Think of it as the ultimate “undo button” for your expensive, non-refundable travel plans. That’s the real power behind travel insurance with Cancel For Any…

Think of it as the ultimate “undo button” for your expensive, non-refundable travel plans. That’s the real power behind travel insurance with Cancel For Any Reason cover. It’s an optional upgrade that acts as a financial safety net, paying you back a huge chunk of your prepaid trip costs if you have to cancel for any reason—even ones a standard policy won’t touch.

Your Ultimate Safety Net for Global Travel

For expats, digital nomads, and retirees living abroad, life is packed with unique variables that standard insurance just wasn’t built for. While a long-term expat medical insurance plan covers your health, it doesn’t protect the significant financial investment of your travel. Traditional trip cancellation policies are pretty rigid. They only kick in for a specific, pre-approved list of reasons, like a sudden illness or a natural disaster.

But what about all the situations that fall into the gray areas of a global lifestyle?

Beyond Standard Coverage

Cancel For Any Reason (CFAR) isn’t a standalone policy. Instead, it’s a powerful rider you add to a comprehensive travel insurance plan. Think of it as a strategic tool that gives you a level of flexibility standard coverage simply can’t match. This is especially vital for anyone whose life and career span across borders, and it complements the security provided by your primary expat medical insurance.

Just consider these common expat scenarios where a standard policy would almost certainly deny your claim:

- A long-awaited visa gets unexpectedly delayed, making your planned move impossible.

- That amazing job offer you moved for is suddenly pulled right before your start date.

- You just get a bad gut feeling about political instability brewing at your destination.

- A critical family matter back home requires your presence for an indefinite period.

In every one of these cases, CFAR lets you get back a significant portion of your non-refundable trip costs—usually between 50% to 75%. This can cover everything from international flights and accommodation deposits to prepaid tour packages. For a deeper dive into what makes a great policy, our comprehensive travel insurance guide offers some essential tips.

Protecting Your Financial Investment

For an expat, a big trip is often much more than a vacation; it’s a major life event that can involve thousands of dollars in upfront costs. Whether you’re planning a complex family reunion across continents or orchestrating a major relocation, the financial stakes are high. Your expat medical insurance protects your health, but CFAR protects the trip’s finances.

It’s particularly true when you’ve invested heavily in a once-in-a-lifetime trip, like an escape to one of the world’s best all-inclusive honeymoon resorts. The peace of mind CFAR coverage brings is invaluable.

The ability to cancel for reasons beyond your health or the weather is fundamental for anyone managing the uncertainties of an international career or retirement. CFAR protects the substantial financial investment that underpins these life-changing moves.

At the end of the day, travel insurance with Cancel For Any reason cover is all about managing risk in an unpredictable world. It gives you the freedom and confidence you need to plan those ambitious global journeys, knowing you have a reliable backstop if things have to change for any reason at all. It’s an essential piece of the puzzle for a lifestyle that demands adaptability.

How CFAR Coverage Actually Works

So, how does this ultimate travel safety net actually function? Think of travel insurance with Cancel For Any Reason cover as a high-performance tool. It’s incredibly powerful, but you have to follow the operating instructions perfectly to get the results you want.

There are three non-negotiable rules baked into every CFAR policy. They aren’t there to trip you up; they’re the framework that allows insurers to offer such flexible coverage in the first place. Get these right, and you unlock the full power of CFAR.

The Three Golden Rules of CFAR

Successfully using your CFAR coverage all comes down to timing and commitment. Insurers have to balance their risk, which means you need to follow a strict process right from the moment you start booking your trip.

Here’s exactly what you need to do:

- Purchase Promptly: You must buy your travel insurance policy with the CFAR add-on within a tight window—usually 14 to 21 days from your very first trip payment. That initial payment could be for anything: a flight deposit, a tour, a hotel. If you wait too long, you’re out of luck.

- Insure Everything: You’re required to insure 100% of your prepaid and non-refundable trip costs. No picking and choosing which parts of the trip you want to cover. The policy has to reflect the total amount of money you have on the line.

