")

For most Americans, the dream of retiring abroad is well within reach—your Social Security benefits can follow you almost anywhere. This means you can count on that hard-earned income while immersing yourself in a new culture. But there’s one critical detail you absolutely cannot afford to ignore: U.S. Medicare does not cover you overseas. This makes private expat medical insurance an absolute necessity.

Your Social Security Benefits Living Abroad

The idea of retiring to the sun-kissed shores of Europe or the vibrant streets of Mexico, all while your U.S. Social Security checks keep rolling in, is a reality for a growing wave of Americans. In fact, a whopping 760,000 retirees are already doing it, according to the latest Social Security Administration (SSA) reports.

That number is staggering when you consider it was just 431,000 in 2019. It marks a nearly 76% surge in just a few years, proving that expats are increasingly seeking lower costs of living and dream lifestyles overseas. You can explore more on this trend in 401k Specialist Magazine’s piece on global retirement indexes.

This guide is built to give you a complete picture of what a global retirement looks like, with your Social Security as the reliable foundation for your new life. We’ll walk through how payments are handled across borders and break down the eligibility rules, but our core focus will be on the most crucial decision you’ll make: securing your health with expat medical insurance.

The Most Important Factor Expat Retirees Face

While the financial logistics are surprisingly straightforward, the single biggest challenge you’ll need to solve is healthcare. Many retirees are shocked to discover their U.S. Medicare coverage becomes practically useless the moment they move abroad.

Relying on Medicare for healthcare coverage while living overseas is a significant financial risk. A single medical emergency could potentially wipe out years of savings, making private expat medical insurance an essential safeguard for your retirement funds.

This creates a dangerous gap in your safety net, leaving your retirement savings exposed to potentially catastrophic medical bills. Without a proper plan, the very Social Security income that’s supposed to provide security is left vulnerable. This isn’t just a minor detail; it’s the central pillar of a successful retirement abroad.

Bridging the Gap with Expat Medical Insurance

To protect both your health and your nest egg, securing private expat medical insurance is non-negotiable. Unlike the plan you had back home, international health insurance is specifically designed for the unique needs of people living abroad.

Here’s what a solid expat medical plan brings to the table:

- Global Coverage: You get access to a trusted network of doctors and hospitals in your new country and often worldwide.

- Emergency Medical Evacuation: This covers transportation to the nearest top-tier medical facility if local care isn’t up to snuff—a benefit Medicare does not provide.

- Routine and Specialist Care: Benefits are designed to cover everything from regular check-ups to specialized treatments, giving you comprehensive care.

- Peace of Mind: You can relax, knowing an unexpected illness or accident won’t derail your financial stability.

By closing the Medicare gap with the right insurance, you transform your Social Security benefits from a simple income stream into a truly secure foundation for a fulfilling life abroad.

Before we dive deeper, it’s helpful to have a high-level view of the key areas you’ll need to manage. This table summarizes the most critical considerations for any U.S. citizen planning to receive Social Security benefits while living overseas.

Key Considerations for US Expats and Social Security

| Factor | Key Takeaway | Where to Find More Info |

|---|---|---|

| Eligibility & Citizenship | Generally, U.S. citizens can receive benefits abroad. Non-citizens face stricter rules and may lose payments after 6 months outside the U.S. | SSA’s “Your Payments While You Are Outside The United States” |

| Country Restrictions | Payments are blocked to a handful of countries like Cuba and North Korea. Some other countries have specific restrictions you must follow. | SSA’s Payments Abroad Screening Tool |

| Payment Logistics | Direct deposit to a U.S. bank or a foreign bank (in select countries) is the easiest way to receive your money. | Direct Deposit for International Recipients |

| Healthcare (Medicare) | Medicare provides virtually no coverage outside the U.S. This is the biggest gap you must fill with private expat medical insurance. | Medicare.gov’s page on coverage outside the U.S. |

| Tax Implications | Your Social Security may be taxable by both the U.S. and your host country. Totalization Agreements can prevent double taxation. | IRS Publication 915, “Social Security and Equivalent Railroad Retirement Benefits” |

| Reporting Requirements | You must report life events like marriage, divorce, or a change of address to the nearest Federal Benefits Unit (FBU). | List of U.S. Embassies and Consulates with FBUs |

This table is your starting point. Each of these factors involves important details and decisions that we will explore throughout this guide, ensuring you have the knowledge to make your retirement abroad both successful and secure.

