")

So, you’re moving abroad. It’s an incredible adventure, but let’s be honest—figuring out healthcare can feel like trying to solve a puzzle in a foreign language. This is where expat medical insurance comes in. Think of it as your long-term, comprehensive medical plan for living in another country, and it’s worlds apart from the basic travel insurance you’d buy for a one-week vacation. It’s designed to be your primary health plan, covering everything from regular check-ups to serious medical emergencies while you’re living overseas.

Understanding Your Global Health Insurance Options

Starting a life in a new country is a massive step, and securing the right healthcare is fundamental to your peace of mind. Many people mistakenly believe a standard travel policy is sufficient, but this assumption can lead to huge coverage gaps and jaw-dropping medical bills. The distinction isn’t just a technicality—it’s about choosing a plan built for your specific needs.

Here’s a simple way to think about it: travel insurance is a first-aid kit for a vacation. It’s built for short-term mishaps—a broken leg on a ski trip, a sudden stomach bug, or a lost passport. Its main job is to patch you up and, in most serious cases, get you back home for proper treatment.

On the other hand, expat medical insurance is your personal doctor, specialist, and hospital network abroad. It’s designed for your life as a resident, providing comprehensive coverage for the day-to-day. This means it covers not just emergencies but also routine doctor’s visits, preventative care, and managing any long-term health issues you might have.

To make this crystal clear, here’s a quick breakdown of how these two types of plans stack up against each other.

Travel Insurance vs Expat Health Insurance at a Glance

| Feature | Short-Term Travel Insurance | Long-Term Expat Health Insurance |

|---|---|---|

| Primary Purpose | Covers emergencies on short trips (e.g., trip cancellation, lost luggage, urgent medical care). | Provides comprehensive, long-term health coverage for people living abroad. |

| Duration | Limited to the length of your trip, usually from a few days to a few months. | Annual, renewable plans designed for stays of 6 months or longer. |

| Medical Coverage | Emergency medical and dental only. Stabilizes you for return home. | Full coverage: inpatient, outpatient, preventative care, check-ups, chronic conditions. |

| Routine Care | Almost never covered. No coverage for regular doctor visits or physicals. | A core benefit. Covers check-ups, screenings, and managing ongoing health. |

| Pre-existing Conditions | Typically excluded or only covered for acute, unexpected flare-ups. | Often covered after medical underwriting, designed for long-term management. |

| Choice of Doctor | Limited to emergency facilities, often with a “pay first, claim later” model. | Freedom to choose from a global network of doctors and hospitals, often with direct billing. |

| Best For | Tourists, vacationers, and short-term business travelers. | Expats, digital nomads, international students, and retirees living abroad. |

As you can see, relying on a travel plan for long-term living is like using a band-aid for a broken bone—it just won’t do the job.

The Growing Need for Real Coverage

The demand for robust international medical insurance isn’t just a niche concern anymore; it’s a direct reflection of our globally mobile world. With more people living and working abroad, rising medical costs, and many countries tightening visa rules, having proof of proper health coverage is often a requirement, not a suggestion.

The global travel insurance market is projected to skyrocket, with some estimates predicting it will reach nearly USD 63.87 billion by 2030. This surge shows a massive global awakening to the financial risks of being caught without the right medical protection abroad.

This huge market growth tells a simple story: having a plan designed for your situation is non-negotiable. A basic travel policy just isn’t built to handle the real healthcare needs of someone who is actually living in a new country. You can explore more about the travel insurance market trends and see for yourself why robust, long-term plans are becoming essential.

Why Expat Medical Insurance Is the Smart Choice for Long-Term Stays

Choosing the right international health insurance is one of the most critical decisions you’ll make before you move. An expat plan gives you access to quality healthcare without the fear of facing crippling out-of-pocket bills. It provides the security you need to actually build your new life with confidence, knowing you’re protected.

This guide is laser-focused on expat medical insurance because, frankly, it’s the only sustainable solution for anyone living abroad long-term. We’ll break down exactly what these plans cover, how they truly differ from travel policies, and how you can choose the best one for your own unique adventure.

Travel Insurance vs. Expat Health Insurance: A Detailed Comparison

While the last section gave a quick overview, getting the right insurance really comes down to understanding the philosophy behind each type. They might sound similar, but they are built for fundamentally different jobs.

