")

When you move abroad, your life changes, but your need for reliable healthcare doesn’t. International medical insurance is the answer for expats and their families—it’s a comprehensive, long-term health plan designed specifically for people living outside their home country.

This isn’t your average short-term travel policy. Think of it as your primary health plan, covering everything from routine doctor visits to unexpected, major medical emergencies. It’s built to give you consistent, quality healthcare access, no matter where your journey takes you.

Your Healthcare Passport for a Life Abroad

International medical insurance is your healthcare passport for living abroad. Just as a regular passport gets you into a new country, this insurance opens the door to medical care and financial security while you’re there. It’s crafted to handle the unique challenges expats face, filling the critical gap between your old healthcare system and the new one.

Let’s be clear: your domestic health plan from back home is designed for a specific network of doctors and hospitals. The moment you move overseas for any real length of time, that coverage becomes practically useless. This is exactly why a dedicated international plan is so crucial for any expat.

Why Your Plan from Back Home Just Won’t Cut It

Trying to rely on your domestic insurance while living abroad is a gamble you don’t want to take. These plans simply aren’t built for a global lifestyle. The differences are stark:

- Geographic Walls: Most home-country policies draw a hard line at the border, leaving you completely exposed once you’re overseas.

- Useless Networks: Your approved list of doctors and hospitals doesn’t extend globally. Any care you get would be considered “out-of-network,” which usually means “not covered.”

- Missing Expat Essentials: Critical benefits like medical evacuation, repatriation, and 24/7 multilingual support are standard in expat plans but completely absent from domestic ones.

An international medical insurance plan is your financial safety net. It protects you from potentially devastating healthcare costs in a foreign country and gives you the peace of mind to actually enjoy your new life without the fear of a medical bill wiping you out.

A Growing Need for Global Coverage

As more people pack their bags for international opportunities, the demand for this kind of specialized insurance is booming. The international medical insurance market was valued at around USD 25.5 billion in 2022 and is on track to hit nearly USD 67.9 billion by 2031.

This explosive growth tells a simple story: professionals and families moving abroad understand they need a real, long-term health solution they can count on.

Of course, health coverage is just one piece of the puzzle. Getting the practical things sorted is just as important for a smooth transition. For instance, figuring out the local banking system is a must-do, and a good guide on opening a bank account in Singapore for expats can be a lifesaver. Getting these foundational elements right from the start makes all the difference.