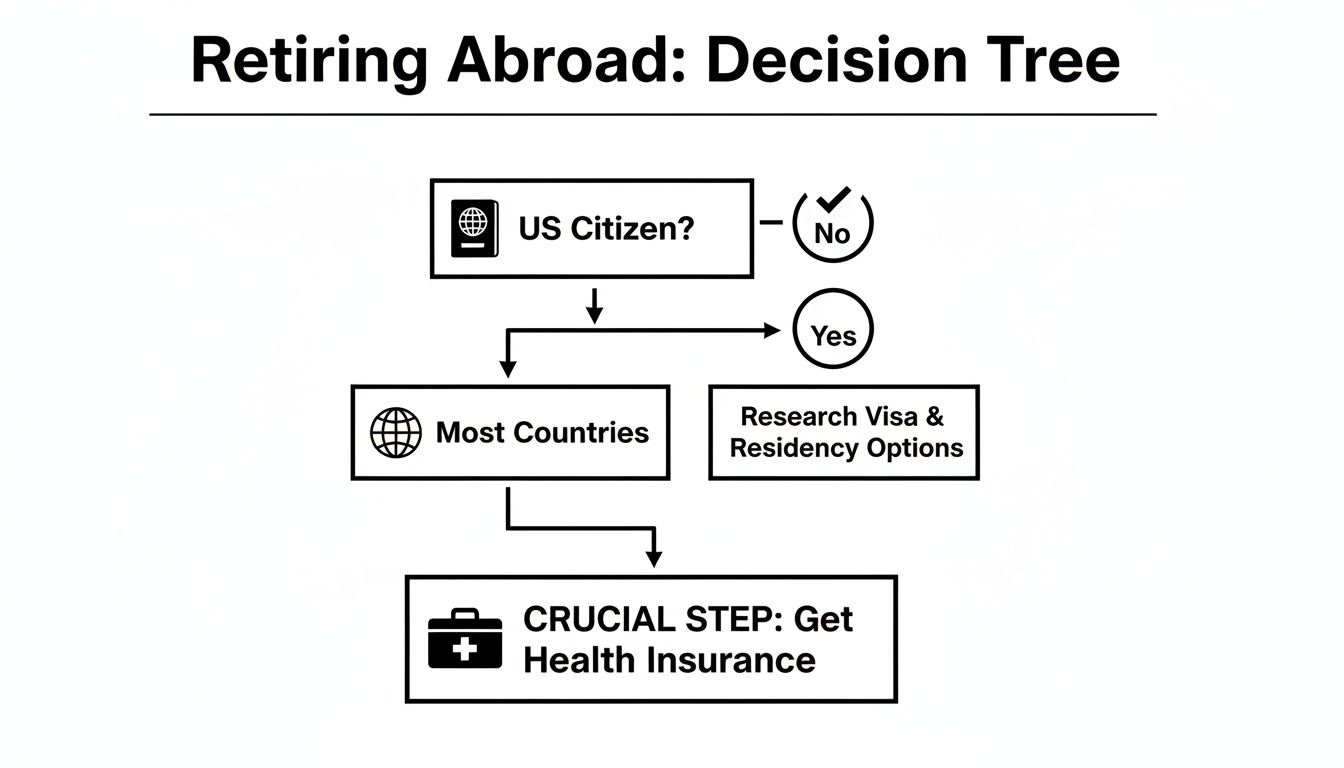

Understanding Eligibility and Country Restrictions

So, you’re dreaming of retiring abroad, but can your Social Security benefits make the journey with you? Before you start packing, it’s essential to understand the rules. Think of your eligibility as a passport for your payments—it’s widely accepted, but a few key regulations and a handful of destinations are off-limits.

The good news? For most U.S. citizens, getting social security benefits while living abroad is absolutely possible.

