")

Securing the right Spain medical insurance is a critical first step for any expat planning a move. For many non-EU citizens, it’s not just a safety net—it’s a non-negotiable requirement for obtaining a visa and residency.

Spanish authorities require proof of a specific type of private health insurance to ensure you won’t be a financial burden on the public system. The policy must be comprehensive, offering full coverage with no co-payments or deductibles. This guide is designed to help expats navigate this essential requirement with confidence.

Navigating Healthcare in Spain: An Introduction for Expats

Before you can immerse yourself in Spain’s vibrant culture, you need to understand its healthcare system. Spain operates a dual system with both public and private options. As an expat, knowing which one you’ll use is crucial for a seamless transition into your new life.

The public system, the Sistema Nacional de Salud (SNS), is highly regarded and comprehensive. It’s like a well-run public transport network—efficient and covering almost everything. However, like public transit, it can experience delays, sometimes leading to long waits for non-urgent specialist appointments.

Private medical insurance, tailored for expats, is like having your own car. It offers speed, convenience, and direct access to specialists, many of whom are English-speaking. This option allows you to bypass public queues and often includes perks like private hospital rooms, which can be a significant comfort in a new country.

To help you understand the landscape, here’s a quick comparison from an expat’s perspective.

Public vs. Private Healthcare in Spain at a Glance

| Feature | Public System (SNS) | Private System (Expat Insurance) |

|---|---|---|

| Eligibility | Tied to social security contributions (work/pension) | Open to any expat who purchases a plan |

| Cost | Funded by taxes, no monthly premiums | Monthly premiums paid to an insurance company |

| Wait Times | Can be long for specialists and non-urgent procedures | Significantly shorter, often with direct specialist access |

| Doctor Choice | Assigned a primary care doctor; limited choice | Freedom to choose doctors and specialists within the network |

| Language | Primarily Spanish-speaking staff | Wide availability of English-speaking doctors and staff |

| Facilities | Shared hospital rooms are common | Private rooms are standard |

| Visa Requirement | Not suitable for initial residency applications | Mandatory for most non-EU expat visas |

This table clearly illustrates why private insurance is the go-to choice for most expats, especially during the initial residency process. It’s not just about convenience; it’s a legal necessity.

Who Needs Which Type of Coverage as an Expat

So, who qualifies for the public system, and who must secure private expat insurance?

Eligibility for the public SNS is almost always linked to legal residency and contributing to Spain’s social security system. This generally means you’re covered if you are:

- An employee working for a Spanish company

- A registered self-employed worker (autónomo) in Spain

- A state pensioner from the EU/EEA or a country with a reciprocal healthcare agreement

- A long-term resident who meets specific conditions

For most expats arriving on visas like the Non-Lucrative Visa or Digital Nomad Visa, private insurance isn’t just an option; it’s a mandatory part of the application. Understanding the latest Spain residency requirements is critical, as having the correct medical insurance is a make-or-break detail for visa approval.

The Spanish government requires this private coverage to ensure new residents can handle their own healthcare needs from day one, without immediately relying on the public system. It’s a foundational requirement that shows you’re self-sufficient as you begin your residency journey.

This initial private policy is your golden ticket to residency. It provides the peace of mind that you’re fully covered and compliant from the moment you land. In the next sections, we’ll dive deeper into how both systems work, so you can make the best choice for your health as an expat in Spain.

Understanding Spain’s Public Healthcare System

To make an informed choice about your Spain medical insurance, it’s helpful to understand the public system you may eventually join. The Sistema Nacional de Salud (SNS) is a universal system funded primarily through social security contributions from workers and employers.

Once you start working in Spain and paying into the system, you gain access to this national service.

The system is decentralized. While the central government sets national standards, each of Spain’s 17 autonomous communities manages its own healthcare services. This can lead to minor regional differences, but the core commitment to high-quality care remains consistent nationwide.

Who Is Eligible for Public Healthcare?