Choosing Your Expat Health Plan Type

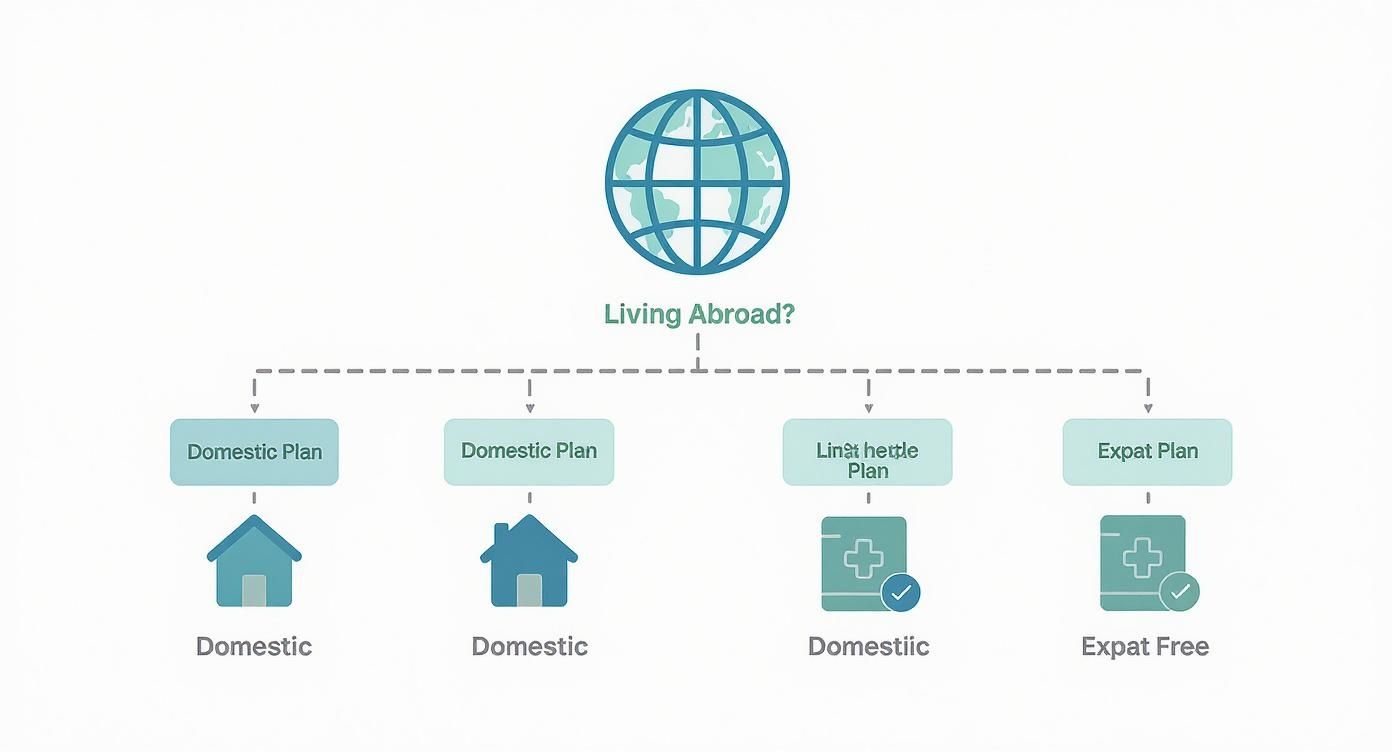

Figuring out the right type of international medical insurance for expats can feel like a maze, but it really just boils down to your specific plans. Not all insurance is created equal, and picking the wrong kind is a classic—and often expensive—expat mistake. The single most important thing to get right from the start is the difference between a simple travel policy and a genuine expat health plan.

Many first-time expats think travel insurance is all they need. It’s not. In fact, they’re two completely different products. Travel insurance is for short trips and is built to handle travel emergencies—a canceled flight, lost bags, or a sudden illness during a two-week holiday. Think of it as a temporary safety net for things that go wrong while you’re traveling.

International medical insurance, on the other hand, is your actual health coverage for long-term living abroad. It acts just like the health plan you had back home, covering everything from routine doctor’s appointments and preventative care to specialist visits and major surgeries. Relying on travel insurance for your day-to-day life as an expat is like trying to drive cross-country on a spare tire; it was never designed for that kind of journey and is guaranteed to fail when you need it most.

This decision tree can help you visualize which path makes the most sense for you.

As you can see, if you’re truly living overseas, a dedicated expat health plan is the only way to get comprehensive and reliable coverage.

Short-Term vs. Annual Expat Plans

Once you’ve correctly ruled out travel insurance, your next decision is between a short-term or a long-term (annual) expat health plan. This choice hinges entirely on how long you plan to be away and what you’ll be doing.

A short-term plan is perfect for assignments or stays lasting anywhere from a few months up to a year. These policies give you solid coverage without locking you into a long-term contract. For example, if you’re a digital nomad testing out a new city for six months or you’re on a temporary work project, a short-term policy is exactly what you need.

An annual plan is the go-to choice for anyone moving for a year or longer, or relocating indefinitely. These are renewable policies designed to be your ongoing healthcare solution abroad. They offer more robust, stable coverage, often with better terms for chronic conditions and options for lifetime renewal. This is the path for expats who are truly setting up a new home base.

Choosing between short-term and annual coverage isn’t just about the price tag; it’s about aligning your insurance with your life. A mismatch can leave you seriously underinsured or paying for coverage you simply don’t need.