One is for visiting a place. The other is for living there.

Think of travel insurance as an emergency response team. Its entire job is to deal with sudden, unexpected things that throw a wrench in your trip—a canceled flight, lost bags, or a medical crisis that needs immediate attention. When it comes to healthcare, its goal is simple: patch you up, get you stable, and if necessary, get you back home.

On the other hand, expat medical insurance is your primary healthcare system in a new country. It’s designed for the long haul, covering your health from top to bottom. This isn’t just about emergencies; it’s about your actual life abroad. We’re talking routine check-ups, preventative care, specialist visits, and managing any ongoing health conditions.

The Philosophy of “Visiting” vs. “Living”

Travel insurance is temporary, emergency-first coverage. It’s built to answer one question: “What do we do if something goes wrong on this trip?” It’s reactive. It jumps into action when a problem hits to handle the immediate fallout.

Expat medical insurance is proactive and comprehensive. It’s designed to answer a much bigger question: “How will I manage my health while building a life here?” It works from the assumption that you’ll need more than just an ambulance, because real life involves regular doctor visits, health screenings, and ongoing medical needs.

The core distinction is simple yet profound. A travel policy is designed to get you well enough to travel back home for continued care. An expat plan is designed to provide that continued care in your new home country, treating it as your primary place of residence.

This difference becomes crystal clear when you look at real-world health situations that go beyond a simple ER visit.

Real-World Scenarios Uncover the Difference

Let’s make this practical. Imagine you’re an avid skier spending a year in the French Alps. You take a bad tumble on the slopes and tear a ligament in your knee.

- With Travel Insurance: Your policy would almost certainly cover the emergency room visit, the initial diagnosis, and probably the surgery to fix the ligament. But that’s likely where it stops. The six months of physical therapy you need to get back on your feet? You’d be on your own for that, or the policy would expect you to fly home to do it.

- With Expat Medical Insurance: This is exactly the kind of situation this plan is built for. It would cover the emergency services, the surgery, and the entire course of follow-up care, including all the necessary months of physical therapy with a local specialist.

Now, let’s take a non-emergency but equally important scenario. Say you’re an expat in Spain managing a chronic condition like diabetes.

- With Travel Insurance: This policy would be pretty much useless. It doesn’t cover routine check-ups with an endocrinologist, the recurring cost of insulin, or your regular blood tests. It’s just not designed for managing an ongoing, pre-existing condition.

- With Expat Medical Insurance: This is precisely what the plan is for. It covers your specialist appointments, prescription refills, and any other routine care you need to manage your condition effectively while living abroad. For a deeper dive, you can learn more by exploring our detailed guide on expat medical insurance vs travel insurance and which one you actually need.

These examples really drive home why picking the right type of insurance is so critical. A travel policy is a temporary patch for a temporary stay, while an expat plan is a sustainable healthcare solution for your new life abroad.

What Your Expat Medical Insurance Policy Actually Covers

Trying to figure out what an expat health plan actually covers can feel like you’re trying to decipher a secret code. But it’s simpler than it looks once you get the basic structure down. An expat plan isn’t a flimsy policy for emergencies; it’s built from the ground up to be your primary healthcare solution while you’re living abroad.

Think of it like building with LEGOs. Every solid plan starts with a strong foundation—the core benefits that handle the big, scary, and expensive medical needs. From there, you can snap on optional blocks, or riders, to build a policy that fits your life perfectly.

This modular approach is what makes a good expat medical insurance plan so valuable for anyone living overseas long-term. It’s not just a safety net; it’s a complete system for managing your health, no matter where you are.

The Foundation: Core Inpatient Coverage

At the heart of every single expat medical insurance policy is inpatient coverage. This is the non-negotiable part of your plan, covering serious medical events that require you to be admitted to a hospital. It’s designed to shield you from the kind of health crises that can be financially devastating.

Inpatient benefits will almost always include:

- Hospital Stays: This covers the cost of your room, nursing care, and other essential services when you’re admitted overnight.

- Surgeries: It takes care of the surgeon’s fees, anesthesiologist costs, and operating room charges for medically necessary procedures.