Access to the SNS is not automatic for every expat. Your eligibility is directly tied to your legal residency status and, crucially, your social security contributions. As an expat, you typically qualify if you meet one of these criteria:

- You’re an employee: If you have a work contract with a Spanish company, you’ll be registered for social security and automatically entitled to public healthcare.

- You’re self-employed (autónomo): As a registered freelancer paying monthly social security contributions, you are also covered.

- You’re a pensioner: Retirees from the EU/EEA or countries with a reciprocal agreement can transfer their healthcare rights to Spain using an S1 form.

- You’re a dependent: The spouse, partner, or child (under 26) of someone already covered by social security can often be added as a dependent.

For many new expats, particularly those on non-lucrative or other non-working visas, these conditions won’t apply initially. This is precisely why private Spain medical insurance is a mandatory requirement for their residency applications.

The Convenio Especial: A Pay-In Option for Expats

What if you’re an expat who doesn’t fit into those categories? Spain offers a solution called the Convenio Especial. This is a special pay-in scheme allowing certain residents to access the public SNS by paying a monthly fee.

This option is designed for long-term residents who aren’t otherwise eligible—for example, an early retiree from a non-EU country. The monthly fee is generally around €60 for those under 65 and €157 for those 65 and over.

The Convenio Especial is an excellent bridge to the public system, but it has limitations: it doesn’t cover prescription costs and, most importantly, cannot be used to meet visa requirements for new expats. It’s a solution for those already registered as residents in Spain.

How to Register and Get Your Health Card

Once you are eligible and registered with social security, the final step is obtaining your tarjeta sanitaria (health card). This card is your key to the public healthcare system.

- Get Your Social Security Number: This is the first step. Your employer usually handles it, or you’ll do it when registering as an autónomo.

- Register at Your Local Health Center (Centro de Salud): Visit the health center assigned to your address with your residency card (TIE), social security document, and proof of address (empadronamiento).

- Receive Your Health Card: After processing, your tarjeta sanitaria will be issued, granting you access to an assigned family doctor and the broader public network.

Spain’s system covers 99.5% of the population and is highly efficient, with healthcare spending at €2,771 per capita, nearly 33% below the EU average.

Despite the excellence of the SNS, many expats opt for private cover to bypass long wait times for specialists and overcome potential language barriers. Understanding the practical differences between public vs private healthcare for expats is key to finding the right fit for your peace of mind.

Why Private Insurance Is Often a Non-Negotiable for Expats in Spain

For most non-EU expats dreaming of a life in Spain, private medical insurance isn’t just a good idea—it’s an absolute requirement. The primary reason is that Spanish authorities mandate it for nearly every long-stay visa and residency application.

Whether you’re an expat applying for the Non-Lucrative Visa, the Digital Nomad Visa, or another long-term permit, the consulate will demand proof of comprehensive private health coverage. This policy must meet strict criteria, acting as your healthcare safety net until you may become eligible for the public system.

This rule ensures that new expat residents do not place an immediate strain on Spain’s public finances and can support themselves from day one.

The Gatekeeper for Your Expat Visa and Residency

Think of your private insurance policy as the key that unlocks your new life in Spain. Without the right one, your visa application is almost certain to be rejected. The Spanish government is explicit that your insurance must provide coverage at least equivalent to its public Sistema Nacional de Salud (SNS).

This means your expat policy must have these critical features:

- Full Coverage Across Spain: Your policy must cover everything, everywhere in Spain—from GP visits to specialist appointments, surgery, and hospitalization.

- Zero Co-payments (Sin Copagos): This is a deal-breaker. Your plan must cover 100% of medical costs. Policies with per-service fees are not acceptable for visa applications.

- No Deductibles or Waiting Periods: Your coverage must be active from day one. You cannot have a waiting period for benefits or an initial amount to pay out-of-pocket.