If you’re a U.S. citizen and have earned enough work credits to qualify for retirement, disability, or survivor benefits, you can generally have your payments sent to most countries. Your citizenship is the master key here. The rules get much stricter for non-U.S. citizens, who might see their benefits cut off after being outside the U.S. for more than six consecutive months unless they meet very specific criteria.

This decision tree lays out the typical thought process for a U.S. citizen planning a move abroad and flags one of the most important next steps: figuring out healthcare.

As you can see, once you’ve confirmed you can receive benefits in your chosen country, you have to tackle the healthcare gap. Medicare generally doesn’t cover you overseas, so this is a critical piece of the puzzle to solve. Without a solid expat medical insurance plan, the rest of your planning is built on a shaky foundation.

Countries Where Payments Are Restricted

While your benefits can follow you to popular spots like Mexico, Portugal, or Japan, the U.S. Treasury Department does block payments to a small list of countries. Currently, the Social Security Administration (SSA) cannot send money to anyone living in Cuba or North Korea.

If you move to one of these countries, your benefits will be put on hold. You won’t lose them forever, but you can only claim the accumulated payments once you move to a country where payments are allowed.

Beyond that, other U.S. sanctions can impact payments. The SSA keeps a running list of nations with certain restrictions, which currently includes places like Belarus and Azerbaijan. To get a clear “yes” or “no” for your dream destination, the SSA has a handy online Payments Abroad Screening Tool that gives you the answer country by country.

The Role of Totalization Agreements

What if you’ve worked in both the United States and another country? This is where Totalization Agreements come into play, and they are a massive help. These are basically international treaties the U.S. has with 30 other nations to solve two big headaches for people who have worked globally.

First, they stop you from being double-taxed. Without an agreement, you could get hit with social security taxes from both countries on the same income. These agreements assign your coverage to just one country’s system, so you don’t pay twice.

Second, they can help you qualify for benefits in the first place. Let’s say you don’t have enough work credits in the U.S. or in your other country to get a pension. A Totalization Agreement allows you to combine your work credits from both places to meet the minimum requirements.

Totalization Agreements act like a financial bridge, connecting your work history across borders. They ensure that your contributions in one country aren’t lost and can help you secure a retirement benefit you might not have qualified for otherwise.

This is a huge advantage for expats who have split their careers between the U.S. and countries like Canada, Germany, the United Kingdom, Japan, or Australia. Federal employees should also be aware of the Windfall Elimination Provision (WEP), which can reduce your Social Security benefits if you also get a pension from a job where you didn’t pay Social Security taxes. Getting a handle on these rules is a non-negotiable part of planning your finances for a life abroad.

How to Manage Payments and Taxes from Abroad

Okay, so you’ve confirmed you’re eligible. Now for the nuts and bolts: getting the money and keeping Uncle Sam happy. Setting up your Social Security benefits while living abroad comes down to a pretty straightforward payment system and a non-negotiable duty to stay current with your U.S. taxes. Getting these logistics right from the start is the key to a stress-free financial life overseas.

You basically have two ways to get your monthly benefits, and each has its own pros and cons. Your choice will really boil down to your banking setup and how comfortable you are with managing international money transfers.

Choosing Your Payment Method

The Social Security Administration (SSA) will push you toward direct deposit, and for good reason—it’s the most secure and reliable way to get paid. They’ve practically phased out mailing paper checks internationally because it’s slow, risky, and a logistical headache. Electronic payments are the new standard.

Here’s a look at your two main choices:

- Direct Deposit to a U.S. Bank Account: This is the simplest and, frankly, the most recommended route. Your money lands in your U.S. account like clockwork. From there, you can transfer it to your foreign bank whenever you like using services such as Wise or Revolut. This method gives you total control over currency conversion rates and timing.

- Direct Deposit to a Foreign Bank Account: The SSA’s International Direct Deposit (IDD) program is an option in many countries. It sends your payment straight to your local bank in the local currency. While it sounds convenient, the big drawback is that you have no control over the exchange rate—it’s set by whatever the U.S. Treasury’s processing bank decides that day.

For most expats, keeping a U.S. bank account is the most flexible approach. It lets you easily pay any U.S.-based bills and gives you the freedom to shop for the best exchange rates when you need to move money abroad.