- Intensive Care Unit (ICU): For those critical situations, this covers the incredibly high costs of specialized ICU care.

- Diagnostic Tests: This includes things like MRIs, CT scans, and lab work done while you’re admitted to the hospital.

Without this core coverage, a single bad accident or a sudden illness abroad could easily lead to crippling debt. It’s the foundational layer of protection every single expat needs.

Adding the Next Layer: Outpatient Services

While inpatient care has your back for the big emergencies, you’ll also need coverage for your day-to-day health. That’s where outpatient coverage comes in. It handles all the medical care that doesn’t require a hospital stay and is typically the second major piece of a well-rounded plan.

Outpatient services usually cover:

- Doctor’s Appointments: Routine visits to your local doctor for check-ups or when you’re feeling under the weather.

- Specialist Consultations: Seeing experts like cardiologists, dermatologists, or orthopedic surgeons.

- Prescription Medications: Coverage for drugs your doctor prescribes to manage both short-term illnesses and ongoing conditions.

- Preventative Care: Services like vaccinations, annual physicals, and health screenings designed to keep you healthy from the start.

This is the part of your policy that really turns it from an emergency-only plan into a functional, everyday health insurance system, letting you proactively look after your well-being.

Customizing Your Plan with Optional Add-Ons

Once you have your inpatient and outpatient needs locked in, you can start customizing your policy with optional benefits. These modules let you pay only for the extra coverage you actually need, creating a plan that’s tailored just for you.

A well-structured expat health plan isn’t a one-size-fits-all product. It’s a modular system that provides essential protection at its core while offering the flexibility to add specific benefits like dental or vision care based on individual needs.

Common add-ons you can often choose from include:

- Dental and Vision: Comprehensive coverage for everything from routine dental check-ups and major dental work to eye exams and glasses.

- Wellness Benefits: Reimbursement for things like gym memberships, health screenings, and other proactive wellness activities.

- Maternity Coverage: If you’re planning to start or grow your family abroad, this covers prenatal care, delivery, and postnatal care.

The growing demand for this kind of specialized coverage is part of a bigger picture. The global market for travel medical insurance is exploding, with some forecasts predicting it will swell to about USD 10.21 billion by 2034. This just goes to show how essential tailored health protection has become for a global population. You can read more about the travel medical insurance market growth to get a better sense of this trend.

What Is Typically Not Covered

Knowing what’s not included is just as important as knowing what is. Every policy has its limits, and being aware of them ahead of time can save you from a nasty surprise when you go to make a claim.

Standard exclusions you’ll often see are:

- Elective Cosmetic Procedures: Any surgeries or treatments that aren’t medically necessary.

- Certain Pre-existing Conditions: Health issues you had before the policy started might be excluded or require a special review and a waiting period.

- Injuries from High-Risk Activities: If you’re into professional sports or very hazardous hobbies, you might not be covered without a specific add-on.

Always take the time to read the fine print in your policy documents. It’s the only way to get a crystal-clear picture of your benefits and your limitations before you ever need to use them.

Navigating Pre-Existing Conditions and Medical Evacuation

Let’s talk about two of the biggest worries for anyone living abroad: what happens if my old health issue flares up, and what if I have a major medical emergency far from home? These aren’t just minor details; they cut right to the core of feeling safe and secure in your new life. That’s why you absolutely have to understand two critical pieces of your expat medical insurance: how it handles pre-existing conditions and what medical evacuation really means.

First, what is a pre-existing condition? In simple terms, it’s any illness, injury, or medical issue you’ve had symptoms, a diagnosis, or treatment for before your new policy kicks in. This could be anything from asthma or diabetes to a knee injury from years ago. Being completely honest about your medical history on your application is non-negotiable. Hiding something could lead to a denied claim right when you need help the most.

Insurers have two main ways of looking at your health history, and knowing the difference is key to getting the right kind of coverage from the start.

Underwriting Your Health History

When you apply for an expat health plan, the insurance company needs to get a clear picture of your health. They typically do this in one of two ways.

- Moratorium Underwriting: Think of this as the “wait-and-see” approach. It’s faster because the insurer doesn’t ask for your full medical history upfront. Instead, if you make a claim, they’ll investigate to see if it’s related to a pre-existing condition. If you go for a set period (usually 24 months) without any symptoms or treatment for that condition, it may then become eligible for coverage.

