")

Moving abroad is an exciting, life-changing adventure. But here’s a hard truth many U.S. citizens learn too late: your domestic health insurance, including Medicare and ACA plans, becomes virtually useless the moment you cross the border for a long-term stay. This is where expat medical insurance for US citizens steps in. It’s not just a nice-to-have; it’s the essential financial safety net designed specifically to provide comprehensive medical protection while you’re living overseas.

Think of it as your primary health plan, rebuilt from the ground up for an expat lifestyle. An unexpected illness or accident in your new home shouldn’t turn into a financial catastrophe.

Your Guide to Securing Expat Health Coverage Abroad

Planning a new life in another country is filled with big decisions, from choosing a city to fumbling your way through a new language. But arguably the most critical piece of the puzzle—and the one that’s easiest to overlook—is securing reliable healthcare. For Americans, this is a unique challenge because our healthcare system is so fundamentally different from almost anywhere else in the world.

The foundation of a successful move is a solid, long-term expat medical insurance plan. This isn’t some flimsy, temporary travel policy. It’s robust, year-round coverage built for people establishing a new home base abroad. It’s designed to handle everything from emergency hospital stays to routine check-ups and prescription medications.

Why Proactive Planning Is Non-Negotiable

Failing to get proper coverage before you move can have devastating consequences. Imagine facing a serious medical issue in Portugal or getting into an accident in Thailand without that safety net. You’d be on the hook for the full cost of care, a scenario that can wipe out savings in an instant.

Securing coverage isn’t just about managing risk; it’s about giving yourself peace of mind. Knowing you have access to quality healthcare allows you to fully embrace your new expat life without the constant worry of “what if?”

This growing need is clear in the market trends. The broader U.S. travel insurance market, which includes these vital expat health components, is projected to hit $5.8 billion in revenue by 2025. This steady growth is driven by the increasing number of U.S. citizens—expats, retirees, and digital nomads—who understand just how important global protection is. You can explore more data on top insurance carriers to see this trend for yourself.

This guide will walk you through these crucial choices with confidence. We’ll break down exactly what you need to know, ensuring you are protected from the moment you land.

Why Your US Health Insurance Is Useless Overseas

Here’s a hard truth every American planning a move abroad needs to hear: your domestic health insurance won’t be coming with you. It’s one of the most dangerous—and potentially expensive—assumptions you can make as an expat.

Think of your U.S. health plan, whether it’s from your employer, the ACA marketplace, or even Medicare, like a key that only fits one lock. That lock is the American healthcare system.

The moment you settle overseas for an extended period, that key becomes useless. These plans are built around specific networks of U.S. doctors and hospitals. They simply aren’t designed to process claims from a clinic in Lisbon or a hospital in Bangkok. This leaves you completely exposed, facing the full financial weight of any medical care you might need.

The Hard Limits of Medicare and ACA Plans for Expats

Let’s be crystal clear about this. Medicare provides virtually no coverage outside of the United States. There are a few incredibly rare exceptions, like being on a cruise ship within six hours of a U.S. port, but these are irrelevant for anyone actually living abroad. If you’re a retiree dreaming of a life in Mexico or Spain, you cannot count on Medicare for a single thing, from a routine check-up to an emergency surgery.

It’s the same story for plans purchased through the Affordable Care Act (ACA). They are designed for U.S. residents, and their coverage slams to a halt at the border. Trying to rely on an ACA plan while living in another country is a massive financial gamble that can lead to devastating out-of-pocket bills. You can get the full story on why U.S. health insurance doesn’t work abroad.

This is precisely why a dedicated expat medical insurance plan isn’t just a nice-to-have; it’s an absolute necessity.

Travel Insurance Is Not a Long-Term Expat Solution

So, what about travel insurance? It’s a common point of confusion, but mixing up travel insurance and proper expat health insurance is a critical mistake. They serve entirely different purposes for a U.S. citizen abroad.

- Travel Insurance: This is your temporary safety net for short trips and vacations. Its job is to handle trip-related problems like lost luggage and, more importantly, sudden, acute medical emergencies—think a broken leg while skiing or a sudden illness. It’s not built for routine doctor visits or managing long-term health needs as an expat.