Navigating U.S. Tax Obligations as an Expat

Here’s a reality check every U.S. citizen living abroad must face: you are taxed on your worldwide income, no matter where you call home. And yes, that includes your Social Security benefits. Forgetting this rule is one of the biggest—and costliest—mistakes an American expat can make.

Your U.S. citizenship comes with an ongoing obligation to file a federal tax return every year. This requirement doesn’t disappear when you move abroad, and your Social Security income must be reported.

Whether your benefits are taxable depends on your “combined income.” If your total income, including half of your Social Security benefits, tops $25,000 for an individual or $34,000 for a married couple, a slice of your benefits will be hit with U.S. income tax. It’s also critical to know that Social Security income does not qualify for the Foreign Earned Income Exclusion (FEIE).

How Tax Treaties Prevent Double Taxation

Living abroad often makes you a tax resident in your new country, too. So, how do you keep from being taxed twice on the same income—once by the U.S. and again by your host nation? This is where tax treaties, also known as tax conventions, save the day.

The U.S. has tax treaties with dozens of countries specifically designed to prevent this problem. For those navigating their finances and tax obligations while living abroad, understanding international mechanisms such as Double Tax Agreements is crucial to avoid being taxed twice on the same income.

These agreements lay out specific rules that decide which country gets the first crack at taxing different types of income, including Social Security. Typically, these treaties let you claim a credit on your U.S. tax return for taxes you’ve already paid to your country of residence. This nifty mechanism ensures you don’t pay more in total tax than the higher of the two countries’ rates.

The rules can get complicated, which is why many expats hire a tax professional who specializes in expat issues. It’s often money well spent to ensure you’re compliant and not overpaying.

Solving the Expat Health Insurance and Medicare Gap

Receiving Social Security benefits while living abroad gives you a solid financial floor, but it comes with a massive catch—one that many expats dangerously misunderstand. The assumption that U.S. Medicare will cover you overseas is a myth, and believing it can put your entire retirement at risk.

This simple fact creates the single biggest financial puzzle for American retirees to solve. If you move abroad counting on Medicare, you’re exposing yourself to catastrophic financial blows from even a single, unexpected medical emergency. This is where a private expat medical insurance plan becomes non-negotiable.

Why Medicare Falls Short Abroad

Think of Medicare as a healthcare system with strict geographical borders. Once you cross the U.S. border to live, its protective shield essentially vanishes. Barring a few extremely rare and specific situations, Medicare will not pay for your hospital stays, doctor visits, or prescription drugs in another country.

This leaves you completely exposed. You could be on the hook for 100% of your medical costs out-of-pocket, for everything from a minor illness to a life-threatening accident. In many countries, hospitals will demand proof of payment before they even begin treatment, which can be a terrifying prospect in an emergency.

Protecting your Social Security income is about more than just managing payments and taxes. It’s about building a financial shield against the single biggest threat to your savings: an unforeseen health crisis in a country where your primary insurance is worthless.

A robust expat insurance plan is that shield. It’s specifically designed to plug this critical Medicare gap, ensuring your hard-earned retirement funds are spent on your dream life abroad, not wiped out by one hospital bill.

What to Look for in an Expat Medical Insurance Plan

Not all insurance is created equal. A basic travel policy just won’t cut it for long-term living. A true expat medical plan needs to offer features designed for someone who has made another country their home.

When you’re shopping around, you absolutely need a plan that includes:

- Comprehensive Inpatient and Outpatient Care: This covers the big stuff like hospitalizations and surgeries, as well as routine doctor visits and specialist appointments.

- Emergency Medical Evacuation: This is a deal-breaker. If you have a serious medical event in a place without top-tier facilities, this benefit covers the sky-high cost of flying you to the nearest hospital that can handle your needs.

- A Strong Global Network: Look for providers with vast networks of trusted hospitals and doctors worldwide. This gives you choices and ensures you have access to quality care wherever you are.

- 24/7 Assistance and Support: When you’re in a crisis, you need a team you can call anytime for help with claims, finding care, and coordinating all the logistics.

These features create a safety net that travels with you, protecting both your health and your financial stability. For a deeper dive, you can explore more about international health insurance options for US citizens to see how these plans are structured.