- Repatriation Coverage: The policy must include costs for medical evacuation and, in a worst-case scenario, the repatriation of remains.

Let me be clear: a standard travel insurance plan won’t cut it. You absolutely need a dedicated Spain medical insurance policy designed specifically for expats.

Beyond the Paperwork: The Real-World Perks for Expats

While fulfilling visa requirements is the initial driver, many expats maintain their private insurance long after settling in. The practical, day-to-day benefits offer a level of convenience that the public system can sometimes lack.

The biggest advantage for an expat is speed. With a private plan, you can often book an appointment directly with a specialist and be seen within days, bypassing the public system’s referral process and potentially long waiting lists.

This direct and rapid access to specialized care is one of the most compelling reasons expats stick with private coverage. It eliminates long waits and provides incredible peace of mind when a health issue arises.

It’s also worth noting the pressures on the public system. In 2024, Spain had over 1 million registered healthcare professionals but only 296 hospital beds per 100,000 people—well below the EU average of 525. This contributes to longer wait times. You can explore more on Spain’s healthcare professional statistics at INE.es. Private facilities help alleviate this pressure.

Comfort and Clear Communication for the Expat Community

The patient experience is another area where private healthcare shines for expats. A private plan typically guarantees a private room during hospitalization, offering peace and quiet for recovery.

Furthermore, the language barrier is a significant consideration for many expats. Private hospitals and clinics cater to the international community, making it much easier to find English-speaking doctors and staff. Being able to communicate clearly about your health in your native language is invaluable.

Ultimately, a private Spain medical insurance plan serves two vital roles for an expat: it’s your ticket to legal residency and your tool for ensuring fast, comfortable, and stress-free medical care in your new home.

How to Choose the Right Expat Medical Insurance Plan

Choosing the right Spain medical insurance can feel overwhelming, but it’s manageable if you break it down. Start with the non-negotiable visa requirements, then add features that fit your expat lifestyle.

This approach ensures you meet the legal requirements first, then you can customize the plan to your specific needs. It’s like buying a car: first, you ensure it’s road-legal; then you choose the features that make it perfect for you.

Decoding the Visa Non-Negotiables for Expats

For nearly every non-EU expat applying for residency, the Spanish government has a strict insurance checklist. These are the “road-legal” requirements. Miss one, and your visa application will be rejected.

Your expat plan must offer:

- Complete Coverage in Spain: It must cover everything the public system does, including GP visits, specialist care, surgery, and hospitalization.

- No Co-payments (Sin Copagos): The insurer must pay 100% of covered medical costs. You cannot pay anything out-of-pocket for services.

- Zero Deductibles: The policy must cover you from the first euro, with no initial amount to pay yourself.

- Repatriation Clause: The policy must cover medical evacuation to your home country and, if necessary, the repatriation of remains.

Any plan that fails to meet these four criteria is unsuitable for a Spanish residency application. Be cautious of cheap plans, as they often fall short, particularly on the sin copagos rule.