Travel Insurance vs. International Medical Insurance

To make an informed decision, you need to be crystal clear on what each plan is designed to do. Let’s break down the core differences in a simple, side-by-side comparison.

| Feature | Travel Insurance | International Medical Insurance |

|---|---|---|

| Primary Use | Short-term travel hiccups, trip protection, emergencies. | Primary health coverage for long-term living abroad. |

| Coverage Scope | Limited emergency medical, cancellations, lost luggage. | Comprehensive inpatient, outpatient, wellness, and routine care. |

| Duration | Days or weeks, sometimes up to a few months. | Typically annual and renewable for long-term needs. |

| Renewability | Generally not renewable; a new policy is needed. | Designed for annual renewal to provide continuous coverage. |

Ultimately, the type of plan you select dictates how you’ll access healthcare in your new country. This choice directly impacts which doctors and hospitals you can see, which is why it’s also worth learning about the differences between PPO and HMO networks for expats to ensure your plan offers the flexibility you need.

Understanding Your Core Coverage and Key Benefits

An international medical insurance policy can feel a bit overwhelming at first, but when you boil it down, it’s really designed to cover two fundamental areas of healthcare. Think of these as the foundation of your plan, built to protect you whether you’re dealing with a minor bug or a major medical emergency.

These two pillars are inpatient care and outpatient care. Just about every expat health plan is built around these core benefits, and getting a handle on what they mean is the first step toward picking the right coverage for your life abroad.

Inpatient care is for the serious stuff—medical issues that require you to be admitted to a hospital. This covers things like surgeries, overnight stays for treatment, and intensive care. It’s the coverage you hope you never have to use, but it’s absolutely essential to have for that “what if” moment.

Outpatient care, on the other hand, is for everything else that doesn’t require a hospital bed. This is your day-to-day healthcare: visiting a GP for a check-up, getting lab tests done, or having an X-ray or MRI.

Beyond the Basics: Essential Add-Ons

While inpatient and outpatient coverage form the bedrock of any plan, most expats find they need a bit more than just the basics to feel truly secure. This is where optional add-ons, often called riders, come into play. They let you customize your plan so it actually fits your life.

Some of the most common and important add-ons to consider are:

- Dental and Vision: Routine dental cleanings, fillings, and new glasses are rarely part of a core plan, but they’re crucial for staying healthy long-term.

- Maternity Care: If starting or growing your family abroad is in your plans, this coverage is a must-have. It typically handles prenatal visits, the delivery itself, and postnatal care. Just be aware that most insurers have a waiting period, often 10-12 months, before maternity benefits kick in.

- Mental Health Support: Let’s be honest, living abroad can be stressful. This benefit gives you access to therapists, psychologists, and other mental health professionals, making sure you can look after your emotional well-being just as you do your physical health.

The Ultimate Safety Net: Medical Evacuation

Of all the benefits you can get, medical evacuation and repatriation is arguably the most critical for any expat. This is your ultimate safety net, designed for a worst-case scenario that is, unfortunately, a real possibility for many people living far from home.

Imagine you’re in a country with limited medical facilities and you have a severe accident or a complex illness. The local hospitals simply may not have the specialists or equipment to give you the care you need. This is exactly where medical evacuation becomes a lifesaver.

Medical Evacuation (Medevac): This benefit covers the massive cost of transporting you from where you are to the nearest medical center that can provide the right level of care. That might be a top-tier hospital in a nearby capital city or even in another country altogether.

Repatriation takes it a step further. It covers the cost of flying you back to your home country for treatment if it’s medically necessary. Without insurance, these emergency transport services can easily cost tens or even hundreds of thousands of dollars.

A Real-World Evacuation Scenario

Let’s make this real. An expat is working remotely in a beautiful but remote part of Southeast Asia. He gets into a serious motorcycle accident and suffers multiple fractures and internal injuries. The local clinic is completely unequipped to handle complex orthopedic surgery.

Without medical evacuation coverage, he and his family face a terrible choice: settle for inadequate care locally or drain their life savings to pay for an emergency air ambulance to a major hospital in Bangkok or Singapore.

With a proper international medical insurance for expats plan, the process is simple. One call to the insurer’s 24/7 emergency hotline kicks a coordinated plan into high gear. The insurance company arranges and pays for the medically supervised flight, getting the expat to the right surgeons without delay. This single benefit can be the difference between a full recovery and a life-altering tragedy, making it a non-negotiable part of any solid expat health plan.