- Expat Health Insurance: This is real, comprehensive health insurance designed for someone living in a foreign country. It provides broad, ongoing coverage for everything you’d expect from a primary health plan back home: preventative care, specialist appointments, hospital stays, and managing chronic conditions.

Here’s a simple way to think about it: travel insurance is the first-aid kit in your suitcase, perfect for patching up unexpected scrapes. Expat medical insurance is the fully-staffed hospital you rely on for your actual, long-term healthcare as an expat.

This isn’t a minor distinction—it’s the difference between being truly insured and just having a temporary patch. To make it even clearer, the table below breaks down the crucial differences.

US Domestic vs Travel vs International Expat Insurance

This comparison highlights why only one of these options is truly built for the realities of living abroad as a U.S. citizen.

| Feature | US Domestic Insurance (Medicare/ACA) | Short-Term Travel Insurance | International Expat Health Insurance |

|---|---|---|---|

| Primary Purpose | Long-term care inside the U.S. | Trip protection & emergencies | Comprehensive expat health care abroad |

| Geographic Coverage | U.S. territory only | Specific trip destination | Global or specified regions |

| Duration of Coverage | Annual, for U.S. residents | Per trip (days or weeks) | Annual, renewable long-term |

| Routine & Preventive Care | Yes, within network | No | Yes, typically included |

| Pre-Existing Conditions | Covered under ACA rules | Generally excluded | Can be covered, often with review |

| Medical Evacuation | No | Often included | Standard or optional benefit |

As you can see, trying to make a domestic or travel plan do the job of an expat plan is like trying to fit a square peg in a round hole. For any U.S. citizen planning to live outside the U.S., a proper expat medical insurance plan is the only responsible choice.

Finding The Right Expat Medical Insurance Plan

Once you realize your U.S. health plan won’t cut it abroad, the next step is figuring out the right kind of international coverage. For any U.S. citizen making a long-term move, the gold standard is an expat medical insurance plan. This is the bedrock of reliable healthcare when you’re building a new life in another country.

Think of this as your new primary health insurance, not just a temporary patch. It’s designed to give you the same comprehensive care you’d expect back home, covering everything from emergency surgery and hospital stays to routine check-ups, prescriptions, and managing ongoing health issues.

Matching The Plan To Your Expat Lifestyle

The secret to picking the right expat medical insurance is matching the plan’s purpose to your actual life abroad. After all, not all global lifestyles are the same, and neither are the insurance products built to protect them. Different expat situations call for very different kinds of coverage.

Let’s walk through a few real-world examples to see how this plays out:

- Scenario 1: The Retiree in Mexico

A U.S. citizen retires to San Miguel de Allende. They have a pre-existing condition like diabetes that demands regular doctor visits and medication. A short-term travel plan would be useless here. What they truly need is a long-term expat medical insurance plan that offers robust, ongoing coverage for chronic care, so they can manage their health without breaking the bank. - Scenario 2: The Digital Nomad in Bali

A remote worker is planning an eight-month stint in Bali. They’re healthy but want solid protection for unexpected illnesses or accidents. A full-blown, annually renewable expat plan might be overkill. A short-term international medical plan, built for trips of three to twelve months, strikes the perfect balance of emergency and general medical coverage for their stay. - Scenario 3: The Engineer in a Remote Location

An American engineer signs a two-year contract at a remote mining site in South America, hours from the nearest decent hospital. A standard plan might not be enough. Their number one priority should be medical evacuation coverage. This ensures that if a serious accident happens, they can be flown to a top-tier medical facility, even if it means an international flight.

The Core Components Of Expat Medical Insurance

While the details can vary, a true long-term expat plan is built to be a complete health solution. This is what makes it fundamentally different from a travel policy, which is only for acute, unexpected problems. A quality expat plan will almost always include a wide array of benefits.

These plans are absolutely essential for anyone living abroad for a year or more, giving you a seamless healthcare experience. If you want to go deeper, you can learn more about finding the best expat medical insurance for your life abroad in our detailed guide.