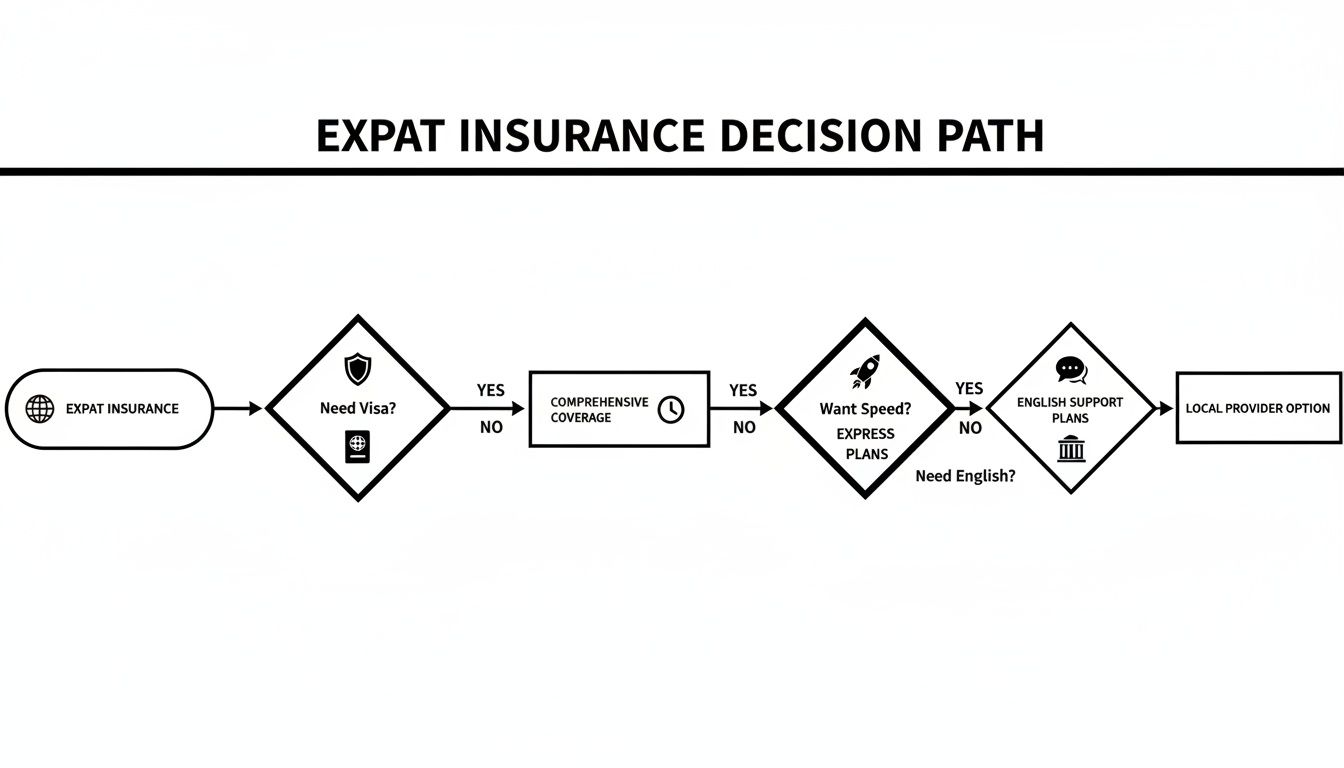

This chart can help guide your initial decisions as an expat.

As the flowchart shows, your visa status, need for rapid access, and requirement for English-speaking support are key factors that will steer you toward either a local Spanish plan or a global expat one.

Matching a Policy to Your Expat Lifestyle

Once the visa essentials are covered, consider your lifestyle. The ideal policy for a retiree in Andalusia will differ from that of a digital nomad exploring Europe from a base in Barcelona.

Consider these factors:

- Inpatient vs. Outpatient Needs: Do you need coverage for major emergencies and hospital stays (inpatient), or also for regular check-ups and tests (outpatient)? Most comprehensive expat plans cover both.

- Dental and Vision Options: Standard health policies rarely include significant dental or vision care. If you need more than basic services, look for plans with optional add-on packages.

- Global Coverage: If you travel frequently outside Spain, a local policy is insufficient. A global medical insurance plan is essential for digital nomads and frequent travelers, providing coverage wherever you are.

Real-World Expat Scenarios: Local vs. Global Insurers

Let’s look at how different expats might choose their Spain medical insurance.

Meet Maria, the Retiree in Valencia

Maria is moving to Spain full-time and plans to travel minimally. Her priority is excellent local care with English-speaking doctors. A top-tier local Spanish insurer like Sanitas or Adeslas is a perfect fit. It meets all visa requirements and provides access to a vast network of private clinics in Spain at a competitive price.