- Cancel in Advance: You have to pull the plug on your trip at least 48 hours before your scheduled departure. CFAR isn’t for last-minute decisions on the day of your flight, though you should always check your specific plan’s deadline.

Following these three steps is the only way to guarantee a successful CFAR claim. They’re designed to prevent people from buying last-minute protection only when they sense trouble, which keeps the system fair for everyone.

Why You Get 50% to 75% Back Not 100%

Here’s a detail that often surprises people: CFAR doesn’t reimburse your entire trip cost. Unlike standard trip cancellation, which can pay back up to 100% for a covered reason, CFAR typically reimburses between 50% and 75% of your insured costs.

Think of it as a shared-risk agreement between you and the insurance company. You’re asking for the ultimate flexibility to cancel for reasons that are totally personal—like a new work project or just feeling anxious about the trip. To make that financially possible, the insurer covers the majority of your loss, and you absorb the rest.

This partial reimbursement is the key that makes CFAR possible. It allows insurers to offer incredible freedom without taking on an unsustainable amount of risk, ensuring this powerful benefit remains available for travelers who truly need it.

This model is also what keeps premiums from skyrocketing. It strikes a delicate balance, giving you a substantial financial cushion for almost any scenario without covering the entire cost of a purely decision-based cancellation. While CFAR coverage can add over $300 to a standard plan, for many expats and nomads, that peace of mind is priceless. You can read more about what makes these plans a popular choice for travelers.

CFAR vs Standard Trip Cancellation A Head-To-Head Comparison

To really see the value of travel insurance with Cancel For Any Reason cover, it helps to put it side-by-side with a standard policy. The differences are stark and show you exactly what that extra premium buys you.

Here’s how they stack up.

| Feature | Standard Trip Cancellation | Cancel For Any Reason (CFAR) Cover |

|---|---|---|

| Cancellation Reasons | Limited to a specific list of covered perils (e.g., documented illness, death in the family, severe weather). | Allows cancellation for nearly any reason not covered by the standard policy, including work conflicts or personal unease. |

| Reimbursement | Up to 100% of non-refundable trip costs for a covered reason. | Typically 50% to 75% of non-refundable trip costs. |

| Purchase Window | Can often be purchased up until the day before departure. | Must be purchased within a strict 14-21 day window of the initial trip payment. |

| Cancellation Deadline | Depends on the specific covered event. | Must cancel at least 48 hours prior to the scheduled departure time. |

As the table shows, with CFAR, you’re essentially trading a higher reimbursement percentage for near-total freedom in your decision to cancel. For expats, digital nomads, and retirees whose lives are often unpredictable, that’s a trade-off that makes perfect sense.

Why Expats and Digital Nomads Actually Need CFAR

For anyone living a global life, “standard” is a word that rarely applies. While a robust expat medical insurance plan is essential for your long-term health, it won’t protect your travel investments. Your plans are often expensive, booked far in advance, and can unravel for reasons a normal policy would never recognize.

This is where travel insurance with Cancel For Any Reason cover stops being just another add-on. It becomes an essential tool for managing a life lived across borders, giving you a crucial financial safety net for the kind of professional, personal, and bureaucratic curveballs you’re bound to face.

Navigating Career and Visa Uncertainties

Picture this: You’ve just landed a dream job overseas. You’ve already paid for non-refundable flights, booked a month of temporary housing, and arranged to ship your belongings. Then, a few weeks before your departure, the company pulls the plug on the offer because of an internal shake-up. A standard policy is useless here—a lost job offer isn’t a covered reason.

With CFAR, that devastating financial hit gets a lot softer. You can cancel everything and get back a huge chunk—up to 75%—of your prepaid expenses. The same logic applies to other all-too-common expat headaches:

- Sudden Visa Delays: Your visa gets tangled up in bureaucratic red tape, making your planned arrival date totally impossible.

- Failed Work Permits: Despite all assurances, your work permit application is denied at the eleventh hour.