The crucial takeaway is that your plan’s structure must align with your expat needs. Choosing the wrong type of coverage—like relying on travel insurance for a long-term move—creates dangerous gaps that can leave you financially exposed when you are most vulnerable.

A solid expat health plan should always offer:

- Inpatient and Outpatient Care: Covers everything from major surgeries requiring a hospital stay to simple doctor’s appointments and lab tests.

- Emergency Services: This includes ambulance rides, emergency room treatment, and urgent care visits.

- Prescription Drug Coverage: A must-have for anyone needing regular medication for chronic or acute conditions.

- Wellness and Preventive Care: Many plans cover annual check-ups, vaccines, and health screenings to help you stay ahead of any issues.

- Optional Benefits: You can often add riders for dental, vision, and maternity care to build a policy that fits your specific health needs.

Ultimately, choosing the right expat medical insurance for US citizens comes down to an honest look at your plans, your health, and where you’re headed. By understanding the core types of coverage out there, you can make a smart decision that provides genuine peace of mind.

What Drives The Cost Of Your Expat Health Plan

Figuring out what shapes the price tag on your expat medical insurance is the first step to finding a plan that actually protects you without blowing up your budget. An expat health plan isn’t a simple, one-size-fits-all product. Instead, its premium is a blend of several key factors that reflect your personal situation and the level of risk the insurer takes on.

Think of it like building a custom car. The base model has a set price, but every feature you add—a bigger engine, a premium interior, advanced safety systems—nudges the final cost up. Your insurance premium works exactly the same way.

Your Age And Personal Profile

The most fundamental factor is your age. It’s just a statistical reality: older individuals are more likely to need medical care, so premiums naturally rise as we get older. This is standard practice across the entire insurance industry.

Beyond your age, your overall medical history plays a huge role. Insurers need to look at your past and current health to get a sense of your potential future needs, which brings us to the big one: pre-existing conditions.

Handling Pre-Existing Conditions

A pre-existing condition is any medical issue you had before your new insurance coverage kicked off. Insurers like Cigna or GeoBlue have different ways of handling these, and it’s absolutely vital to be completely upfront and honest on your application.

Here’s how it usually plays out:

- Waiting Period: The insurer might agree to cover a condition, but only after a specific “wait and see” period has passed, like 12 or 24 months, without any symptoms or treatment.

- Premium Surcharge: A more common approach is to cover the condition but at a higher premium. This is often called a surcharge or a “loading.”

- Exclusion: For particularly complex or chronic conditions, the insurer might offer you a policy but specifically exclude any costs related to that one illness.

Knowing these possibilities helps you set realistic expectations from the get-go.

The Impact Of Geographic Coverage

Where you need coverage is a massive cost driver. Healthcare isn’t priced the same everywhere. A procedure in Monaco or Switzerland will be wildly more expensive than the same one in Vietnam or Thailand. Insurers price their plans to reflect this, often creating different coverage zones. A worldwide plan will always cost more than one limited to, say, Southeast Asia.

For U.S. citizens, the single biggest geographic factor is whether you need coverage back home.

Choosing a plan that includes the United States is like adding a high-performance engine to that custom car—it dramatically increases the cost but provides powerful benefits if you need care during visits home. This is the biggest lever you can pull to influence your premium.

The reason? The absolutely staggering cost of American healthcare. Just look at U.S. hospital services costs—they exploded by 227.2% between January 2000 and December 2022, blowing past general inflation. This trend makes including U.S. coverage a major financial decision for both you and the insurer. You can discover more insights about these U.S. price impacts and see just how much they affect global insurance pricing.

Customizing Your Plan With Deductibles And Co-Insurance

Finally, you can take control of your premium by adjusting your plan’s cost-sharing elements. These are the tools that let you balance what you pay each month against what you’ll pay out-of-pocket when you actually need care.

- Deductible: This is the fixed amount you pay for medical care each year before the insurance company starts chipping in. Choosing a higher deductible, like $5,000 instead of $500, means you’re taking on more initial risk, which will significantly lower your monthly premium.