- Full Medical Underwriting (FMU): This is the deep dive. You provide your complete medical history when you apply, and an underwriter reviews it before your policy even starts. Based on their review, they might offer to cover the condition as is, cover it but for a higher premium, or exclude it completely. It takes longer, but the huge advantage of FMU is clarity—you know exactly what is and isn’t covered from day one.

Getting a handle on how insurers approach these health issues is a massive step. For a more detailed look, you can find a ton of valuable information in our guide on medical travel insurance for pre-existing conditions. This knowledge gives you the power to pick a plan that genuinely fits your personal health needs.

Your Lifeline in a Crisis: Medical Evacuation

Now, let’s switch gears to a scenario nobody wants to think about: you’re in a serious accident or become critically ill in a place where the local hospital just isn’t equipped to handle it. This is where medical evacuation coverage goes from being a line item on your policy to an absolute lifeline. Frankly, it’s one of the most important benefits any expat health plan can offer.

Medical evacuation coverage arranges and pays to transport you from a place with inadequate care to the nearest medical center that can give you the treatment you need.

This is so much more than calling a local ambulance. We’re talking about coordinating a private, medically-staffed air ambulance to fly you to another city—or even another country—to get life-saving care.

Just think about what that means in the real world. A bad car accident in rural Southeast Asia or a major heart attack while living on a small island could have a grim outcome without this. The local clinic might be great for setting a bone, but they won’t have the neurosurgeons, cardiac specialists, or ICU technology needed for complex emergencies.

Your medical evacuation benefit handles all the dizzying logistics and astronomical costs, which can easily top $100,000 for an international air ambulance. It means your only job is to focus on getting better, not on the impossible task of arranging and funding your own emergency transport. For any expat, especially those living or traveling outside of major cities, this coverage is the ultimate safety net.

How to Choose the Right Expat Health Insurance Plan for You

Okay, so now you’ve got the basics down. You know what makes up an expat health plan. The real trick is putting those pieces together to build a plan that actually fits your life, not the other way around. This isn’t about finding some magical one-size-fits-all policy; it’s about making a smart, calculated decision based on where you’re going, your health, and your budget.

Picking the right expat medical insurance for long-term living abroad is a balancing act. You have to weigh what you can afford against the kind of coverage that lets you sleep at night. It’s a personal decision, and getting it right is crucial.

Assess Your Destination and Lifestyle

First things first, look at where you’re headed. The cost and quality of healthcare can be wildly different from one country to the next. What you’d pay for a routine doctor’s visit in Thailand might not even cover a cup of coffee in Zurich, and your insurance plan needs to account for that.

Start by digging into the local healthcare system. Is it mostly public, private, or a mix of both? Are medical costs generally low, or are you looking at prices that rival the notoriously expensive U.S. system? Knowing this helps you decide on the right coverage limits for your policy.

Next up, think about how you’ll be living. Are you a digital nomad bouncing between countries every few months, or are you putting down roots in a single city? A nomad absolutely needs a plan with broad, worldwide coverage. But if you’re staying put, a more localized—and usually cheaper—plan could be all you need.