- Changing Business Needs: You’re a freelance digital nomad, and a major client at your destination suddenly cancels a project, making the whole trip financially pointless.

In any of these scenarios, CFAR gives you the power to make the right call for your career and finances without losing your entire investment. It’s a vital shield against the volatile nature of international work and immigration. For a lifestyle that demands flexibility, our guide to digital nomad health insurance offers more ideas for building a solid safety net.

Managing Complex Personal Situations

An expat’s life is also full of unique personal duties that can force a sudden change of plans. Standard policies might cover you if a close family member has a medical emergency, but what happens when life gets more complicated?

CFAR is designed for the gray areas of life that don’t fit into a tidy insurance box. It’s for the ‘just in case’ moments that are incredibly common in the complex lives of global citizens.

Think about a situation where an aging parent back home isn’t critically ill, but they start needing more consistent care, and you feel you need to be there for them. Or maybe a relationship with the partner you planned to move abroad with comes to an unexpected end. These are legitimate, life-altering reasons to cancel a big move, but they are never covered by standard insurance. Travel insurance with Cancel For Any Reason cover gives you the freedom to put your family and your well-being first.

Growing anxiety among travelers, fueled by everything from political instability to chaos at airports, has made standard policies feel pretty flimsy for many. This has led to a major spike in people buying CFAR, as they look for more control over their plans. For an expat, that control isn’t a luxury—it’s a necessity for managing a life packed with unpredictable variables.

Calculating the Cost of Total Flexibility

The ultimate freedom to change your plans comes with a price tag, which brings us to the big question for any expat or digital nomad: is travel insurance with Cancel For Any Reason cover actually worth the extra cash?

The short answer is, it depends on a simple cost-benefit analysis. Once you run the numbers, you can decide with confidence whether that higher premium is a smart investment or an unnecessary expense for your specific journey.

At its heart, CFAR is an investment in managing risk. You’re paying more to hand over a big chunk of your financial exposure—the kind that comes from a sudden change of heart or situations that a standard policy won’t touch—to your insurer. The cost for this level of flexibility is pretty consistent across the board.

Breaking Down the Premium

Adding a CFAR rider to a standard travel insurance policy will typically bump up your premium by 40% to 50%. Now, that percentage might sound steep, but let’s put it into real-world dollars. If a comprehensive policy for your trip costs $400, tacking on CFAR might bring the total to somewhere between $560 and $600.

That extra cost buys you the power to cancel for reasons that could otherwise leave you thousands of dollars out of pocket. Think of it as a calculated expense designed to shield you from a much larger, and potentially devastating, financial hit. Getting a handle on insurance costs is key for expats, and you can dive deeper by checking out our international medical insurance cost guide.

The Cost-Benefit Scenario: An Expat Example

To see if CFAR makes financial sense, you have to weigh the premium against your total non-refundable expenses. Let’s walk through a realistic scenario for an expat relocating for a new job.

Imagine your total prepaid, non-refundable costs add up to $15,000. This includes things like:

- One-way international business class flights: $6,000

- First month’s rent and security deposit on an apartment: $5,000

- Prepaid international moving service: $4,000

Let’s say your standard travel insurance policy is $1,000. Adding CFAR at a 50% premium increase brings your total insurance cost to $1,500. A few weeks before your move, you get a much better job offer in a different country and decide to change plans.

Without CFAR, that decision would cost you the full $15,000. With CFAR, you file a claim and get a 75% reimbursement, which works out to $11,250. Your net loss is only $3,750, plus the $1,500 premium you paid.

In this case, spending an extra $500 on the CFAR rider saved you $9,750. It’s easy to see why it made sense here.

The market for this type of coverage is booming for a reason. The global CFAR travel insurance market is projected to skyrocket to USD 95.5 billion by 2031, fueled by a growing awareness of travel risks among consumers. This growth shows just how much travelers value security, justifying premiums that are 40-50% higher than basic plans for those who need that no-questions-asked peace of mind. You can discover more insights about the growing CFAR market.