Managing Costs: Premiums and Policy Limits

Let’s talk money. Getting a handle on the financial side of international medical insurance for expats is one of the most important steps to making a smart choice. It’s not just about what you pay each month; it’s about understanding how your policy is structured to share costs and what really drives your price up or down. A solid grasp of these details means no nasty surprises or unexpected bills down the road.

Think of managing your insurance costs like a three-legged stool. Each leg—the deductible, co-insurance, and out-of-pocket maximum—plays a crucial role. Together, they create a balanced and predictable way to handle what you pay for your healthcare.

How Deductibles and Co-Insurance Work Together

Your deductible is what you pay out-of-pocket for medical services before your insurance company starts chipping in. For instance, if your plan has a $1,000 deductible, you’re on the hook for the first $1,000 of your covered medical bills each year.

Once you’ve paid that deductible, co-insurance comes into play. This is where you and your insurer share the cost of the remaining bill, based on a set percentage. A common split is 80/20, which means the insurance company covers 80% of the cost, and you pay the other 20%.

Then there’s the out-of-pocket maximum, which is your ultimate financial safety net. It’s the absolute most you will have to pay for covered medical care in a policy year. After you hit this limit, your insurer pays 100% of all covered costs for the rest of that year.

Example in Action: Let’s say your policy has a $1,000 deductible, 80/20 co-insurance, and a $5,000 out-of-pocket maximum. You end up needing a medical procedure that costs $20,000.

- You first pay the $1,000 to meet your deductible.

- The remaining bill is $19,000. Your 20% co-insurance share of that is $3,800.

- Your total payment is $1,000 + $3,800 = $4,800. Since this is less than your $5,000 maximum, this is what you owe. Your insurer handles the rest.

Key Factors That Influence Your Premium

The price you’re quoted for an international health plan isn’t pulled out of thin air. It’s carefully calculated based on a few key factors. Knowing what they are helps you understand why quotes vary so much and how you might be able to tweak your plan to better fit your budget.

- Your Age: This is one of the biggest drivers. Simply put, younger people generally have lower health risks, which translates to lower premiums.

- Geographic Coverage Area: Where you need coverage matters—a lot. A plan that includes the USA will always be significantly more expensive because of the notoriously high cost of healthcare there. Opting for a “Worldwide excluding USA” policy can lead to substantial savings.

- Level of Coverage: The more benefits you add—like comprehensive dental, vision, and maternity care—the higher your premium will be.

Medical inflation is another major force that shapes premiums. Healthcare costs are rising rapidly across the globe, with some reports showing annual increases of 12.1% in Africa and the Middle East and 9.3% in Europe. These trends have a direct impact on insurance pricing, often leading to premium hikes between 8% to 25% each year, depending on your age and benefits.

Understanding Common Exclusions and Limits

Every insurance policy has its boundaries. Knowing what your plan doesn’t cover is just as critical as knowing what it does. These are called exclusions, and paying attention to them can save you from the shock of a denied claim.

Here are a few common exclusions to look out for:

- Pre-existing Conditions: Many plans won’t cover health problems you had before you enrolled. Some may offer coverage after a waiting period or for a higher premium, but it’s never a given.

- High-Risk Activities: Got a taste for adventure? Injuries from activities like scuba diving, rock climbing, or competitive sports often aren’t covered unless you purchase a special add-on or rider.

- Cosmetic Procedures: Any elective surgery that isn’t deemed medically necessary is almost always excluded.

- Addiction Treatment: Coverage for substance abuse rehabilitation can be very limited or excluded completely.

The best advice is to always read your policy documents from front to back to understand these limits. For a deeper dive into the numbers, check out our comprehensive international medical insurance cost guide. It will give you a much clearer picture of what to expect and how to budget for your new life abroad.

How to Find the Right Insurance Plan for You

Choosing an international medical insurance for expats is about so much more than just comparing monthly premiums. Think of it as finding a true partner for your health journey abroad—one you can count on to deliver real peace of mind when you need it most. This guide will walk you through the factors that actually matter, helping you look beyond the price tag to see what a plan genuinely offers.

