")

If you’re planning a long-term move to Mexico, your standard travel insurance policy just won’t cut it. To truly settle in and live with peace of mind, a dedicated expat medical insurance plan is essential. Think of it this way: travel insurance is for tourists and emergencies, but a proper expat plan is for residents who need real, everyday healthcare access.

Why Expat Health Insurance in Mexico Is a Non-Negotiable

Picture this: you’ve finally retired to that sunny beach town you’ve dreamed of, but a sudden medical issue sends you to the hospital. It’s a common fear, and for good reason. Too many expats assume their health plan from back home or a cheap travel policy will cover them. The hard truth is, those plans are designed to patch you up and get you on the next flight home—not to manage your health while you build a new life abroad.

This simple oversight can turn into a massive financial and medical nightmare. The real difference is in the scope of coverage. Expat medical insurance acts as your primary healthcare partner. It’s there for the routine check-ups, the management of chronic conditions, and specialist visits—all the things travel insurance almost never touches. It’s your golden ticket to Mexico’s top-notch private healthcare system without liquidating your savings. You can get a clearer picture of these limitations by reading why U.S. health insurance doesn’t work abroad.

Understanding Mexico’s Healthcare Landscape

In recent years, having solid private insurance has become more critical than ever. Mexico had made huge strides in getting its population insured, but recent policy changes have unfortunately walked back some of that progress. After a key public health program was dismantled, the number of uninsured people in Mexico shot up to 29.1% by 2023.

This shift highlights just how unreliable public options can be for non-citizens, making a private International Health Insurance plan an absolute must-have for securing quality, consistent care.

A dedicated expat plan isn’t a luxury; it’s a fundamental part of a secure and sustainable life in Mexico. It provides access to top-tier private hospitals and English-speaking doctors, ensuring you receive high-quality care without facing crippling out-of-pocket costs.

To help you see the options more clearly, here’s a quick breakdown of what’s available.

Your Mexico Health Coverage Options at a Glance

This table simplifies the main choices for foreigners in Mexico. As you’ll see, for anyone staying longer than a few months, an expat plan is the only one that truly covers all the bases.

| Coverage Type | Ideal For | Primary Limitation |

|---|---|---|

| Travel Insurance | Short trips, vacations (under 90 days) | Covers emergencies only; no routine care. |

| Home Country Plan | U.S. residents (almost never works abroad) | Extremely limited or no coverage outside the U.S. |

| Mexican Public (IMSS) | Legal residents with CURP | Can have long waits and inconsistent quality. |

| Expat Medical Insurance | Long-term residents, retirees, digital nomads | Higher premium, but offers comprehensive care. |

Ultimately, choosing the right insurance boils down to matching your coverage to your lifestyle. The needs of a one-week vacationer are worlds apart from someone retiring or working remotely for a year or more. A robust expat plan ensures your health and finances are protected, so you can focus on enjoying everything Mexico has to offer.

Vacation Coverage vs. Expat Medical Insurance

Picking the right insurance for Mexico isn’t just about ticking a box; it’s about matching your coverage to your actual life. One of the biggest mistakes people make is confusing a short-term travel policy with a long-term expat plan. Getting this wrong can leave you with massive coverage gaps and even bigger bills.

The easiest way to think about it is with a simple analogy: standard travel insurance is like a first-aid kit. It’s built for sudden, unexpected emergencies—a nasty bout of food poisoning, a broken bone from a fall, or a last-minute trip cancellation. Its job is to patch you up, stabilize the situation, and, if things are really serious, get you back home for proper care. It’s perfect for a week in Tulum, but totally wrong for someone putting down roots.

On the flip side, expat medical insurance is your full-time healthcare plan. This is the kind of comprehensive coverage you’d have back home. It’s designed for the long haul, covering not just accidents but also the routine, day-to-day health needs that come with living somewhere. If Mexico is your new home base—whether you’re retiring, working remotely, or starting a new chapter—this is what you need.

What Expat Insurance Covers That Travel Insurance Doesn’t

The real difference shines through when you look at what each policy is actually designed to do. While your travel plan is waiting for an emergency, an expat plan is there to provide a much wider safety net for your overall health.