Healthcare Quality and Insurance Needs in Top Expat Destinations

The quality of healthcare varies dramatically from country to country, and that directly impacts your insurance needs. Many popular retirement spots for Americans have excellent healthcare systems, but getting access often requires either enrolling in a national plan (which isn’t always an option for expats) or having solid private insurance.

Just look at the landscape in countries where thousands of U.S. retirees are already collecting Social Security. Japan, home to over 55,000 U.S. recipients, has a world-class system. Germany, with 23,000 recipients, ranks 13th worldwide for health—leagues ahead of the U.S. spot at 69th. But even in these top-tier countries, navigating the local system without proper private coverage can be a complex and expensive headache.

In other popular destinations like Mexico, where 33,000 Americans enjoy living costs of around $698 a month, or Greece, with its 13,000 SSA recipients, private insurance is absolutely essential. Medicare skips these borders entirely, leaving you to face local systems or potentially massive out-of-pocket bills.

This reality highlights a universal truth for expats: no matter how great your destination’s healthcare is, a private insurance plan is the key to getting seamless, affordable access to care without putting your finances on the line. It’s the final, crucial piece of the puzzle for a successful and worry-free retirement abroad.

Staying Compliant with SSA Reporting Rules

Getting your Social Security benefits while living abroad isn’t a “set it and forget it” deal. The Social Security Administration (SSA) needs you to keep an open line of communication, reporting certain life changes to make sure you remain eligible. Think of it as a periodic check-in to confirm your status. Staying on top of these rules is the key to keeping your payments flowing without any hiccups.

This ongoing responsibility is simply your side of the bargain. If you don’t report key events, you could end up with overpayments that you’ll have to pay back or, even more commonly, a sudden suspension of your benefits. The bottom line is the SSA needs to know about any event that could affect your payment amount or eligibility.

What Events Must You Report to the SSA?

As an expat receiving benefits, you have to promptly let the SSA know when certain life events happen. Keeping your records up-to-date is the best way to prevent payment disruptions and potential headaches down the road.

You’ll need to contact the SSA if you:

- Change your address: This is a big one, especially since they’ll be mailing you a mandatory questionnaire. You don’t want to miss it.

- Begin or stop working: Any work, even part-time, can affect your benefit amount. This is especially true if you haven’t reached your full retirement age.

- Change your marital status: Getting married, divorced, or losing a spouse can directly impact spousal or survivor benefits.

- Are unable to manage your own funds: If a health condition changes and you need someone else to manage your benefits (a representative payee), the SSA has to be officially notified.

Usually, you’ll handle this reporting through the nearest U.S. Embassy or Consulate, which will have a Federal Benefits Unit (FBU) on site.

The Critical SSA Questionnaire: Form SSA-7161 or SSA-7162

Every one or two years, the SSA will mail a critical document to the address they have for you. It will be either Form SSA-7161 or SSA-7162, sometimes just called the “Report to United States Social Security Administration.” This form is basically a “proof of life” and status check.

Failure to complete and return this questionnaire is the single most common reason expats have their Social Security benefits suspended. The SSA will simply assume you are no longer eligible if they don’t get your completed form back on time.

This isn’t a friendly suggestion; it’s a mandatory requirement. The form asks you to confirm your personal information and answer a few questions about your work, marital status, and where you’re living. It’s their way of preventing fraud and ensuring payments only go to people who are actually eligible.

Actionable Tips for Timely Compliance

Given how crucial this questionnaire is, you absolutely cannot afford to let it slip through the cracks. International mail can be notoriously unreliable, so you need a proactive game plan to make sure you receive, complete, and return it without a hitch.

Here are a few practical steps to stay on top of it:

- Use a Reliable Mailing Address: If the local post in your new country is spotty, think about using a U.S.-based mail forwarding service or a P.O. box with a solid reputation.

- Mark Your Calendar: If you know the form typically arrives every two years around a certain month, set a recurring reminder on your calendar. If it doesn’t show up when expected, reach out to the FBU proactively.

- Return Promptly with Tracking: Don’t let the form sit on your desk. When you mail it back, use an international courier service that offers tracking so you have solid proof of delivery.