To get started, you need a simple framework for matching your unique situation to what different providers have on the table. It’s like creating a personal checklist. This makes sure you aren’t swayed by flashy marketing and can focus on the substance of the coverage and the quality of service you’ll get.

Start With Your Personal and Geographic Needs

Before you even glance at a single quote, take a moment to look inward. The right plan for a solo digital nomad bouncing around Southeast Asia is worlds apart from the ideal coverage for a family of four putting down roots in Europe.

Kick things off by asking yourself a few straightforward questions:

- Family Health: Do you or anyone in your family have chronic conditions or specific medical needs that require ongoing care? This is non-negotiable.

- Destination Healthcare: What’s the healthcare system like where you’re going? Moving to a country with fantastic but pricey private care (think Switzerland) demands a different plan than moving somewhere with more limited facilities.

- Lifestyle: Are you an adrenaline junkie who loves high-risk hobbies? Or maybe you’re thinking about starting a family? Your lifestyle choices have a direct line to the kind of coverage you’ll need.

Dig Into the Insurer’s Network and Reputation

Once you have a clear picture of your needs, it’s time to scrutinize the insurance companies. This is where you separate the good from the great. An insurer’s global medical network is one of the most critical pieces of the puzzle. This is simply the list of hospitals, clinics, and doctors that have a direct working relationship with the insurance company.

A strong network is your ticket to seamless healthcare. It means less paperwork, less out-of-pocket stress, and faster access to care. This brings us to a crucial distinction you absolutely need to grasp: direct billing versus pay-and-claim.

Direct Billing vs. Pay-and-Claim

Think of a direct billing network like using your credit card at a store. The hospital sends the bill straight to your insurer, and you usually only handle a small copay, if anything. It’s a cashless, no-fuss experience. A pay-and-claim system is more like paying with cash and waiting for a rebate; you foot the entire medical bill upfront and then submit your receipts to the insurer to get your money back.

While you might run into pay-and-claim situations occasionally, a provider with a solid direct billing network makes life infinitely easier, especially when you’re already dealing with a stressful medical issue.

Don’t Overlook Customer Service and Claims

An insurer’s reputation for customer service is just as vital as its network. When you’re sick or hurt in a foreign country, the absolute last thing you want is to battle an unresponsive call center or navigate a painfully slow claims process.

Look for these signs of top-notch service:

- 24/7 Multilingual Support: Can you get help in your language, day or night?

- Easy Claims Process: Do they have a simple online portal or a mobile app for submitting claims?

- Payout Reputation: Read the reviews. Do they have a solid track record of paying claims fairly and without a fight?

Picking a provider is a huge decision that directly impacts your health and financial security. To help you weigh your options, our guide to the best international health insurance providers offers detailed comparisons and insights to simplify your search and find a plan that truly has your back.

From Application to Your First Claim

Getting your international medical insurance for expats policy is the first big step. But what really matters is knowing how to use it when you actually need it. The admin side of things can feel a little daunting at first, but thankfully, most providers have made the process pretty straightforward.

Let’s walk through how it works, from filling out the application to handling your first doctor’s visit. Understanding the flow from day one takes all the anxiety out of the equation.

It all starts with the application, where you’ll share your personal details and health history. This information goes into medical underwriting, which is just the insurer’s way of getting to know your health profile. Be totally upfront here—full disclosure of any pre-existing conditions is absolutely essential to make sure your policy is rock-solid when you need to rely on it.

Once you’re approved, you’ll get your policy documents, your insurance card, and access to an online member portal. Pro tip: The moment you get these, save your insurer’s 24/7 assistance number in your phone. You’ll thank yourself later.

Your First Doctor’s Visit In-Network

Let’s say you need a routine check-up. The simplest path is to use your insurer’s direct billing network. This whole system is designed to be cashless and hassle-free, so you can focus on your health instead of payments.

- Find a Provider: Hop on your insurer’s online portal or app to find a clinic or hospital in their network.

- Schedule and Present Your Card: When you book the appointment, let them know about your insurance. Once you’re there, just show them your insurance card like you would back home.

- Treatment and Sign-Off: After your consultation, you’ll likely sign a form. The clinic handles the rest, billing your insurance company directly for everything that’s covered.