Here’s where they part ways:

- Routine and Preventive Care: Expat plans are built to cover things like annual physicals, wellness screenings, and vaccinations. A travel policy won’t touch these.

- Chronic Condition Management: If you manage a condition like diabetes or high blood pressure, an expat plan covers your specialist appointments and prescriptions. Travel insurance is strictly for brand-new, unforeseen issues.

- Specialist Consultations: Need to see a dermatologist for a nagging rash or a physical therapist for a sore back? An expat policy covers these routine visits. A travel plan only covers specialists if it’s tied to a sudden, acute emergency.

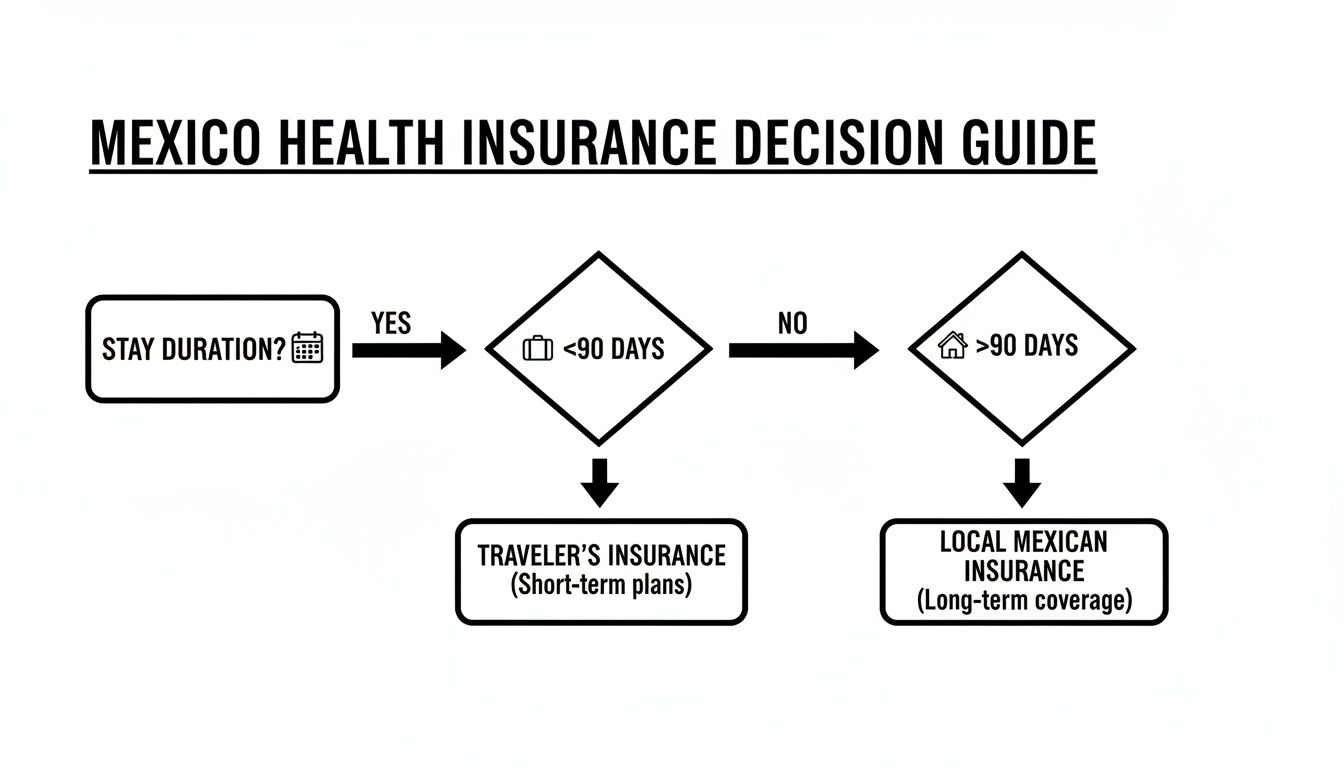

This simple decision tree can help you see which path makes sense for you.