- Co-insurance: This is the percentage of the medical bill you pay after you’ve met your deductible. A common split is 80/20, where the insurer pays 80% and you cover the remaining 20% of the costs. Agreeing to a higher co-insurance percentage on your end can also bring down your premium.

By carefully choosing your coverage area and tweaking these cost-sharing features, you can fine-tune your expat medical insurance for US citizens to perfectly match your needs. To get into the nitty-gritty of pricing, check out our detailed guide on understanding expat health insurance cost. This strategic approach ensures you get the protection you need at a price you can actually afford.

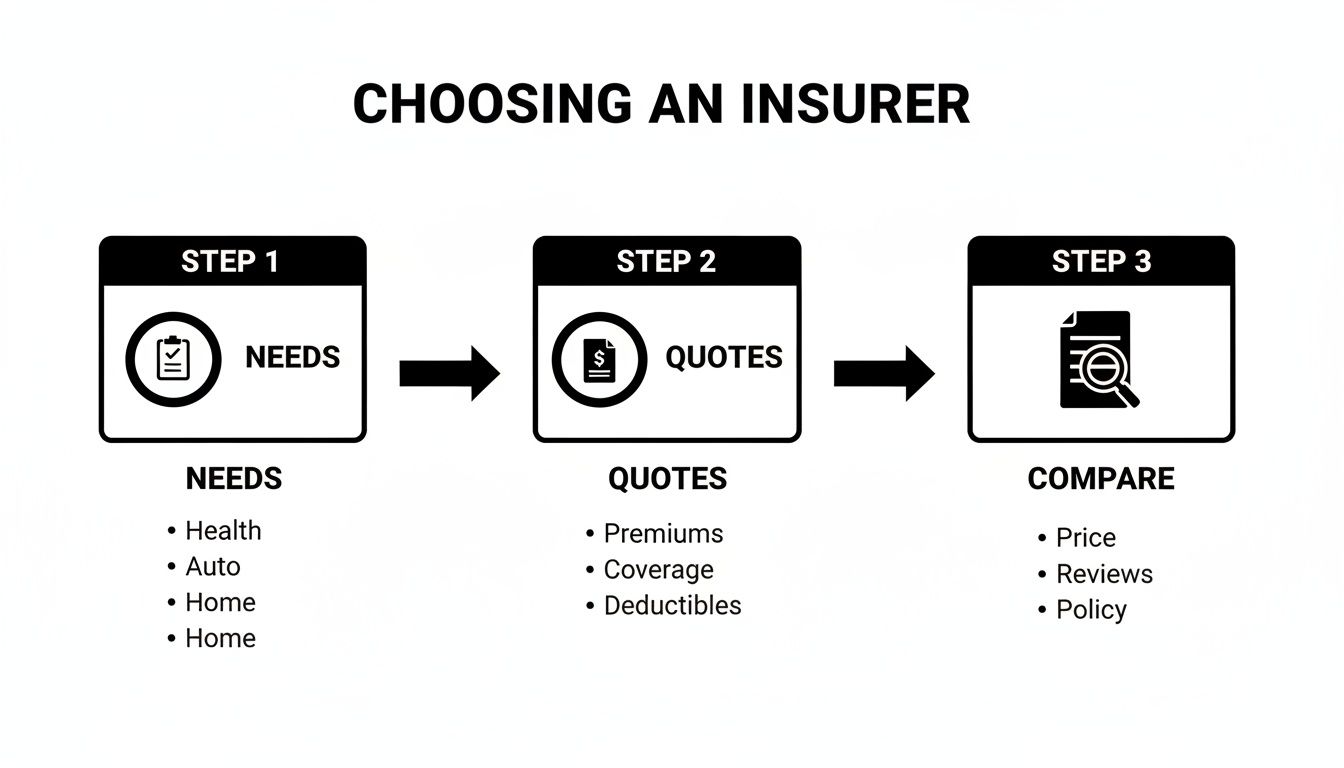

How to Choose the Best Expat Medical Insurer

Picking an insurer for your expat medical insurance for US citizens is a lot more than just chasing the lowest price. Think of this company as your healthcare partner for your entire life abroad. Choosing a stable, reliable company is every bit as important as the fine print in the policy itself. A practical, step-by-step approach will help you make a choice you can feel good about.