Ultimately, the decision boils down to your personal risk tolerance and what’s financially at stake for your trip. By comparing your non-refundable costs against the premium, you can make a smart, informed choice that protects both your wallet and your peace of mind.

Getting to Grips with Your CFAR Policy’s Fine Print

It’s one thing to know that travel insurance with Cancel For Any Reason cover exists; it’s another to master how it actually works. To really get the most out of this flexible upgrade, you have to understand its specific rules and how it plays with your main policy. Getting this part wrong is a classic mistake that can lead to denied claims and a lot of frustration.

First things first: CFAR is always an optional upgrade. You can’t just go out and buy a standalone CFAR policy. It’s a rider that enhances a comprehensive travel insurance plan, which should also include essential medical emergency coverage that works alongside your main expat medical insurance plan for short-term travel incidents.

This distinction is absolutely critical because it dictates how you should file a claim. You essentially have two different paths for getting your money back if you cancel a trip, and picking the right one makes a huge difference to your wallet.

Standard Cancellation vs. CFAR: Knowing Which Lever to Pull

Picture this: you have to cancel an expensive, non-refundable trip two weeks before you’re supposed to leave. The reason you’re canceling determines which part of your policy to use. This is where so many travelers trip up and leave a ton of money on the table.

Let’s say you have an unexpected, documented medical emergency that makes travel impossible.

- The Smart Path (Standard Policy): You’d file a claim under your standard trip cancellation benefit. A medical emergency is a classic “covered reason” listed in just about every policy. By going this route and providing the right paperwork, you could get up to 100% reimbursement for your non-refundable costs.

- The Costly Mistake (CFAR Path): If you jumped the gun and filed under your CFAR benefit instead, you’d only get 50% to 75% back. You would have thrown away a significant chunk of your refund simply by using the wrong tool for the job.

The rule of thumb is simple: if your reason for canceling is already covered by your standard policy, always use that path. It maximizes your refund. Save your CFAR benefit for what it was designed for—all the reasons not on that list, like a sudden work conflict, a breakup, or just a gut feeling that it’s not the right time to go.

The Three Unbreakable Rules of CFAR

Beyond knowing when to use it, you absolutely must follow the strict operational rules of CFAR. These aren’t just suggestions; they are non-negotiable requirements. Fail to meet them, and your claim will be denied.

Here are the three big ones to burn into your memory:

- The Clock is Ticking: You have a very small window to add the CFAR upgrade to your plan—usually just 14 to 21 days after making your first payment for the trip.

- Cancel Well in Advance: You must officially cancel your trip with all your travel providers at least 48 hours before you were scheduled to depart. No last-minute changes of heart will be covered.

- It’s Not a Full Refund: You will never get 100% back with a CFAR claim. It’s designed to soften the blow, not erase it completely. Expect a reimbursement of 50% to 75% of your insured, non-refundable trip costs.

By understanding that CFAR is a specialized upgrade, knowing when your standard coverage is the better option, and sticking to the strict timelines, you become a much smarter traveler. This knowledge is what separates a smooth claims process from a costly mistake.

A Step-By-Step Guide to Buying and Claiming CFAR

Dipping your toes into the world of travel insurance with cancel for any reason cover can feel a bit overwhelming, but buying and using it is actually pretty straightforward once you know the playbook. Think of it as a simple process for protecting your travel investment.

The journey begins the second you make that first non-refundable payment for your trip. From that moment, the clock starts ticking, which makes acting quickly essential if you want to lock in this powerful coverage.

How to Purchase Your CFAR Coverage

Buying CFAR is all about timing. Unlike a standard policy, you can’t just add this upgrade whenever you feel like it. You have to move fast right after booking your travel.

Here’s your step-by-step checklist to make the purchase seamless:

- Tally Up Your Total Costs: Before you even start shopping, add up every single non-refundable expense. This means flights, hotel deposits, prepaid tours—anything you’d lose if you had to cancel. You have to insure 100% of this total.