As the chart shows, it really boils down to one thing: how long you’re staying. That’s the key factor that determines the kind of coverage you absolutely need.

Real-World Scenarios: A Sprained Ankle vs. Ongoing Therapy

Let’s put this into practice to see just how wide the gap is between these two types of insurance.

Scenario 1: The Vacationer’s Sprained Ankle

A tourist on a 10-day trip to Cancún takes a wrong step on a cobblestone street and badly sprains their ankle. Their travel insurance kicks right in. It covers the emergency room visit, the X-ray to check for fractures, and the cost of a brace. The policy did its job perfectly by handling an acute, one-off injury.

Scenario 2: The Retiree’s Physical Therapy

Now, picture a retiree living in San Miguel de Allende who needs physical therapy twice a week to manage their arthritis. Their expat medical insurance covers every single one of those appointments because it’s designed for long-term health management. A travel policy would deny these claims in a heartbeat—they aren’t sudden, and they certainly aren’t an emergency.

The core takeaway is simple: Travel insurance is for visiting a country. Expat medical insurance is for living in a country. One is for accidents, the other is for your actual health and well-being.

Getting this distinction right is the first and most important step toward getting the right expat medical insurance in Mexico. For anyone planning to stay longer than 90 days, a proper expat medical plan isn’t just a nice-to-have; it’s essential for a secure and healthy life abroad.

Navigating Mexico’s Public and Private Healthcare Systems

When you’re settling in as an expat or long-term resident in Mexico, you’ll quickly discover the healthcare system runs on two very different tracks. I like to think of it as choosing between a public bus and a private taxi. Both will get you where you need to go, but the journey itself—in terms of speed, comfort, and cost—couldn’t be more different. Grasping this distinction is the key to understanding why solid expat medical insurance in Mexico isn’t just a nice-to-have; it’s your ticket to the best possible care.

First, there’s the public system, which is mainly run by the Instituto Mexicano del Seguro Social (IMSS). While legal residents can access it, foreigners often run into some pretty significant roadblocks. It’s common to hear expats talk about the long, frustrating wait times for appointments and procedures, facilities that feel perpetually overcrowded, and the constant language barrier if your Spanish isn’t up to snuff.

And it’s not just about the system’s structure. A huge part of the challenge involves overcoming healthcare communication barriers, which can turn an already stressful medical issue into a truly overwhelming experience.

The Appeal of Mexico’s Private Healthcare

Then you have the other track: Mexico’s private healthcare system. This is a completely different world and where the country’s reputation for excellent medical care really comes from. Private hospitals and clinics here are genuinely impressive, with modern facilities, top-tier specialists, and plenty of English-speaking doctors.

For many expats, the standard of care is on par with—or even better than—what they’re used to back home. The difference is night and day:

- Immediate Access: You can usually see a specialist within a few days, not a few months.

- High-Quality Facilities: Think modern technology, sparkling clean hallways, and comfortable private rooms.

- English-Speaking Staff: Communication is rarely a problem, from the doctors right down to the administrative team.

Of course, this level of quality comes with a price tag. While it’s still generally more affordable than U.S. healthcare, the costs in Mexico’s private system can add up quickly, especially for anything serious. A major surgery or an extended hospital stay paid out-of-pocket could easily set you back tens of thousands of dollars.

Your Insurance Is the Key to Access

This is precisely where your expat medical insurance plan becomes your most valuable tool. It’s your all-access pass to this premier private system, turning a potentially bank-breaking expense into something you can actually manage. Let’s be honest: without good insurance, the private system is a luxury few can afford when a real emergency strikes.

A comprehensive expat medical plan is designed to bridge that financial gap. It gives you the freedom to choose the best doctors and the best hospitals, right when you need them, without having to drain your savings.

More and more people are catching on. Mexico’s travel insurance market recently hit USD 650.21 million and is projected to soar to USD 1,192.11 million by 2033. This boom is being driven by expats and long-term visitors who get it—private coverage is essential when the public options come with so many limitations, especially for foreigners.