This direct-billing feature is a huge perk of a good international medical insurance for expats plan. It means you aren’t shelling out big bucks from your own pocket for most routine care.

When You Need to File a Claim

Of course, sometimes you might need to see a doctor who isn’t in the network, or maybe pop into a local pharmacy where direct billing isn’t set up. In those situations, you’ll use the pay-and-claim reimbursement process.

This just means you pay for the service yourself first, then send the paperwork to your insurer to get your money back. It sounds like an extra step, but modern insurers have made it way easier than it used to be.

Here’s the typical flow:

- Pay and Get Receipts: Settle the medical bill on the spot. The crucial part is to ask for an itemized invoice and a formal receipt of payment.

- Submit Your Claim: Log into your insurer’s online portal or pull up their mobile app. You’ll fill out a quick claim form and upload photos or scans of your documents.

- Receive Reimbursement: The insurance company reviews your claim. Once it’s approved, they’ll send the covered amount back to you, usually through a bank transfer.

The secret to a smooth reimbursement is just keeping clear records. This flexibility ensures that your coverage has your back, even if you’re miles away from a network provider.

Your Top Questions About Expat Medical Insurance, Answered

Even after getting a good handle on international medical insurance, a few questions almost always pop up. We get it. This is a big decision for any expat. Here are the answers to some of the most common queries we hear, designed to give you that last bit of clarity before you move forward.

Can I Just Keep My Health Insurance From Home While I’m Living Abroad?

Technically, you can keep paying for it, but it’s a terrible idea that offers virtually no real protection overseas. Domestic insurance plans are designed to work within one specific country’s healthcare system. They almost never cover routine doctor’s visits, ongoing treatments, or direct billing in another country.

Trying to rely on your old plan is a massive financial gamble. You’ll be paying for nearly everything out-of-pocket, and you can expect most of your claims to be flat-out denied. The only practical solution is a true international medical insurance for expats plan—it’s the only type of policy built for global coverage from the ground up.

What’s the Difference Between “Worldwide” and “Worldwide Excluding USA” Coverage?

This is one of the single biggest choices that will affect your premium, so it’s a critical one to understand. A “Worldwide excluding the USA” plan gives you medical coverage anywhere on the planet except for the United States, which is notorious for having the most expensive healthcare system in the world.

A “Worldwide” plan, as the name suggests, includes coverage for treatment inside the USA. If you don’t plan on living in or spending significant time in the States, choosing the “excluding USA” option is a savvy move. It can dramatically lower your premium while still giving you fantastic protection everywhere else you might go.

Choosing the right geographic coverage is one of the smartest ways to manage your insurance costs. For the vast majority of expats, a “Worldwide excluding USA” plan hits the perfect sweet spot between comprehensive global access and a much more affordable price tag.

Is It Possible to Get Coverage for Pre-Existing Conditions?

This is a big one, and the answer isn’t a simple yes or no—it really depends on the insurer and the specific plan. Some policies might completely exclude a known condition. Others might agree to cover it after a waiting period, often around 24 months of continuous coverage without any issues.

In some situations, an insurer will offer to cover a pre-existing condition right away but will add a surcharge to your premium. The most important thing you can do is fully and honestly disclose all your medical history on your application. This is where an experienced broker is your best friend; they can guide you toward insurers known for being more flexible with specific health conditions.

How Does Medical Evacuation Actually Work in an Emergency?

Medical evacuation, or “medevac,” is a lifeline. It’s a benefit designed for worst-case scenarios where you have a major injury or illness in a place that just doesn’t have the medical facilities to treat you properly.

When that happens, your insurance company steps in to coordinate and pay for your transportation to the nearest capable medical center. That could be a flight to a bigger city in the same country or even a medically-staffed flight to a different country altogether. For any expat living in a remote area or a nation with a less-developed healthcare system, this coverage is absolutely non-negotiable. Without it, the cost of a private medical evacuation can easily run into the hundreds of thousands of dollars.

Ready to find the international health plan that gives you true peace of mind for your life abroad? The experts at Expat Global Medical are here to help you sort through the options, compare quotes, and build a policy that fits you perfectly.