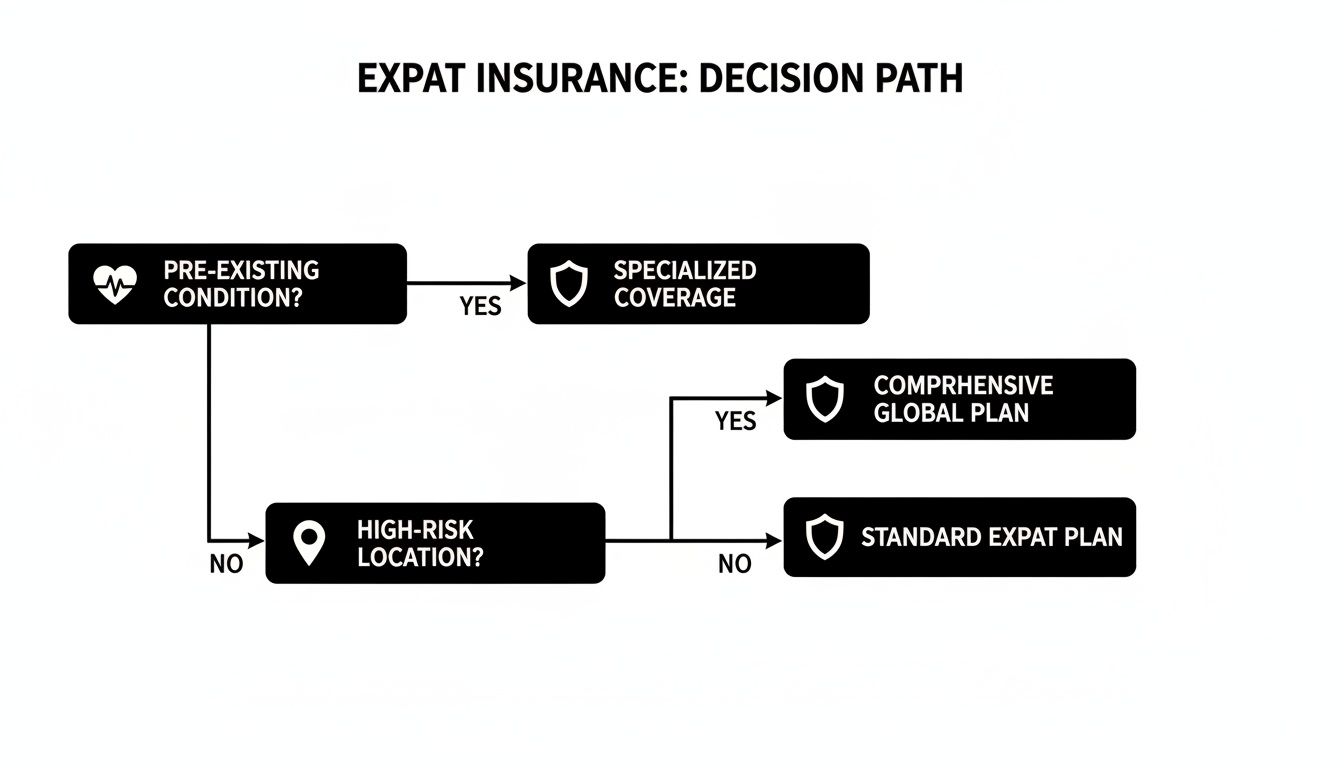

This little flowchart is a great way to visualize those first few decision points.

As you can see, things like pre-existing conditions and the medical standards in your new country are the foundational questions that shape everything else.

Evaluate Your Personal and Family Health Needs

Once you have a handle on the external factors, it’s time to look inward. This is where the plan really becomes tailored to you.

Be honest with yourself. Are you young and healthy, or do you have chronic conditions that need regular check-ups? Do you think you might need specialized care down the road? Your health history and what you anticipate for the future are non-negotiable factors here.

For families, the list of considerations gets even longer. Do you need maternity coverage for a growing family? What about routine check-ups, vaccinations, or even orthodontics for the kids? Each of these can be covered, but you’ll likely need to add them as specific benefits.

Choosing the right plan means matching your policy’s benefits directly to your life’s circumstances. A digital nomad prioritizes global flexibility and emergency care, while a retiree may focus on comprehensive coverage for chronic conditions and a low deductible.

We’re seeing a clear trend of expats thinking more long-term. While single-trip policies still dominate the market—making up around 61% of revenue—the real growth is in annual and long-stay plans. It shows that people who travel often or live abroad are finally realizing they need continuous, solid coverage.

A Practical Checklist for Different Expat Profiles

To make this a bit more concrete, let’s look at what different kinds of expats should be prioritizing. Here’s a quick-and-dirty checklist to see what really matters for your situation.

It’s clear that your needs can change dramatically based on your lifestyle. A plan that’s perfect for a solo digital nomad would be completely inadequate for a family settling in one place. This table helps break down the core considerations for a few common expat profiles.