Ultimately, the healthcare path you choose will have a massive impact on your life in Mexico. While the public system is there, it’s the private network that delivers the peace of mind and quality of care most expats are looking for. To dig deeper, you can explore our detailed comparison of private vs. public healthcare for expats. Having the right insurance plan simply ensures this superior care is always within reach.

Must-Have Features in Your Expat Insurance Plan

Picking the right expat health insurance isn’t about snagging the lowest price—it’s about locking in a plan with the right features to truly protect you in a new country. Once you look past the price tag, you’ll find there are several non-negotiable elements every solid expat medical insurance mexico plan has to include. Think of these as the backbone of your medical security, giving you the confidence to handle anything from a routine check-up to a serious emergency.

Knowing what to look for helps you evaluate policies like a pro. Each of these features is critical for a specific reason, directly impacting your access to quality care and your financial stability while living in Mexico.

High Coverage Limits for Major Medical Events

Probably the most critical piece of any expat plan is a high overall coverage limit. This is your total safety net. While a minor illness might only set you back a few hundred dollars, a serious accident or an unexpected surgery can spiral into tens or even hundreds of thousands of dollars, even within Mexico’s more affordable private healthcare system.

A low limit might look tempting when you’re trying to save on premiums, but it leaves you dangerously exposed. A good rule of thumb is to look for plans with at least $1,000,000 USD in annual coverage. That figure ensures a catastrophic event won’t bankrupt you, covering everything from an ICU stay to complex surgeries without you having to sweat about hitting your cap.

Comprehensive Inpatient and Outpatient Care

A truly great expat plan does more than just cover disasters; it supports your day-to-day health. This is where understanding the difference between inpatient and outpatient coverage becomes so important.

- Inpatient Care: This is anything that requires you to be formally admitted to a hospital. It covers your room, surgeries, nursing care, and any medications they give you during your stay.

- Outpatient Care: This bucket holds everything else—all the medical services that don’t need a hospital stay. We’re talking doctor’s appointments, specialist visits, diagnostic tests like X-rays and blood work, and prescription medications you pick up from the pharmacy.

For anyone living abroad long-term, solid outpatient benefits are a must. They let you manage your health proactively, see a doctor when you feel off, and tackle minor issues before they snowball into major ones. Without it, you’d be paying out-of-pocket for every single consultation.

A Strong Direct Billing Network

Picture this: you’re in the midst of a medical emergency, and the hospital asks you to pay $20,000 upfront before they’ll even admit you. It sounds like a nightmare, but it’s a real possibility at many private facilities if your insurer doesn’t have a direct billing (or “cashless”) agreement set up.

Direct billing simply means the hospital sends the invoice straight to your insurance company. You just handle your deductible or copay, not the entire, staggering cost of treatment.

Before you commit to a plan, always check the insurer’s network of hospitals in Mexico—especially in the city or town where you plan to live. A plan with a strong direct billing network is what stops a medical crisis from becoming an instant financial one.

Emergency Medical Evacuation and Repatriation

So, what happens if you’re living in a smaller town like Ajijic or a remote beach community and something serious happens that the local clinic just can’t handle? This is where medical evacuation coverage becomes a literal lifesaver. This benefit covers the cost of getting you to the nearest hospital that can provide the level of care you need.

That could mean an ambulance to a major hospital in Guadalajara or Mexico City. In extreme cases, it could even mean an air ambulance back to your home country. These services are incredibly expensive, often topping $50,000. Without this coverage, you could be stuck in an under-equipped facility or face an impossible bill. On a related note, repatriation of remains is a sensitive but practical feature that covers the cost of returning a deceased person home.

The demand for these robust features is on the rise. Market analysis shows steady growth in Mexico’s health insurance sector, largely driven by expats who want plans that cover everything from dental and vision to pre-existing conditions. This trend signals a clear shift toward policies built for living abroad, not just visiting. To see the data behind this market evolution, you can explore the latest findings on Mexico’s health insurance industry.

Understanding the Costs and Common Exclusions

Once you start shopping for expat medical insurance in Mexico, the conversation quickly shifts to two things: how much it costs and what’s hidden in the fine print. Honestly, understanding how your premium is calculated and what your plan won’t cover is just as vital as knowing what it will. Think of this knowledge as your best defense against surprise medical bills. It’s what allows you to pick a policy with total confidence.