- Find a Solid Base Plan: Look for a comprehensive travel insurance policy that already has the medical and standard cancellation coverage you need. For expats, this should be seen as a supplement to, not a replacement for, your annual expat medical insurance plan.

- Select the CFAR Upgrade: As you’re going through the purchase process, you’ll see an option to add the Cancel For Any Reason benefit. It will come with an additional premium.

- Buy Within the Window: This is the big one. You must complete the purchase within the insurer’s strict timeframe, usually 14 to 21 days from your very first trip payment. If you miss this deadline, the option for CFAR is off the table.

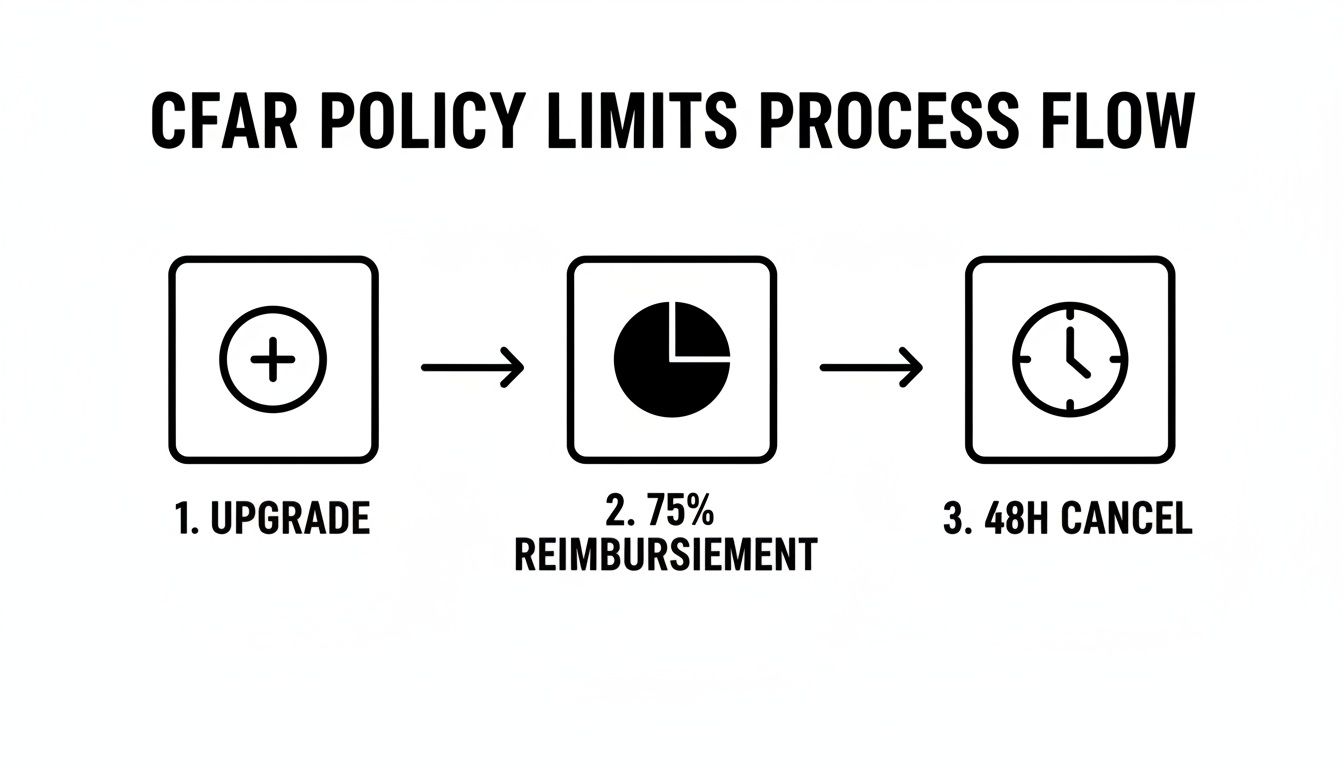

This graphic really breaks down the core rules that make a CFAR policy tick—from the initial upgrade to the reimbursement caps and cancellation deadlines.