The whole process starts with a good, honest look at your own needs. Once you have a clear picture, you can start gathering quotes from reputable carriers and really dig into what they’re offering. It means looking past the monthly premium to see the real value hiding behind the price tag.

Assessing Your Needs and Getting Quotes

First things first, create a personal health profile. Are you generally healthy, or are you managing a pre-existing condition that needs regular attention? Do you think you might need specialized care, dental work, or even maternity services down the road? Answering these questions gives you a solid blueprint for your ideal coverage.

With that blueprint in hand, it’s time to get quotes from well-regarded insurance carriers. You’ll want to focus on companies with a long, proven history in the expat market, like Cigna, GeoBlue, or IMG. These guys have the global infrastructure and experience to properly support US citizens living anywhere in the world. Just be sure to give each carrier the exact same information to get quotes you can accurately compare side-by-side.

Look Beyond the Monthly Premium

A low premium can look mighty tempting, but it often comes with significant strings attached. When you’re comparing policies, you have to dig deeper to understand what you’re actually getting for your money. A plan that costs a bit more each month might offer vastly better protection and service, potentially saving you thousands if something serious happens.

Here are the critical details to zero in on:

- Provider Network: Does the insurer have a strong network of hospitals and clinics in your destination country that offer direct billing? Direct billing is a huge deal—it means the hospital bills the insurer directly, so you aren’t stuck paying a massive bill upfront and waiting for reimbursement.

- Coverage Limits: Pay close attention to the annual maximum benefit. A plan with a $1 million limit just doesn’t offer the same level of catastrophic protection as one with a $5 million limit.

- Exclusions and Waiting Periods: Get into the fine print and see what isn’t covered. Look carefully for any waiting periods on specific benefits, like maternity care or coverage for pre-existing conditions, so there are no surprises later.

- Claims and Emergency Process: How easy is it to file a claim? More importantly, what’s their process for a real emergency? You’ll want a company with a 24/7 assistance line and multilingual support you can count on.

Choosing the right insurer is like picking a co-pilot for your global journey. You need a partner who is financially sound, has a proven track record, and is ready to respond effectively when you hit turbulence.

Verifying Insurer Stability and Reputation

An insurance policy is only as good as the company backing it. Before you sign on the dotted line, take a little time to check out the insurer’s financial health and what other expats are saying about them. This bit of due diligence is absolutely crucial for your peace of mind.

A great indicator of an insurer’s strength is its financial stability rating from agencies like A.M. Best. A rating of “A” (Excellent) or higher is a strong signal that the company can meet its financial obligations. You should also read real customer reviews and testimonials to get a feel for their customer service and how they handle claims.

The importance of this can’t be overstated. A staggering 86.97 million people were covered by plans from members of the U.S. Travel Insurance Association (USTIA). With emergency medical costs being one of the top claims for long-haul trips, the reliability of your insurer is everything. You can learn more about these critical travel insurance statistics to see just why picking a solid provider is so essential.

By following this simple framework—assessing your needs, comparing the nitty-gritty policy details, and vetting the insurer’s stability—you can find a global medical insurer that gives you more than just a policy. You’ll have a genuine partner dedicated to protecting your health abroad.

Enrolling In Your Expat Plan And Making A Claim

You’ve done the hard work of comparing plans and have zeroed in on the right insurer. Now, it’s time to move from planning to action. The enrollment process for an expat medical insurance plan for US citizens is usually pretty straightforward, but you’ll want to pay close attention to the details to make sure everything goes off without a hitch.

The application is the heart of the process. You’ll be asked for personal information, details about your move or long-term travel, and a complete medical history. This is where honesty is non-negotiable. Trying to hide a pre-existing condition might seem tempting, but it can backfire badly, leading to a denied claim or even having your policy canceled just when you need it most.