Just like car insurance, the price of your expat medical plan isn’t random. A few key factors shape what you’ll pay, with the biggest drivers being your age, your deductible, and how wide you want your coverage area to be.

Decoding Your Insurance Premium

The cost is really a reflection of risk and personal choice. For instance, an older applicant will almost always pay a higher premium than a younger one, and that’s simply because the statistical likelihood of needing medical care increases with age.

Your deductible—the amount you agree to pay out-of-pocket before your insurance starts paying—is another huge piece of the puzzle. If you choose a higher deductible, you’re taking on more of the initial financial risk, which brings your monthly premium down. On the flip side, a lower deductible means you pay less upfront for care, but your monthly premium will be higher. It’s a bit like a seesaw: as one side goes up, the other comes down, helping you find the perfect balance for your budget. To really get into the weeds on this, you can learn more about how international health insurance cost is determined and what kind of numbers to expect.

Tackling Common Policy Exclusions

Every single insurance policy on the market has a list of exclusions—specific situations or conditions it just won’t pay for. Insurers aren’t trying to pull a fast one; these exclusions are necessary to keep plans from becoming outrageously expensive and to manage their overall risk. The key is to know them upfront to avoid any major headaches down the road.

Here are the most common things you’ll see on that “not covered” list:

- Pre-existing Conditions: This is the big one. Most plans will define a pre-existing condition as any medical issue you sought treatment or advice for before your policy kicked in. Some plans might exclude these conditions permanently, while others may agree to cover them after a waiting period of, say, 24 months.

- Elective and Cosmetic Procedures: Any treatments that aren’t medically necessary, like plastic surgery or other cosmetic work, are almost universally excluded.

- High-Risk Activities: Planning on a life of adventure in Mexico? If your hobbies include things like scuba diving, rock climbing, or paragliding, you’ll likely need to buy an extra “rider” to cover potential injuries. Standard plans typically steer clear of these activities.

- Drug or Alcohol-Related Incidents: Injuries or illnesses that are a direct result of being under the influence of drugs or alcohol are a standard exclusion across the board.

Knowing your policy’s exclusions isn’t just about avoiding a denied claim—it’s about truly understanding the boundaries of your financial protection. Carving out time to carefully read this section of your policy document is one of the smartest things you can do.

By balancing the factors that drive your premium and getting crystal clear on what’s left out, you can land on a plan that gives you solid protection without any nasty surprises. That transparency is what will let you make a secure, informed decision for your health and well-being in Mexico.

How to Choose and Purchase Your Health Insurance

Knowing you need a real expat health plan is one thing; actually picking one and getting it set up is another. The whole process of choosing the right expat medical insurance in Mexico can feel a bit overwhelming, but it really just breaks down into a few manageable steps. Let’s walk through how to turn your research into a decision, making sure you end up with a policy that genuinely fits your life here.

It all starts with an honest look at your own situation. Think about your current health, any chronic conditions you manage, the kind of lifestyle you’ll have in Mexico, and what your budget can handle. Are you an active retiree who might need solid coverage for joint issues down the road? Or a digital nomad who just wants a strong safety net for a true emergency? A frank self-assessment is the best place to begin.

Once you have a clear picture, you can start gathering and comparing quotes from reputable providers. It’s tempting to just grab the cheapest one, but that’s rarely a good idea. Dig into the details of what each plan offers, because a slightly lower premium might hide a much higher deductible or skimpy outpatient benefits.

Assessing Providers and Hospital Networks

A great insurance plan is only as good as the hospitals and clinics that actually accept it. Before you sign anything, do a little homework on the insurer’s network, especially in the city or region you plan to call home. You want to see strong partnerships with top-tier private facilities.

This is especially critical when it comes to direct billing. A solid network means you won’t have to fork over tens of thousands of dollars out of pocket during a medical crisis and wait for reimbursement. You can almost always find a provider directory on the insurer’s website, or you can just ask them for a list of affiliated hospitals in your area.