The main takeaway here is that CFAR works on a tight schedule with specific reimbursement limits. That’s the trade-off for getting such incredible flexibility.

Filing a Claim The Right Way

If the time comes to actually use your CFAR benefit, a methodical approach is your best friend. It’ll help ensure your claim gets processed without a hitch. The key is to keep organized records right from the get-go.

To successfully file a CFAR claim, you must first cancel your trip with your travel providers. This means calling the airline, emailing the hotel, and letting your tour operators know you won’t be coming before you even start the insurance claim.

Once you’ve notified all your providers, follow these steps to file with your insurer:

- Notify Your Insurer Promptly: Give your insurance company a heads-up about your cancellation as soon as you can, making sure you respect that crucial 48-hour pre-departure deadline.

- Gather Your Documents: Start collecting all the necessary paperwork. You’ll need original receipts for every trip payment, proof of cancellation from each supplier (like their confirmation emails), and your policy documents.

- Submit Your Claim: Fill out the insurer’s claim form and send it in with all your supporting documents. While you don’t have to prove why you canceled, you absolutely have to prove your financial loss.

Common Questions About CFAR Coverage

When you’re dealing with travel insurance with cancel for any reason cover, a few questions always pop up, especially for expats and global travelers whose plans can be pretty complex. Getting straight answers is the only way to use this benefit correctly and protect what you’ve invested in your trip.

Let’s clear up the confusion and tackle the most common questions head-on.

Can I Buy CFAR Insurance at Any Time Before My Trip?

This is a big one, and the answer is a firm no. It’s probably the most critical rule to remember about CFAR coverage because getting it wrong is a costly mistake.

You have a very tight window to add this upgrade. Typically, you must purchase it within 14 to 21 days of making your very first trip payment or deposit. This rule is non-negotiable and exists to prevent people from buying last-minute coverage only when they get a bad feeling about their trip. The key is to plan ahead: add the CFAR rider right when you buy your main travel insurance policy, immediately after you’ve put down your first non-refundable payment.

Does CFAR Reimburse 100 Percent of My Trip Cost?

Another common misunderstanding is that CFAR is a magic “get all your money back” button. It isn’t designed to provide a full, 100% refund.

Instead, CFAR is built to help you recover a large chunk of your prepaid, non-refundable expenses. You can generally expect to get back between 50% and 75%, depending on the specific policy you choose. This partial reimbursement is what allows insurers to offer such an incredibly flexible reason for cancellation.

If you need to cancel for a reason that’s already covered by your standard policy—like a documented, serious illness—you should file a standard trip cancellation claim. That’s the path to getting up to 100% of your money back, making it the smarter financial move in those specific situations.

Is CFAR a Standalone Insurance Policy?

Nope. You can’t buy CFAR by itself. It only exists as an optional upgrade, or “rider,” that you can add to a comprehensive travel insurance policy.

Think of it like this: you first have to buy the main car (a base policy with standard trip cancellation, medical, etc.), and then you can add the sunroof (the CFAR benefit). You need that foundational policy in place before you can enhance it with CFAR. For expats, this travel policy is a separate purchase from your long-term expat medical insurance.

What if My Travel Company Goes Out of Business?

This is a great question, but this scenario is usually handled by the standard part of your policy, not your CFAR benefit. The financial default of a travel supplier—like your airline or tour operator suddenly shutting down—is a covered reason under most standard trip cancellation plans.

If that happens, you would file a regular claim and could be reimbursed up to 100%. The travel insurance with cancel for any reason cover is really meant for all the personal reasons that wouldn’t otherwise be covered—things like a sudden conflict at work, deciding you just don’t want to go anymore, or even feeling unsafe about traveling.

At Expat Global Medical, we specialize in providing insurance solutions that fit the unique needs of a global lifestyle. If you’re planning your next big move or an extended trip abroad, securing the right protection is the first step toward peace of mind. Get a free quote today and explore how our plans can safeguard your journey.