The Application And Underwriting Journey

Once you hit “submit” on your application, it heads into underwriting. This is the behind-the-scenes step where the insurer’s team reviews your medical background to assess their risk and finalize your policy’s terms and cost. For healthy folks with no complex medical history, this can be a surprisingly quick process, sometimes wrapping up in just a few days. However, if the underwriters need to dig into medical records for a pre-existing condition, it can stretch out for several weeks.

To keep things moving smoothly, it helps to have these documents ready to go:

- A clear copy of your passport to verify your identity.

- Your complete medical history, including any treatments or medications you’re currently on.

- In some cases, they might ask for the contact information of your primary care doctor.

This simple graphic lays out the high-level steps you take to choose your insurance partner, long before you even fill out that first application form.

As you can see, the journey really begins with figuring out what you need, then getting quotes, and finally, lining them up to compare before you commit to enrolling.

Navigating Medical Care Abroad

The moment of truth arrives when you actually have to use your insurance. Knowing how to get care and handle the bills is absolutely essential. There are two main ways medical bills are handled when you’re abroad.

The key is knowing which payment method your plan uses and what to do in an emergency. Contacting your insurer’s 24/7 assistance line immediately should always be your first step in a serious medical situation.

That one phone call sets critical support in motion. They can help coordinate your care, guarantee payment to the hospital so you’re not hassled, and even arrange an emergency evacuation if it’s medically necessary.

Here’s a breakdown of how the payment part usually works:

- Direct Billing: This is the ideal scenario. The hospital or clinic has a direct relationship with your insurer and sends the bill straight to them. You just show your insurance card, pay your deductible or co-pay, and you’re done.

- Reimbursement: If you end up at a facility that’s not in your insurer’s network, you’ll probably have to pay the entire bill yourself, right then and there. You then need to collect all the detailed receipts and fill out a claim form to send to your insurer, who will then reimburse you for the covered expenses.

Your Questions, Answered

Stepping into the world of expat medical insurance can feel a bit like learning a new language. It’s natural to have questions. Here are some straightforward answers to the things U.S. expats most frequently ask us.

Does Expat Insurance Cover Me On Visits To The USA?

Yes, but it’s a major cost driver. Many top-tier expat medical plans offer riders or built-in benefits for short trips back home. Because U.S. healthcare costs are astronomical, adding this feature will significantly bump up your premium. Plans like GeoBlue Xplorer are built from the ground up to handle this, offering solid stateside coverage for those who know they’ll be back often.

What Happens If I Have A Pre-Existing Condition?

This is where policies really differ. Some insurers will cover pre-existing conditions after a set waiting period, while others might accept you but tack on a surcharge. It’s also possible for a plan to cover you for everything except that specific condition.

Complete honesty on your application isn’t just a good idea—it’s essential. A seasoned broker knows which insurers are more flexible with certain conditions and can steer you toward a plan that offers the most favorable terms for your health history.

This way, you avoid any nasty surprises right when you need your coverage the most.

Can I Still Use My ACA Plan While Living Abroad?

Legally, you can keep your Affordable Care Act (ACA) plan, but practically, it’s useless outside the United States. Relying on an ACA plan for your healthcare while living as an expat is a huge financial gamble. For genuine protection covering everything from a routine check-up to a serious emergency in your new country, a dedicated expat medical insurance plan is the only real solution.

How Far In Advance Should I Apply For A Plan?

Give yourself a buffer of at least 30 to 45 days before you move. This is crucial for the underwriting process, which is where the insurer reviews your application and health history.

- If you have a clean bill of health: Approval can be as quick as a few days.

- If you have a more complex medical history: Underwriters may need to request and review your medical records, a process that can easily stretch into several weeks.

Applying early means your policy will be active and ready to go from the moment you land. Don’t leave this critical piece of your expat puzzle to the last minute.

Finding the right protection is the most important step in your journey abroad. At Expat Global Medical, we specialize in helping U.S. citizens secure reliable and affordable expat medical insurance. Get a free quote today and let our experts build a plan that safeguards your global lifestyle.