Meet Tom, the Digital Nomad in Madrid

Tom works remotely and will spend much of the year traveling. A local Spanish plan won’t cover him outside the country. He needs a global health insurance plan. While more expensive, it offers seamless coverage whether he’s in Madrid, Lisbon, or Bangkok.

Meet the Smiths, a Family in Barcelona

The Smiths have two young children and may have more. They need excellent maternity coverage, pediatric care, and a strong network of family-friendly clinics. They should seek a plan—local or global—that highlights its strong family and maternity benefits, even if it costs more.

Spain’s healthcare is world-class and offers incredible value. In 2023, its healthcare spending reached €138 billion, yet per-person spending remains efficient. With just 4.0% of household consumption going to health, the system delivers outstanding results. You can find more insights on European healthcare spending at Eurostat.

Choosing the right plan involves balancing cost, coverage, and convenience. By weighing your personal needs against policy offerings, you’ll find the perfect match. For a broader look, see our guide on how to choose the right expat medical insurance by country.

Putting Your Insurance Plan into Action

You’ve selected a policy that meets both visa requirements and your personal needs. So, what’s next? Activating and using your insurance is a straightforward process for most expats in Spain. Knowing what to expect makes it simple.

Enrollment is typically smooth. After choosing your plan, you’ll submit a few basic documents. While requirements vary by provider, you’ll likely need:

- A copy of your passport.

- Your Spanish Foreigner’s Identity Number (NIE), if available.

- Proof of your address in Spain (your empadronamiento) or your intended address.

- Your bank details for premium payments.

Once approved, you’ll receive your policy documents and an insurance card (digital or physical). This card is your key to the private healthcare network. It’s wise to understand the importance of health insurance documents and keep them organized.

Finding a Doctor and Booking Appointments as an Expat

Your first step is finding a doctor. Most insurers offer an online portal or mobile app with a provider directory (cuadro médico). Here, you can search for doctors and hospitals, filtering by location, specialty, and—crucially for many expats—language.

Booking is usually as simple as calling the clinic directly. Provide your insurance details and policy number. A major perk of private insurance in Spain is the ability to book specialist appointments directly, without a GP referral, saving significant time.

When you arrive for your appointment, you’ll just need your insurance card and an ID, like your passport or TIE. The clinic handles billing directly with your insurer, making the process seamless for you.

Understanding Direct Billing vs. Reimbursement

Understanding how bills are paid is essential to avoid surprises. With Spain medical insurance, you’ll typically encounter two models: direct billing or reimbursement.

Direct Billing (Asistencia Sanitaria)

This is the standard and most convenient method in Spain. Your insurer has agreements with a network of providers. You show your card, receive care, and the provider bills the insurer directly. For covered services, you pay zero out-of-pocket.

Reimbursement (Reembolso)

This model offers more freedom, allowing you to see any doctor, even those outside the network. With a reimbursement plan, you pay the bill upfront, get a detailed invoice (factura), and file a claim with your insurer for a refund. While flexible, it requires more paperwork and a temporary out-of-pocket expense. This is also how most international policies work for care outside Spain.

Clarifying this distinction from the start ensures a smooth healthcare experience. For worst-case scenarios requiring transport, it’s worth understanding how Medical Evacuation Insurance can fill critical coverage gaps.

Common Insurance Mistakes Expats Make (And How to Avoid Them)

You can save yourself significant trouble by learning from the common mistakes other expats make with their Spain medical insurance. A few avoidable errors are responsible for countless visa rejections and unexpected medical bills. Knowing what not to do is as important as knowing what to do.

The single biggest mistake expats make is buying a cheap travel insurance policy, believing it will suffice for residency. Spanish consulates are extremely strict: travel insurance is for short-term trips, not for the comprehensive, year-round coverage required for a residency visa. This error is a top reason for visa denials.

Mistake 1: Choosing a Plan with Co-payments

Many local Spanish insurance plans seem attractive with their low monthly premiums, which are achieved by including copagos (co-payments). This means you pay a small fee for each doctor’s visit or test. While a great option for long-term residents looking to save money, it is a fatal flaw for nearly all Spanish visa applications.