Expat Profile Insurance Needs Checklist

| Consideration | Digital Nomad | Expat Family | Retiree Abroad |

|---|---|---|---|

| Global Coverage Area | ✔️ Must-Have | ❌ Nice-to-Have | ❌ Nice-to-Have |

| Emergency Evacuation | ✔️ Must-Have | ✔️ Must-Have | ✔️ Must-Have |

| High Deductible Option | ✔️ Good for Savings | ❌ Less Ideal | ❌ Less Ideal |

| Maternity/Newborn Benefits | ❌ Rarely Needed | ✔️ Must-Have | ❌ Rarely Needed |

| Wellness & Preventative Care | ❌ Nice-to-Have | ✔️ Must-Have | ✔️ Must-Have |

| Dental & Vision Add-ons | ❌ Nice-to-Have | ✔️ Must-Have | ✔️ Must-Have |

| Chronic Condition Coverage | ❌ Less Common | ❌ Nice-to-Have | ✔️ Must-Have |

| Low Out-of-Pocket Costs | ❌ Less Ideal | ✔️ Must-Have | ✔️ Must-Have |

| Reputation for Claims | ✔️ Must-Have | ✔️ Must-Have | ✔️ Must-Have |

By using this checklist, you can quickly pinpoint the non-negotiables for your specific situation. It’s all about aligning the policy features with your real-world needs to avoid paying for benefits you’ll never use or, worse, finding yourself without coverage when you need it most.

Of course, a huge part of this puzzle is understanding the specific requirements of your destination country. For a deeper dive into that, check out our guide on how to choose the right expat medical insurance by country.

By walking through these steps—your destination, your health, and your lifestyle—you can go from feeling totally overwhelmed to feeling confident you’re making the right choice. The goal is to find a plan that acts as a true safety net, protecting your health and finances no matter where your adventure takes you.

Common Questions About Expat Health Insurance

As you get closer to choosing a plan, some practical questions always pop up. Getting straight answers to these common queries is often the final step to feeling confident about your decision. Let’s tackle some of the things people ask us most often.

Can I Just Use My Home Country Health Plan?

This is probably the number one question we hear, and for the vast majority of expats, the answer is a hard no. Domestic health plans are built to work within one country’s system—its network of doctors, its billing codes, its regulations.

Once you move abroad, that plan offers little to no coverage for anything beyond a true, short-term travel emergency. It was never designed for routine check-ups, ongoing treatments, or significant medical care in another country. This is why a dedicated expat health plan isn’t just a good idea; it’s an absolute necessity.

What Is the Difference Between Inpatient and Outpatient Care?

Getting this distinction is crucial to understanding what your policy actually covers. The easiest way to think about it is this:

- Inpatient Coverage: This kicks in when you’re in a serious medical situation and need to be formally admitted to a hospital. It’s for the big stuff—your hospital room, major surgeries, intensive care, and all the treatments you receive while you’re staying there.

- Outpatient Coverage: This covers pretty much everything else. It’s for all the medical care where you aren’t admitted overnight. Think doctor’s appointments, visits to a specialist, picking up prescription drugs, or getting lab tests and X-rays.

The best expat health plans give you solid coverage for both inpatient and outpatient care. This comprehensive approach is what truly separates real expat insurance from a basic travel policy, protecting you from minor sniffles to major medical events.

How Does My Coverage Work in Different Countries?

Expat insurance is built for a global life. When you pick a plan, you’ll choose a geographic area of coverage. The two most common options are “Worldwide” or “Worldwide excluding the USA.” The second option is often cheaper simply because healthcare costs in the United States are so high.

Within your chosen region, you’re free to get treatment from a huge network of doctors, clinics, and hospitals. This gives you the flexibility to get quality care whether you’re in your new home country or just traveling to another spot within your coverage zone.

Are Dental and Vision Benefits Included?

Most standard expat health plans don’t include dental and vision care right out of the box. Instead, they’re offered as optional add-ons, or “riders.”

This structure actually works in your favor. It lets you customize your policy so you only pay for the extra coverage you really need. If you know you’ll need routine dental cleanings, major work like a crown, or a new pair of glasses, adding these modules is a very smart move.

Feeling more confident about your options? The team at Expat Global Medical has been helping expats navigate these questions since 1992. Get personalized advice and a free, no-obligation quote to find the perfect plan for your new life abroad. Start your free quote with Expat Global Medical today.