The Importance of Full Disclosure

When you get to the application, being completely upfront and honest is non-negotiable. It can be tempting to downplay or even leave out a past health issue to try and snag a lower premium, but trust me, this is a huge mistake.

Insurers have a process called underwriting where they carefully review your medical history. If you fail to disclose a pre-existing condition and later file a claim related to it, the insurer has every right to deny that claim—and could even cancel your policy outright. Full transparency from day one ensures your coverage will actually be there when you need it most.

Reading your policy documents isn’t just a casual suggestion—it’s absolutely essential. This is your contract. It spells out every benefit, every limit, and every exclusion. You need to carve out some time to really understand it before you sign on the dotted line.

Working with a Specialist Broker

Let’s face it, navigating the world of international insurance can get complicated fast. This is where an experienced broker who specializes in expat medical plans can be a lifesaver. A good broker isn’t just a salesperson; they’re your advocate.

Here’s how they can help:

- Personalized Advice: They’ll take the time to understand your unique needs and then recommend plans from multiple insurance companies that are the best fit for you.

- Market Knowledge: They live and breathe this stuff. They understand the subtle differences between policies and can explain complex insurance jargon in plain English.

- Application Support: They’ll guide you through the application from start to finish, making sure everything is filled out correctly to avoid any hiccups later on.

In the end, a broker does more than just sell you a policy. They provide expert guidance to help you make a truly informed decision, turning what feels like a complicated chore into a clear path toward securing your health and peace of mind in Mexico.

Got Questions About Expat Health Insurance? We Have Answers.

It’s only natural to have a few questions floating around as you navigate the world of expat medical insurance. Let’s tackle some of the most common ones we hear from folks planning their move to Mexico, so you can feel confident you’ve got all your bases covered.

Can I Just Use My U.S. Medicare Plan in Mexico?

The short answer is a hard no. U.S. Medicare offers practically zero coverage once you cross the border, so you should never, ever rely on it for your healthcare needs while living in Mexico. This is exactly why getting a dedicated expat medical insurance plan in Mexico isn’t just a good idea—it’s absolutely essential for protecting both your health and your wallet.

Is It Too Late to Buy Insurance if I’ve Already Moved to Mexico?

Technically, yes, you can usually buy a plan after you’ve already arrived. But honestly, we can’t recommend this approach. It’s much smarter to get your coverage locked in before you move.

Doing it this way means you’re protected from the moment your feet hit the ground. You’ll sidestep any frustrating waiting periods or unexpected hitches that might pop up while you’re trying to get settled in a new country. It’s all about making sure that safety net is in place from day one.

The best strategy is to have your insurance sorted out before you land. Arriving with a policy in hand means you can immediately access Mexico’s private healthcare system if an unexpected illness or accident occurs.

What Does “Medical Evacuation” Coverage Actually Do?

Think of medical evacuation as your ultimate emergency transport plan. If you suffer a serious illness or injury and the local facility can’t provide the care you need, this benefit kicks in. It arranges and pays to get you to the nearest hospital that can handle your situation.

For instance, if you’re in a remote beach town, this could mean an air ambulance to a top-tier hospital in Mexico City. In extreme cases, it could even mean a flight back to your home country for highly specialized care. This is a huge deal, as evacuation costs can easily rocket past $50,000, turning a medical crisis into a life-altering financial disaster.

Here’s what it handles:

- Logistics: The insurer’s assistance team coordinates all the complex transportation details.

- High Costs: It foots the bill for incredibly expensive services like air ambulances.

- Access to Proper Care: It ensures you get to a facility equipped to treat your specific condition.

Will My Prescription Medications Be Covered?

This is a big one, and the answer really varies from plan to plan. More basic policies might only cover medications you receive while you’re admitted to a hospital. On the other hand, a more robust expat medical plan will usually include coverage for outpatient prescription drugs.

If you have a chronic condition that requires daily or regular medication, this is something you absolutely need to verify. Always dive into the policy details to make sure the prescriptions you rely on are included.

Ready to secure your peace of mind in Mexico? At Expat Global Medical, we specialize in finding the perfect health insurance plan for your new life abroad. Get your free, no-obligation quote today and see how easy it is to protect yourself.