- Don’t do this: Never choose a policy with co-payments for your visa application, no matter how low the monthly price is.

- Do this instead: Ensure your plan is explicitly “sin copagos” (without co-payments). This guarantees the policy covers 100% of costs, a non-negotiable visa requirement.

Mistake 2: Overlooking Repatriation Coverage

The repatriation clause is a detail that many expats overlook, but it’s a deal-breaker for visa applications. Spanish authorities require assurance that if the worst happens, your insurance will cover the full cost of returning you or your remains to your home country.

Failing to ensure your policy includes full coverage for both medical evacuation and the repatriation of remains is an automatic red flag for visa officials. This isn’t an optional add-on; it’s a core requirement of a compliant policy.

Mistake 3: Ignoring Waiting Periods and Pre-existing Conditions

Many expats assume their new insurance covers everything from day one. However, many plans have waiting periods (periodos de carencia) for certain treatments, like non-emergency surgery. While a good visa-compliant plan will have these waived, you must confirm this.

Similarly, not being transparent about pre-existing conditions is a major risk. Hiding your medical history can lead to claim denials just when you need coverage the most.

- Don’t do this: Don’t assume all services are covered immediately, and never hide your medical history.

- Do this instead: Work with an insurance specialist who can find a policy that meets visa rules by eliminating waiting periods. Always declare any pre-existing conditions to ensure your coverage is solid.

Answering Your Top Questions About Spain Medical Insurance

Let’s address some of the most common questions expats have about Spain medical insurance. Getting these details right is crucial for a smooth and successful move.

Here is a quick-reference guide to help you avoid common pitfalls.

“Can I Just Use Travel Insurance for My Spanish Residency Visa?”

The answer is an emphatic no. This is the most frequent mistake expats make, and it results in an automatic visa rejection. Spanish consulates require a proper, long-term private health insurance policy that mirrors the public system’s coverage.

Travel insurance is designed for short-term emergencies and lacks the key features demanded for residency:

- Comprehensive coverage for all medical needs, not just accidents.

- Zero co-payments (sin copagos) and no deductibles.

- A mandatory repatriation clause.

“How Much Should I Expect to Pay for Expat Medical Insurance?”

The cost varies based on age, health, and the level of coverage. As a general guide, a young, healthy expat can find a basic visa-compliant plan starting from €50–€70 per month.

For older expats, families, or those wanting more comprehensive benefits, premiums are more likely to be in the €100 to over €300 monthly range. Global plans that provide worldwide coverage will be at the higher end of this scale, but offer invaluable flexibility for frequent travelers.

“If I Qualify for Public Healthcare, Do I Still Need a Private Plan?”

Legally, no. However, many expats who gain access to the public SNS choose to keep their private plan. They use it not as a replacement, but as a supplement to get the best of both worlds.

A private policy acts as a fast-pass, allowing you to bypass the public system’s potential waiting lists for specialists. It also ensures access to English-speaking doctors and the comfort of a private hospital room, providing significant peace of mind for expats.

“What Exactly is ‘Sin Copagos’ and Why is it So Important for Expats?”

“Sin copagos” means “without co-payments.” For most Spanish residency visas, this is a non-negotiable requirement. It means your insurance policy must cover 100% of the cost for any medical service, with no out-of-pocket fees for you.

The Spanish government mandates this to ensure new residents are financially self-sufficient and will not burden the public healthcare system. A sin copagos plan is proof that you can fully cover your own medical costs.

Feeling more confident but still want an expert to guide you? The world of Spain medical insurance can be complex, but you don’t have to navigate it alone. The team at Expat Global Medical specializes in finding the perfect visa-compliant plan that fits the needs and budget of expats like you.

Get Your Free Quote from Expat Global Medical today and take the guesswork out of your Spanish adventure.