of life and your financial peace of mind.

Let’s move past the theory and look at how expat medical insurance for retirees actually plays out on the ground in a few of the world’s top expat destinations. Every country has its own unique mix of public and private healthcare, not to mention specific insurance rules you’ll need to follow for your residency visa.

Portugal: A Top Choice for a Reason

Portugal has exploded in popularity among expat retirees, and it’s easy to see why. The blend of safety, affordability, and a top-notch healthcare system is hard to beat. But to make it work, you need to plan ahead.

Portugal’s public healthcare system, the Serviço Nacional de Saúde (SNS), is fantastic, but it’s also known for long wait times for specialist appointments and non-emergency procedures. This is exactly why the overwhelming majority of expats secure private health insurance. A solid private plan is your fast-pass to a network of modern, private hospitals and English-speaking doctors, letting you jump the public queue when you need to.

More importantly, for your initial residency visa (like the D7 or D8), showing proof of comprehensive health insurance isn’t optional—it’s a mandatory part of the application.

A recent analysis in the Global Retirement Report 2025 crowned Portugal the number one destination for international retirees, stacking it up against 43 other nations. Its world-class healthcare, a straightforward visa process that requires proof of passive income around €820 monthly, and living costs that are 40-50% lower than in the US or UK are huge factors. You can find more details in the full global retirement report.

Spain: Sun, Lifestyle, and Specific Insurance Rules

Spain is another long-standing favorite, famous for its incredible culture and quality of life. Just like Portugal, it has a highly-rated public healthcare system, but getting access as a new retiree isn’t a given from day one.

To get your initial non-lucrative visa, the Spanish government has a very strict requirement: you must have a private Spanish health insurance plan. This plan has to come with zero copayments and no deductibles, and it must offer coverage that’s on par with the public system. An international plan, no matter how good, usually won’t cut it for this specific visa step.

What many expats do is buy the required Spanish plan for their first year to satisfy the visa rules. Once their residency is established, they often switch to a more flexible expat medical insurance for retirees plan. A global plan gives you much broader coverage, which is perfect if you plan on traveling around Europe or flying back home to visit family.

Mauritius: Tropical Living with Modern Medicine

If your retirement dreams lean more towards a tropical paradise, Mauritius delivers with a surprisingly sophisticated healthcare system. The island has a strong dual system with both public and private options, and it’s even becoming a destination for medical tourism.

The public hospitals offer free services to all residents, but they can get crowded. On the flip side, the private clinics are modern, offer an incredibly high standard of care, and have no wait times. To secure your retirement visa, you’ll have to show proof of health insurance from a provider that’s recognized in Mauritius.

Because of its remote location, having robust medical evacuation coverage is an absolute must for any expat retiree here. While local private care is excellent for most things, a major medical crisis might require a flight to South Africa or Europe for specialized treatment. This feature isn’t just a nice-to-have; it’s a critical part of your insurance plan. If you’re curious about other great spots, check out our guide on the top 7 countries to retire abroad.

Retiree Healthcare Snapshot: Top Destinations

Understanding these country-specific details is crucial. A plan that works perfectly for a visa in Portugal will get you rejected in Spain. This table breaks down the key differences at a glance to help you compare.

| Country | Public Healthcare Access | Private Insurance Recommendation | Avg. Monthly Premium (Couple) |

|---|---|---|---|

| Portugal | Yes, after residency registration. | Required for visa. Chosen to bypass public system wait times. | €300 – €500 |

| Spain | Usually after 1 year of residency. | Required for visa (specific Spanish plan with no copays). | €250 – €450 |

| Mauritius | Yes, for all residents. | Required for visa. Essential for private clinic access & evacuation. | €400 – €600 |

Ultimately, picking the right expat medical insurance for your new home isn’t just about checking a box for a visa application. It’s about making a strategic investment in your own health, making sure you can get the best care, fast, no matter where in the world you decide to live.

Your Checklist for Choosing the Right Plan

Alright, let’s turn all this information into a smart decision. Picking the right expat medical insurance for retirees can feel overwhelming, but breaking it down with a simple checklist makes it much more manageable.

Think of this as your personal scorecard for every plan you look at. By running each potential policy through these four key areas, you’ll be able to confidently pick a plan that truly has your back during your retirement abroad.