- Keep Copies: Always, always make a digital scan or photocopy of the completed form for your records before you send it off.

By treating these reporting duties with the seriousness they deserve, you can ensure your hard-earned Social Security benefits remain a stable source of income for your global retirement.

Your Blueprint for a Secure Retirement Abroad

So, is living your retirement dream overseas really possible? Absolutely, as long as you have a solid plan in place. This guide has walked you through the nuts and bolts, and as you can see, collecting your Social Security benefits while living abroad is actually pretty straightforward once you know the rules.

It really boils down to a few key steps: making sure you’re eligible, figuring out the logistics of getting paid, and staying on top of your U.S. taxes. But the most critical piece of the puzzle—the one that holds everything together—is securing private expat medical insurance to fill that Medicare gap.

Protecting your health with a reliable insurance partner is the cornerstone of a secure retirement. It safeguards your financial future and empowers you to enjoy a fulfilling global lifestyle with complete peace of mind.

When you put your health coverage first, you’re building a firewall around your hard-earned savings, protecting them from a sudden medical crisis. This is the final, essential step that makes sure your Social Security income is funding your adventure, not getting wiped out by an unexpected hospital bill.

As you get your ducks in a row, it’s also a great idea to learn more about how to retire overseas, which can give you an even clearer roadmap. Taking these proactive steps is what allows you to build a secure, fulfilling, and truly incredible life, no matter where in the world you choose to call home.

Common Questions from Expats

When you’re figuring out Social Security from another country, a lot of specific questions pop up. Let’s walk through some of the most common ones we hear from expats, especially when it comes to the tricky relationship between Social Security, Medicare, and staying on the right side of the SSA’s rules.

Does My Medicare Part B Cover Me If I Live Overseas?

This is probably one of the biggest—and most dangerous—misconceptions for Americans retiring abroad. The short answer is no.

Medicare Part B, just like Part A, offers virtually no coverage outside of the United States. Paying those monthly premiums won’t make it work in your new home country.

So why do some expats keep paying for it? Mostly as a defensive move. They want to avoid the steep late enrollment penalties that kick in if they ever decide to move back to the U.S. and need Medicare again. But for your actual day-to-day healthcare or any emergencies you might face while living abroad, you absolutely must get a separate, private expat medical insurance plan.

Trying to rely on Medicare overseas is a huge financial gamble. You could end up paying 100% of your medical bills out of your own pocket, a scenario that could quickly drain a lifetime of retirement savings.

What Happens If I Don’t Send Back That SSA Questionnaire on Time?

If you live abroad, the Social Security Administration (SSA) will periodically mail you a questionnaire (either Form SSA-7161 or SSA-7162) to verify you’re still eligible for benefits. It’s their way of checking in.

Not completing and returning this form on time is the single most common reason expats suddenly find their payments have stopped.

If the SSA doesn’t get that form back by the deadline, they’ll suspend your benefits. It’s crucial to have a reliable mailing address and a system for getting that document back to them promptly. A lost form means your income stream gets cut off, and trying to fix that from another country can be a bureaucratic nightmare.

Can My Spouse, Who Isn’t a U.S. Citizen, Get Survivor Benefits Abroad?

This is where things get complicated, and the answer really depends on a few key details: your spouse’s citizenship, where they live, and how long they lived in the U.S. with you during your marriage.

A non-citizen spouse might be eligible for survivor benefits, but there are specific hurdles to clear. For example, payments can often continue if they:

- Lived in the U.S. for a certain period (often five years) while married to you.

- Are a resident of one of the 30 countries that has a Social Security agreement (a Totalization Agreement) with the United States.

These international agreements act like a bridge, keeping the benefits flowing across borders. Since every family’s situation is different, we strongly advise you to contact the SSA’s Office of International Operations or the nearest Federal Benefits Unit. They’re the only ones who can give you official guidance based on your exact circumstances.

Sorting out the complexities of Social Security and healthcare abroad takes careful planning, but you don’t have to figure it all out alone. Expat Global Medical specializes in creating insurance solutions that protect both your health and your finances, so you can enjoy your retirement anywhere in the world with confidence. Get your free quote today and build a secure foundation for your life overseas.