Coverage Essentials

These are the absolute must-haves—the foundation of any plan worth its salt. Cutting corners here is a recipe for financial disaster.

- Medical Evacuation: Does the plan cover getting you to the nearest top-notch medical facility? A medical flight can easily top $100,000, so this benefit is what stands between you and financial ruin if you need critical care far from home.

- High Lifetime Maximum: Is the total coverage limit at least $1,000,000 USD? This high ceiling protects you from a catastrophic medical event that could otherwise wipe out your entire retirement nest egg.

Cost and Financials

You need to get a firm grip on the numbers. Understanding how a plan is structured financially helps you manage both your monthly budget and your potential out-of-pocket risks.

Your deductible is simply the amount you agree to pay out-of-pocket before your insurance kicks in. Many retirees choose a higher deductible to lower their monthly premium, but just make sure it’s an amount you could comfortably pay if a medical issue arises.

- Deductible Options: Does the plan give you the flexibility to choose a deductible that fits your financial comfort zone?

- Coverage Area: Can you lower your premium by excluding expensive regions you don’t plan to visit, like the USA?

Provider Access and Service

Fantastic coverage on paper means nothing if you can’t actually use it when you need it most. Look for features that make the whole process smooth and stress-free, especially during an emergency.

- Direct Billing Network: Does the insurer have a solid network of hospitals in your new country that will bill them directly? This is a huge deal—it means you won’t have to pay massive hospital bills upfront and wait weeks for reimbursement.

- 24/7 Assistance: Is there multilingual emergency support available any time, day or night? A medical crisis doesn’t stick to a 9-to-5 schedule, and getting immediate help from a real person is absolutely critical.

Your Top Questions About Expat Health Insurance, Answered

When you’re planning a retirement abroad, navigating the world of expat medical insurance can feel a bit like learning a new language. A few key questions always pop up, and getting clear, straightforward answers is the first step toward making a smart decision for your health and future.

Let’s cut through the noise and tackle the most common queries we hear from expat retirees just like you.

Can I Just Keep My Medicare Plan if I Move Abroad?

Yes, you can absolutely keep your Medicare plan active while you live overseas, but here’s the critical part: it’s almost completely useless for healthcare outside the United States. With only a handful of very specific, rare exceptions, Medicare will not pay for medical care you receive in another country.

That means your day-to-day doctor visits, prescription refills, or even a serious hospital stay in your new home country won’t be covered. Many retirees keep their Part B to avoid late-enrollment penalties if they ever return to the U.S., which is a fine strategy. But you should never, ever think of it as your primary health coverage while living abroad.

Relying on Medicare overseas is like bringing a house key to unlock a car—it’s simply the wrong tool for the job. You need a dedicated expat medical insurance plan built for a global life.

At What Age Does Getting Coverage Become Difficult?

This is a big one, and it’s smart to think about it early. Your age is definitely a major factor when you’re applying for a new expat health insurance policy. While plenty of providers are happy to offer plans to seniors, your options do start to shrink the older you get.

Most insurers draw a line in the sand with a maximum enrollment age, which usually lands somewhere around 74 or 75 years old. Once you’re past that age, finding a new, comprehensive plan becomes significantly harder—and sometimes, it’s just not possible.

This is exactly why it pays to be proactive. Securing a plan in your late 60s or early 70s opens up a much wider menu of choices. More importantly, it locks in a policy that’s renewable for life, giving you a safety net that will protect you well into your later retirement years.

Does My Plan Cover Visits Back Home?

It’s an excellent question, especially since most expat retirees plan on visiting family and friends back in their home country. The short answer is: it depends entirely on your specific policy and the coverage area you choose.

Many of the best expat medical insurance plans for retirees include an option for home country coverage. This benefit is designed for short-term visits, typically covering you for a limited period—say, 30 to 90 days per year—while you’re back home. It’s perfect for handling an unexpected illness or injury that pops up during a trip, but it’s not meant for long-term stays or planned, elective procedures. Always dig into the policy details to see exactly how long this coverage lasts and if there are any limitations.

Ready to secure your health and peace of mind for the retirement adventure you deserve? At Expat Global Medical, we specialize in helping expat retirees find the right medical coverage for their unique plans.

Get Your Free International Health Insurance Quote Today and see how simple it is to protect your new global lifestyle.